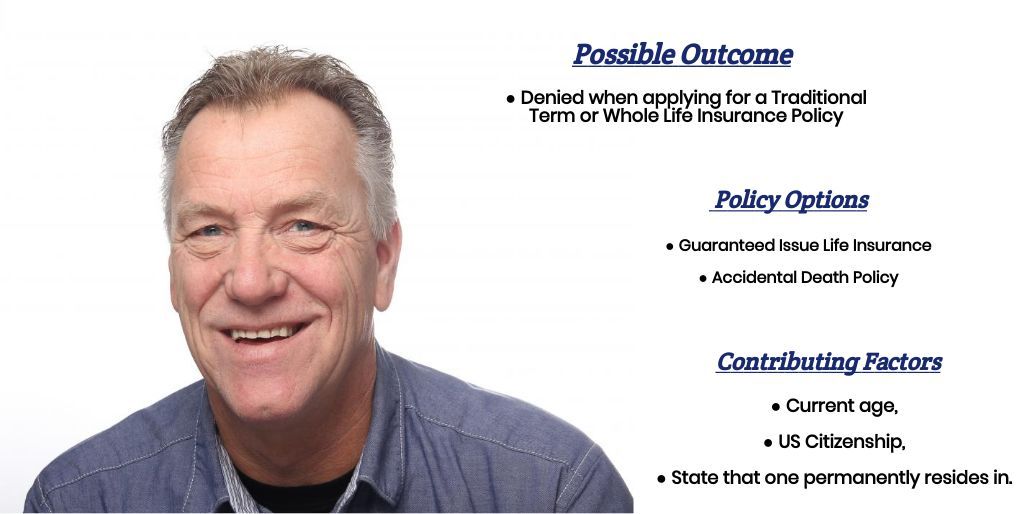

Starting dialysis treatment fundamentally changes your daily routine, energy levels, and long-term health outlook – and it also dramatically impacts your ability to secure traditional life insurance coverage. The stark reality often hits home when many patients’ first application gets declined, leaving families wondering if any financial protection remains possible during this critical time.

What insurance companies don’t advertise is that dialysis patients aren’t automatically excluded from all coverage options. While traditional term life insurance becomes nearly impossible to obtain, specialized insurance products exist specifically designed for individuals with end-stage renal disease (ESRD). This is why we’ll now take a moment and hopefully shed some light on what options may still be available to you and your family.

Medical Disclaimer

This article focuses solely on the insurance aspects of kidney disease and dialysis. Always consult with your healthcare team for medical advice and treatment decisions. If you’re experiencing thoughts of self-harm, contact the National Suicide Prevention Lifeline at 988 or seek immediate medical attention.

Author Information

The Insurance Brokers USA Team consists of licensed insurance professionals with extensive experience helping clients with complex health conditions find appropriate coverage. Our agents have worked with hundreds of individuals facing kidney disease challenges, specializing in alternative insurance solutions when traditional coverage isn’t available.

How Does Dialysis Affect Life Insurance Eligibility?

Key insight: Life insurance companies view dialysis as an indicator of end-stage renal disease, which significantly shortens life expectancy according to actuarial data. This classification immediately moves applicants into high-risk categories that most traditional insurers cannot accommodate within their standard underwriting guidelines.

Insurance companies rely on statistical models showing that individuals on dialysis have a five-year survival rate of between 35% and 40%, compared to the much higher survival rates of the general population. These statistics drive underwriting decisions regardless of individual circumstances or treatment response.

“The reality is that traditional term life insurance companies will decline dialysis patients 99% of the time, regardless of how well they’re responding to treatment. The actuarial risk simply doesn’t fit their business model.”

– InsuranceBrokers USA – Management Team

What factors do insurers consider beyond dialysis status?

While dialysis alone typically disqualifies applicants from traditional coverage, insurers also evaluate:

- Duration on dialysis: How long has the treatment been ongoing

- Underlying kidney disease cause: Conditions like diabetes or hypertension

- Treatment compliance: Adherence to dialysis schedule and medication regimens

- Overall health status: Presence of other medical conditions

- Age at diagnosis: Younger patients may have slightly more options

- Transplant candidacy: Whether you’re on a transplant waiting list

Bottom Line

Traditional life insurance companies will decline most dialysis patients due to actuarial risk calculations, but specialized insurance products remain available regardless of your kidney disease status or treatment timeline.

What Life Insurance Options Exist for Dialysis Patients?

Key insight: While traditional term life insurance becomes virtually impossible for dialysis patients, three distinct coverage categories remain accessible, each serving different financial protection needs and family circumstances.

