In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Lithium which can be used to treat a wide variety of pre-existing medical conditions including:

- Bipolar disorder,

- Depression,

- Schizophrenia,

- Anorexia,

- Bulimia,

Lithium may also be used in conjunction with other medications to help treat:

- Migraine relief,

- Alcohol treatment,

- Epilepsy,

- Diabetes,

- Liver disease,

- Kidney disorders,

- Arthritis,

- Etc, etc…

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Lithium?

- Why do life insurance companies care if I’ve been prescribed Lithium?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been prescribed Lithium?

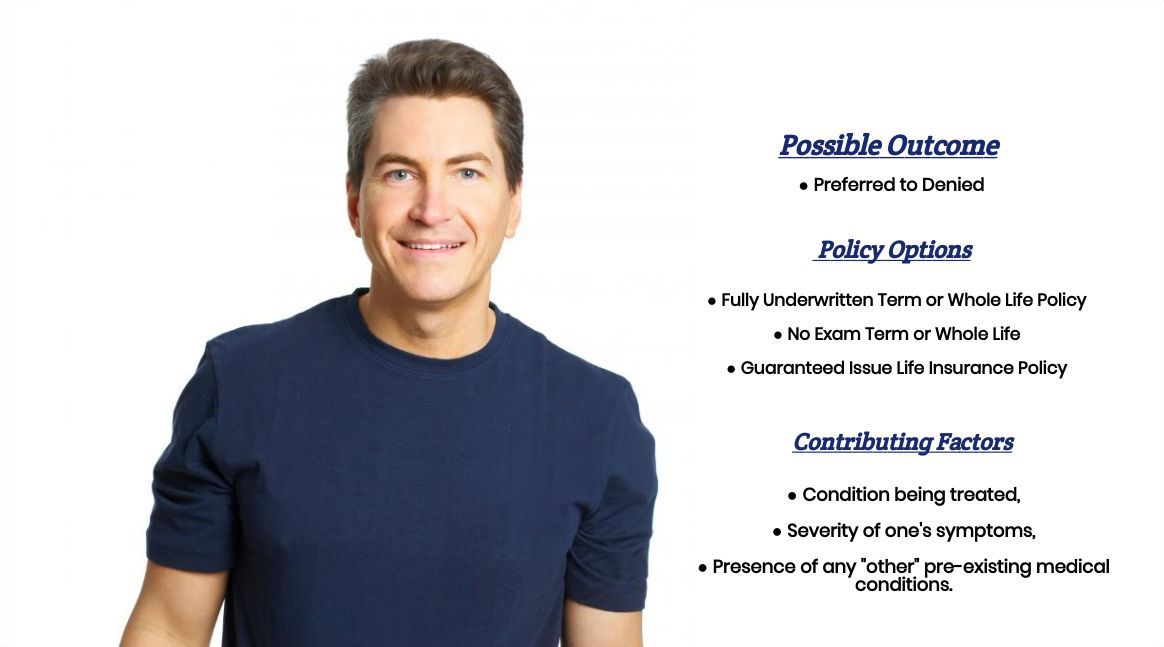

Yes, individuals who have been prescribed Lithium can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, some may even be able to qualify for a Standard Plus rate class depending on what pre-existing medical condition they are using their Lithium to treat.

Why do life insurance companies care if I’ve been prescribed Lithium?

The main reason why life insurance companies “care” if an individual has been prescribed Lithium is because while it is true that Lithium can be used to treat a wide variety of different pre-existing medical conditions, at the end of the day, most of those conditions are pretty serious!

And while…

Your particular situation might not be one that is going to cause a life insurance company to “stress” out too bad, until an insurance underwriter learns more about your particular situation, they’re usually going to assume the worst. This is why, if you have been prescribed Lithium in the past, you’re going to want to make sure that you do choose to apply for a “traditional” term or whole life insurance policy (a policy that will require a medical exam) and you choose to do so with a life insurance professional who is experienced in helping folks like yourself get insured.

What kind of information will the insurance companies ask me or be interested in?

Now it’s important to understand that regardless of whether or not you’ve been prescribed Lithium, in general, most life insurance companies are going to want to as you a lot of questions. Many are obviously going to be “health” related, but there also are going to be a lot that are going to focus on “lifestyle” choices as well.

And because…

Lithium can be used to treat such a wide variety of different medical conditions, rather that list 100’s of different of questions that they “might” ask, we rather focus on questions that they’ll “probably” ask which should be the same regardless of “why” you’ve been prescribed Lithium because at the end of the day they’re going to cover most of the factors a life insurance company is going to be interested in as well as give some insight on how “serious” your underlying pre-existing medical condition may be.

Common questions you’ll likely be asked may include:

- When where you first prescribed Lithium?

- Who prescribed your Lithium? A general practitioner or a specialist?

- Why have you been prescribed Lithium?

- Have you been given a definitive diagnosis?

- Are you taking any additional prescription medications?

- Have any of your prescription medications changed in any way within the past 12 months?

- In the past 2 years, have you been admitted to a hospital for any reason?

- Aside from using medications, are you currently receiving any other therapeutic measures or techniques?

- In the past 12 months, have you used any tobacco or nicotine products?

- Have you been diagnosed with cancer, heart disease, diabetes or depression?

- Have you ever suffered from a heart attack or stroke?

- What is your current height and weight?

- Have you ever been convicted of a felony or misdemeanor?

- Do you have any issues with your driving record? Issues such as multiple moving violations, DUI’s or a suspended license?

- Do you actively participate or plan on participating in any dangerous hobbies?

- Do you have any set plans to travel outside of the United States within the next year?

- In the past 2 years, have you applied for bankruptcy?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

What rate (or price) can I qualify for?

Now as you can see, there are a lot of factors that can come into play when determining what kind of “rate” that an individual can qualify for. And the truth is, at the end of the day, only a life insurance company will know for sure what kind of “rate” you might be able to qualify for since they are the only ones that can make decision for us.

That said however…

There are some “assumptions” that we here at IBUSA like to make so that we don’t find ourselves “over promising” a rate quote that simply isn’t a realist possibility for an individual. For this reason, when we are approached by a potential client who has been prescribed Lithium in the past, we generally assume that the “best” rate that he or she will be able to qualify for is a Standard or “normal” rate and then work our way downwards depending on the severity of one’s condition.

Now…

This doesn’t always mean that we’ll work our way down, it just means that we prefer to start out quoting process at a Standard rate so that our clients have a “realistic” expectation and sometimes get a pleasant surprise when they are actually approved by a life insurance company at a better rate than we had anticipated!

Which brings us…

To the last topic that we wanted to take a moment and discuss with you here in this article because, since you have already been prescribed Lithium and because you’ve already been diagnosed with some kind of pre-existing medical condition, there really isn’t much you can do about that. But, there are some other “things” that you might be able to do to help improve your chances at being able to qualify for the “best” life insurance policy for you!

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance profession who will work as an advocate for you.

Such an agent…

Will not only help guide you through the application process but also be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now does it?

Lastly…

You’ll want to make sure that you’re completely honest with your life insurance agent prior to applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best”

So, what are you waiting for? Give us a call today and see what we can do for you!