In this article, we wanted to take a moment and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Cialis (Tadalafil) to treat a variety of different medical conditions, including

- Erectile dysfunction,

- Benign prostatic hyperplasia (enlarged prostate)

- And/or pulmonary arterial hypertension.

Questions that will be directly addressed will include:

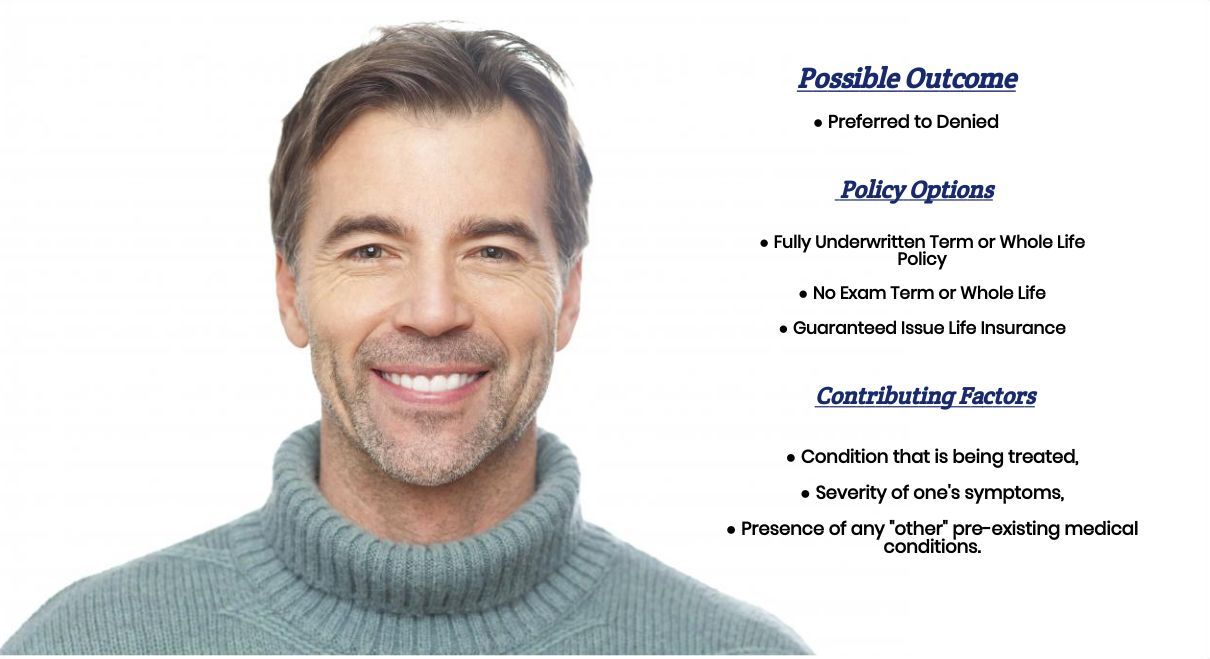

- Can I qualify for life insurance after I’ve been prescribed Cialis?

- Why do life insurance companies care if I’ve been prescribed Cialis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Cialis?

Yes, individuals who have been prescribed Cialis in the past or who are currently using Cialis can and often will qualify for a traditional term or whole life insurance policy. In fact, they may even be eligible for a no-medical-exam life insurance policy at a preferred rate!

The problem is…

While Cialis is most commonly used to treat conditions that won’t typically cause a life insurance underwriter to become too “nervous,” it is also used to treat folks who suffer from Pulmonary Arterial Hypertension. A condition that is usually considered “ineligible” for traditional coverage.

Why do life insurance companies care if I’ve been prescribed Cialis?

The main reason why an insurance company is going to “care” about the fact that an individual has been prescribed Cialis is that Cialis is a prescription medication that does more than help folks who are suffering from erectile dysfunction. It is also a medication that can be used to help those suffering from benign prostatic hyperplasia as well as pulmonary arterial hypertension.

And while…

Having been diagnosed with benign prostatic hyperplasia isn’t likely going to affect the outcome of your life insurance application; having been diagnosed with pulmonary arterial hypertension surely will. This is why before you are “approved” for a traditional term or whole life insurance policy, most (if not all) life insurance companies will want to ensure they fully understand…

“why?”

You’ve been prescribed Cialis, and you understand what kind of “risk” you pose to them should they deny you a life insurance policy.

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked about your Cialis prescription may include:

- When were you first prescribed Cialis?

- Why were you prescribed Cialis?

- Who prescribed your Cialis? A general practitioner or a specialist?

- Have you ever been diagnosed with prostate cancer?

- Have you ever been diagnosed with pulmonary arterial hypertension?

- In the past 12 months, have you used any tobacco or nicotine products?

- What are your current height and weight?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

What rate (or price) can I qualify for?

When it comes time to determine what kind of “rate” an individual may be able to qualify for once it has been determined that they have been prescribed Cialis in the past, you’ll generally find that either the Cialis prescription doesn’t affect the outcome of the application at all, or it makes a huge difference.

Now, for those who are simply using their Cialis to either treat their erectile dysfunction or an enlarged prostate (absent any signs of prostate cancer), most (if not all) life insurance companies will consider one’s Cialis prescription inconsequential. Or, in other words, not something to worry about.

That said, however…

If you are using your Cialis prescription to help you manage your pulmonary arterial hypertension, what you’re likely to find is that you will no longer be eligible for a traditional term or whole life insurance policy and that you will now need to consider purchasing an “alternative product” such as a guaranteed issue life insurance policy or an accidental death policy should you wish to provide some coverage for you and your family.

This brings us to the last topic we wanted to discuss here in this article, which is…

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true life insurance professional who will work as an advocate for them. Such an agent will help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

It would be best to be honest with your life insurance agent before applying for coverage because by doing so, you will help them narrow down the options that might be the “best. “

Now, can we help out everyone who has been prescribed Cialis?

No, probably not. But we can tell you that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies.

This way…

If someone can’t qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, call us!