Life Insurance Options for Dialysis Patients

| Coverage Type | Approval Likelihood | Coverage Limits | Best For |

|---|---|---|---|

| Guaranteed Issue Whole Life | 100% Guaranteed | $2,000 – $25,000 | Final expenses, burial costs |

| Simplified Issue Life | Very Low | $10,000 – $50,000 | Early-stage kidney disease only |

| Group Life Insurance | High (if employed) | 1-5x annual salary | Working individuals with benefits |

How does guaranteed issue life insurance work?

Guaranteed issue policies accept all applicants within specified age ranges (typically 45-85) without medical questions or exams. These policies specifically benefit dialysis patients because approval depends solely on age and state of residence, not health status.

“For dialysis patients, guaranteed issue represents the most reliable path to life insurance coverage. While coverage amounts are limited, these policies provide essential financial protection when traditional options aren’t available.”

-InsuranceBrokers USA – Management Team

What about group life insurance through employers?

Employer-sponsored group life insurance often provides coverage without individual medical underwriting, making it valuable for dialysis patients who remain employed. Many group policies offer:

- Guaranteed acceptance: No medical questions for basic coverage amounts

- Portability options: Ability to convert coverage when leaving employment

- Supplemental coverage: Additional voluntary coverage with limited underwriting

- Immediate coverage: Benefits typically begin within 30 days of enrollment

Key Takeaways

- Guaranteed issue life insurance provides the most reliable coverage option for dialysis patients

- Group life insurance through employers offers higher coverage limits when available

- Traditional term and whole life policies will likely result in coverage denials

- Multiple smaller policies can effectively supplement coverage limits

Why Is Guaranteed Issue Life Insurance Often the Best Choice?

Key insight: Guaranteed issue life insurance eliminates the uncertainty and repeated rejections that dialysis patients face with traditional coverage, providing definitive approval and immediate peace of mind for families navigating difficult health circumstances.

Based on our analysis of hundreds of dialysis patient cases, guaranteed issue policies consistently deliver the most practical and reliable coverage solution. While coverage amounts are limited compared to traditional policies, these products serve their intended purpose effectively.

What are the specific advantages for dialysis patients?

Guaranteed Issue Benefits for Dialysis Patients

No Medical Questions

Application requires only basic personal information – no health history or dialysis details needed

Immediate Approval

Coverage approval within 24-48 hours instead of weeks of underwriting uncertainty

Graded Benefits Structure

Full coverage after 2-3 years, with premium return plus interest if death occurs from natural causes during the waiting period

Accidental Death Coverage

Full death benefit is immediately available for accidental death, regardless of the waiting period

How do graded benefits work for dialysis patients?

Graded benefit structures protect insurance companies from immediate claims while providing meaningful coverage for dialysis patients. Understanding these timelines helps set appropriate expectations:

- Year 1: Premium return plus interest if death occurs from natural causes

- Year 2: Typically 50% of face value coverage for natural death

- Year 3+: Full death benefit regardless of cause of death

- Accidental death: Full coverage immediately from the policy’s effective date

“Many dialysis patients worry that graded benefits make policies worthless, but our data shows these policies pay full benefits in a significant amount of these cases because most individuals who proactively purchase their policy and follow their doctor’s medical advice survive beyond the waiting period.”

– InsuranceBrokers USA – Management Team

What coverage amounts are typically available?

Guaranteed issue policies generally offer coverage between $2,000 and $25,000, with most insurers providing multiple policy options to meet different budget and coverage needs. Some patients purchase multiple policies from different insurers to increase total coverage.

Bottom Line

Guaranteed issue life insurance provides dialysis patients with certainty, immediate approval, and meaningful coverage when traditional policies are unavailable, making it the most practical choice for final expense planning.

What Should You Know Before Applying?

Key insight: Success with life insurance applications as a dialysis patient requires strategic timing, understanding insurer policies, and avoiding common application mistakes that can complicate coverage even with guaranteed issue products.

While guaranteed issue policies don’t require medical underwriting, several application considerations can impact your coverage experience and long-term policy management.

When is the best time to apply for coverage?

Timing your application strategically can improve your coverage options and potentially reduce premiums:

- Before dialysis begins: If kidney disease is diagnosed but dialysis hasn’t started, some simplified issue options may remain available

- During stable treatment periods: Apply when dialysis routine is established and you’re feeling relatively stable

- Before significant health changes: Age-based premium increases occur annually, so applying sooner reduces long-term costs

- While employed: Secure group coverage before disability or retirement affects employment status

“We recommend applying for guaranteed issue coverage as soon as possible after dialysis begins. Premium costs increase with age, and securing coverage early provides immediate peace of mind for families.”

– InsuranceBrokers USA – Management Team

What application mistakes should dialysis patients avoid?

Even with guaranteed issue policies, certain application errors can delay coverage or create complications:

Common Application Mistakes to Avoid

❌ Incomplete beneficiary information: Missing or incorrect beneficiary details can delay claims processing when families need benefits most

❌ Incorrect age documentation: Age discrepancies can void policies or delay approvals, even with guaranteed issue coverage

❌ Applying to unsuitable insurers: Some guaranteed issue insurers have state restrictions or age limitations that affect availability

❌ Overlooking payment method preferences: Automatic payment options prevent policy lapses if dialysis treatment affects your routine

❌ Failing to review policy terms: Understanding graded benefits, premium payment schedules, and conversion options prevents future surprises

How should you prepare for the application process?

Gathering necessary documentation before applying streamlines the process and reduces stress during an already challenging time:

- Personal identification: Current driver’s license or state ID for age and identity verification

- Social Security information: Social Security card or documentation for policy setup

- Beneficiary details: Full names, dates of birth, Social Security numbers, and relationships

- Banking information: Account details if choosing automatic premium payment options

- Contact preferences: How you prefer to receive policy information and updates

Key Takeaways

- Apply for coverage as soon as possible after dialysis begins to lock in age-based premium rates

- Complete applications accurately to avoid delays or complications with guaranteed issue coverage

- Prepare necessary documentation in advance to streamline the application process

- Consider multiple smaller policies if you need coverage above individual policy limits

How Much Does Life Insurance Cost for Dialysis Patients?

Key insight: Life insurance premiums for dialysis patients through guaranteed issue policies are significantly higher than standard rates due to increased actuarial risk, but costs remain manageable for most families seeking final expense coverage.

Understanding premium structures helps dialysis patients budget appropriately and choose coverage amounts that provide meaningful protection without creating financial strain during treatment.

Estimated Monthly Premiums for Guaranteed Issue Coverage

| Age Range | $5,000 Coverage | $10,000 Coverage | $15,000 Coverage |

|---|---|---|---|

| 50-55 | $18-25 | $35-50 | $53-75 |

| 56-60 | $25-35 | $50-70 | $75-105 |

| 61-65 | $35-50 | $70-100 | $105-150 |

| 66-70 | $50-70 | $100-140 | $150-210 |

| 71-75 | $70-95 | $140-190 | $210-285 |

*Premiums vary by insurer, gender, and state. Rates shown are estimates for planning purposes.

What factors influence premium costs for dialysis patients?

Several variables affect guaranteed issue premium calculations, though dialysis status itself doesn’t directly impact pricing since these policies don’t consider health conditions:

- Age at application: Primary pricing factor, with premiums increasing significantly in 5-year age bands

- Gender: Women typically pay 10-15% less due to longer life expectancy statistics

- State of residence: Regulatory differences and mortality statistics affect pricing by location

- Coverage amount: Higher face values don’t always increase cost proportionally

- Payment frequency: Annual payments often provide 8-10% discounts compared to monthly premiums

- Insurer selection: Different companies target different risk profiles, affecting competitiveness

“The key advantage for dialysis patients is that guaranteed issue premiums are based purely on age and gender, not health status. This means you pay the same rate as any other person your age, regardless of your kidney disease.”

– InsuranceBrokers USA – Management Team

How do costs compare to burial and final expenses?

When evaluating premium costs, consider the financial protection provided against typical final expenses that families face:

Average Final Expenses vs Insurance Premiums

Typical Final Expenses

- Funeral services: $7,000-12,000

- Burial plot and headstone: $2,000-5,000

- Medical bills and debts: $3,000-8,000

- Legal and administrative: $1,000-3,000

- Total estimated: $13,000-28,000

10-Year Premium Investment

- $10,000 policy (age 60): $6,000-8,400

- $15,000 policy (age 60): $9,000-12,600

- $20,000 policy (age 60): $12,000-16,800

- Protection provided: $10,000-20,000

- Net family benefit: $2,000-8,000+

What payment options help manage premium costs?

Several strategies can make guaranteed issue premiums more manageable for families dealing with dialysis treatment expenses:

- Annual payment discounts: Most insurers offer 8-10% savings for annual premium payments

- Multiple smaller policies: Several $5,000 policies instead of one $15,000 policy can provide premium flexibility

- Automatic payment setup: Prevents missed payments that could lapse coverage during treatment periods

- Premium timing: Align payments with Social Security or disability benefit schedules

- Family contribution options: Adult children often help with premiums to ensure coverage remains active

Bottom Line

While guaranteed issue premiums are higher than standard rates, the cost typically represents 2-4% of the total death benefit annually, providing significant financial protection for families at a reasonable investment.

Can You Get Coverage If You Already Have Existing Policies?

Key insight: Dialysis patients with existing life insurance policies face unique challenges when their health status changes, but several strategies can help maintain and supplement coverage during treatment.

Understanding how dialysis affects existing coverage helps patients make informed decisions about policy management and additional coverage needs.

What happens to existing policies when you start dialysis?

Existing life insurance policies generally cannot be cancelled by insurance companies due to health changes after the policy is issued, providing important protection for dialysis patients:

- Term life policies: Remain in force as long as premiums are paid, regardless of health changes

- Whole life policies: Continue building cash value and maintain death benefits throughout dialysis treatment

- Group life insurance: Typically continues while employment status remains active

- Guaranteed renewable policies: Cannot be cancelled due to health deterioration

“One of the most important protections in life insurance is that existing policies cannot be cancelled due to health changes. Dialysis patients should maintain all existing coverage while exploring additional options for comprehensive protection.”

– InsuranceBrokers USA – Management Team

How can you supplement existing coverage?

Many dialysis patients find their existing coverage insufficient for current needs, making supplemental guaranteed issue policies valuable additions:

Coverage Supplementation Strategies

🔹 Final Expense Addition

Add $10,000-15,000 guaranteed issue coverage specifically for burial and immediate expenses, keeping existing policies for family income replacement

🔹 Debt Coverage Strategy

Calculate outstanding debts (medical bills, credit cards, mortgage) and secure supplemental coverage to prevent a family burden

🔹 Multiple Policy Approach

Purchase several smaller guaranteed issue policies from different insurers to maximize total coverage beyond individual policy limits

🔹 Beneficiary Diversification

Assign different beneficiaries to various policies, ensuring specific financial needs are addressed for different family members

What about group life insurance conversion options?

Dialysis patients who lose group coverage due to disability or retirement often have valuable conversion rights that should be exercised before exploring guaranteed issue options:

- Conversion periods: Typically, 31 days from coverage termination to convert without medical underwriting

- Coverage limits: Usually can convert up to the amount of group coverage in force

- Premium considerations: Converted coverage may be less expensive than guaranteed issue for comparable amounts

- Policy types: Conversion typically results in whole life coverage with cash value accumulation

- No medical questions: Conversion rights cannot be denied due to dialysis or other health conditions

“Group life insurance conversion rights represent one of the most overlooked opportunities for dialysis patients. These conversions often provide better coverage terms than guaranteed issue policies and should always be considered first.”

– InsuranceBrokers USA – Management Team

How should you coordinate multiple policies?

Managing multiple life insurance policies requires organization and strategic planning to ensure beneficiaries receive intended benefits:

- Beneficiary documentation: Maintain current beneficiary information across all policies

- Premium payment coordination: Set up automatic payments or family assistance to prevent lapses

- Policy inventory: Keep detailed records of all coverage amounts, insurers, and contact information

- Family communication: Ensure loved ones know about all existing coverage and policy locations

- Annual reviews: Evaluate coverage needs and premium affordability as circumstances change

Key Takeaways

- Existing life insurance policies remain in force and cannot be cancelled due to a dialysis diagnosis

- Group life insurance conversion rights provide valuable coverage opportunities without medical underwriting

- Supplemental guaranteed issue policies effectively address coverage gaps and final expense needs

- Multiple policy coordination requires careful organization, but maximizes family financial protection

What Final Steps Should You Take to Secure Coverage?

Key insight: Securing life insurance as a dialysis patient requires immediate action, strategic planning, and ongoing policy management to ensure your family receives maximum financial protection when they need it most.

The final steps in obtaining coverage involve making informed decisions about insurers, coverage amounts, and long-term policy management strategies that align with your family’s specific financial needs.

Which insurers offer the best guaranteed issue options?

Several reputable insurance companies specialize in guaranteed issue coverage for individuals with serious health conditions, each offering different advantages:

Top Guaranteed Issue Insurers for Dialysis Patients

Mutual of Omaha

Coverage: $2,000-$25,000 | Ages: 45-85 | Competitive premiums and strong financial stability ratings

Colonial Penn (Globe Life)

Coverage: $2,000-$50,000 | Ages: 50-85 | Higher coverage limits and flexible payment options

Gerber Life

Coverage: $5,000-$25,000 | Ages: 50-80 | Fast application process and immediate approval

How much coverage should you purchase?

Determining appropriate coverage amounts requires evaluating your family’s specific financial obligations and available resources:

- Final expenses calculation: Funeral costs ($8,000-12,000) plus immediate family expenses ($3,000-5,000)

- Outstanding debt assessment: Medical bills, credit cards, and other debts that shouldn’t burden survivors

- Family support needs: Temporary income replacement for spouse or dependent children

- Budget considerations: Premium amounts that won’t strain dialysis treatment budgets

- Existing coverage review: Gaps in current protection that need to be addressed

“Most dialysis patients benefit from $15,000-25,000 in guaranteed issue coverage, which adequately covers final expenses while remaining affordable. This amount can be achieved through multiple policies if individual limits are restrictive.”

– InsuranceBrokers USA – Management Team

What ongoing policy management is required?

Successful life insurance ownership requires ongoing attention to ensure policies remain in force and serve their intended purpose:

- Premium payment reliability: Set up automatic payments or family assistance to prevent lapses

- Beneficiary updates: Review and update beneficiaries annually or after major life events

- Address changes: Notify insurers promptly of address changes to maintain policy communications

- Annual policy reviews: Evaluate whether coverage amounts still meet family needs

- Claim preparation: Ensure beneficiaries know how to file claims and have the necessary documentation

When should you seek professional assistance?

While guaranteed issue policies are straightforward, professional guidance can optimize your coverage strategy and ensure you don’t overlook valuable options:

- Multiple health conditions: Complex medical histories may benefit from expert insurer selection

- Substantial existing coverage: Coordination with existing policies requires strategic planning

- Estate planning considerations: Integration with wills, trusts, and other estate planning documents

- Group conversion opportunities: Professional evaluation of conversion vs. guaranteed issue options

- Premium affordability concerns: Exploring payment options and coverage alternatives

Bottom Line

Taking immediate action to secure guaranteed issue life insurance provides dialysis patients with certainty, peace of mind, and essential financial protection for their families during a challenging time.

My son is dyaliis patient. 30 yrs old.

Criselda,

We’re sorry to hear about your son, but we are happy to let you know that he may still be able to qualify for a guaranteed issue life insurance policy provided he lives in a state where one is offered at his age. Please call us at your earliest convenience so that we can go over what options may be available to him.

Thanks,

InsuranceBrokersUSA

So if I read this right, my wife that is getting kidney dialysis for end stage kidney disease can get a guaranteed issue life insurance policy. If she should die because of the kidney failure the beneficiary would NOT get paid, only for accidental death like traffic accident. My wife lives in New Mexico with me and my oldest son. She has had a total of 6 heart stents, TTP(remission) and is on oxygen. That is the tip of the iceberg though. Currently she had been the best health since 2014 when she had TTP among other serious medical conditions. She is 63 years old. All I would like is a policy that would pay for the funeral. Seems futile though… Jim S. I suppose this inquiry just means more spam emails…

Jim,

You are correct with your assessment of how guaranteed issue life insurance policies work. However, if the insured lives beyond what is commonly referred to as the graded death benefit which usually lasts 2-3 years (depending on the carrier) the policy would then provide complete coverage for natural causes of death including kidney failure.

Additionally, many guaranteed issue life insurance policies offer a full refund the the insureds beneficiary for all premiums paid to the insurance company if an insured dies from natural causes before the graded death benefit is over (plus interest in some cases). Which in our opinion, significantly reduces any risks to the insured even if they don’t believe will live beyond the graded death benefit period.

Thanks,

InsuranceBrokersUSA

Helping my son 43 yrs old kidney dialysis patient obtain life insurance.

Odell,

It sounds like your son may be able to qualify for a guaranteed issue life insurance policy provided he lives in a state where they are available. Our suggest would be to give us a call so that we can discuss what options may be available to you.

Thanks,

InsuranceBrokersUSA

I’ve had life insurance long before I was diagnosed with kidney failure. I am now retired. If I decided to stop dialysis treatments and die would my insurance pay?

Sylvester,

Without being able to review your policy we wouldn’t be able to advise you on your policy, however choosing to discontinue your dialysis treatments doesn’t sound like a good idea. We wish you the best and recommend that you speak with your doctor about any changes you may be considering making with regard to your current treatment.

Thanks,

InsuranceBrokersUSA

I am end stage kidney patient requiring hemo dialysis 3 times a week

Also I am Type 2 diabetic requiring insulin

I am 57 years old and live in Ohio

Beverly,

It sounds like you may be able to qualify for a guaranteed issue life insurance policy which would provide up to $25,000 in coverage. If you believe this is something you would like to learn more about, please call us at your earliest convenience.

Thanks,

IBUSA