In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance with Pericarditis.

Questions that will be addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Pericarditis?

- Why do life insurance companies care if I’ve been diagnosed with Pericarditis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance”?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I’ve been diagnosed with Pericarditis?

Yes, individuals who have been diagnosed with can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, some may even be able to qualify for some of the best no-medical exam life insurance companies at a Preferred rate!

The only problem is…

There are several different “types” of Pericarditis that an individual can suffer from, and there are many reasons why someone might develop this condition. Which is why, before approving you a traditional term or whole life insurance policy, most (if not all) of the top-rated life insurance companies want to know a lot more about “why” you contracted Pericarditis and how “serious” your condition became before they will be willing to make any definitive decisions about your application.

Why do life insurance companies care if I’ve been diagnosed with Pericarditis?

Any time an individual has been diagnosed with a pre-existing medical condition related to the overall health of one’s heart, it’s pretty safe to say that most (if not all) life insurance companies will want to learn more about it.

And…

This is what we see when it comes to folks who have been diagnosed with Pericarditis, a term used to describe a condition whereby the thin sac-like tissue surrounding the heart becomes inflamed. For this reason, we wanted to take a moment to briefly describe Pericarditis and highlight some of its most common symptoms/complications so that we may better understand exactly what a life insurance underwriter will be looking for when deciding on your life insurance application.

Pericarditis Defined:

Pericarditis is when the pericardium (a sac-like tissue surrounding the heart) becomes inflamed. The purpose of the pericardium is to help hold the heart in place as it pumps within the body, allowing it to perform more efficiently. The main “types” of Pericarditis include:

- Viral or bacterial Pericarditis,

- Constrictive Pericarditis,

- Post-heart attack pericarditis,

- Chronic effusive Pericarditis,

- And Pericarditis following heart surgery.

Common symptoms may include:

- Heart palpitations,

- Shortness of breath when reclining,

- Low-grade fever,

- Chest pain.

Serious complications may include:

- Increased risk of infection,

- Cardiac Tamponade,

- Chronic constrictive Pericarditis.

The underlying cause of the Pericarditis will typically determine treatment options and may include certain medications and/or surgical intervention.

Now, at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who are really good at helping folks with pre-existing medical conditions like this one find and qualify for the life insurance coverage they are looking for.

But…

It’s not so great if you’re seeking answers to specific medical questions. In such cases, we recommend contacting an actual medical professional with the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked may include:

- When were you first diagnosed with Pericarditis?

- Who diagnosed your Pericarditis? A general practitioner or cardiologist?

- What symptoms led to your diagnosis?

- Have you been diagnosed with a particular “type” of Pericarditis?

- Viral or bacterial Pericarditis?

- Constrictive Pericarditis?

- Post-heart attack pericarditis?

- Chronic effusive Pericarditis?

- Or Pericarditis following heart surgery?

- How many times have you developed Pericarditis?

- Have you been diagnosed with any other pre-existing medical conditions?

- Have you been diagnosed with heart disease?

- Have you ever suffered from a heart attack or stroke?

- Are you currently taking any prescription medications?

- In the past two years, have you been admitted to a hospital for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

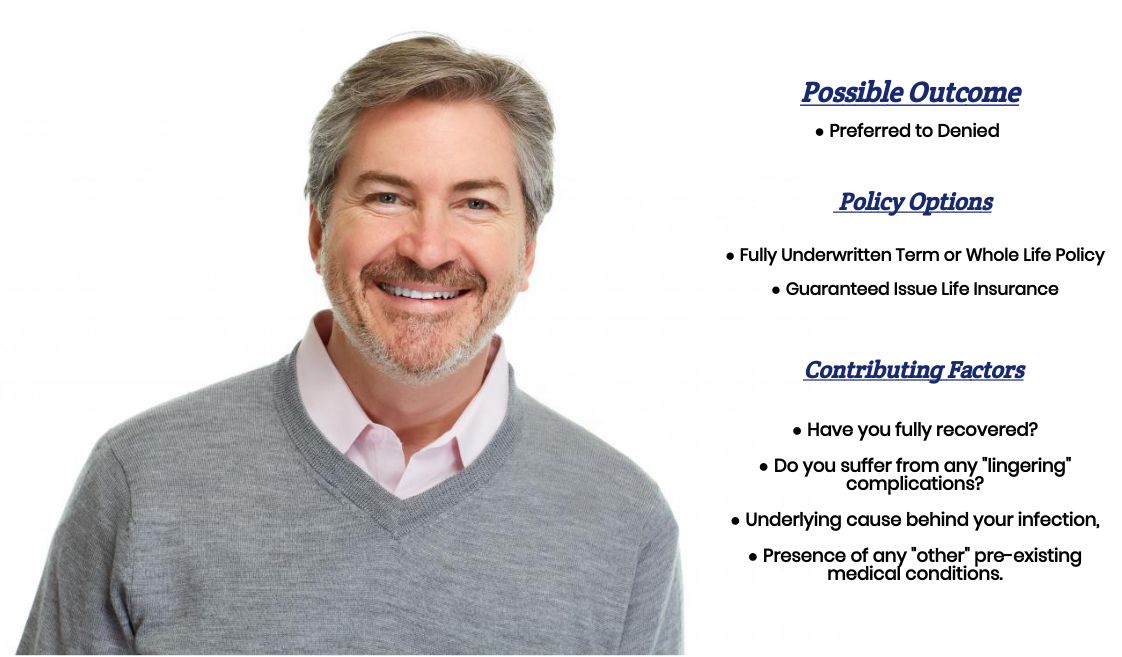

What rate (or price) can I qualify for?

As you can see, many variables can come into play when determining what kind of “rate” an individual diagnosed with Pericarditis might qualify for. This is why it’s pretty much impossible to know what kind of “rate” you might be able to qualify for without first speaking with you directly. That said, however, most individuals diagnosed with Pericarditis usually fall into one of three categories that we can make some “assumptions” about that will generally hold.

Category #1.

The first group of individuals that we’ll commonly encounter with Pericarditis will be those who develop this condition due to some “type” of viral or bacterial infection absent any other “serious” pre-existing medical conditions. These “types” of applicants will generally be considered eligible for coverage once fully recovered.

Additionally…

These “types” of applicants will generally find that most life insurance companies won’t use their previous Pericarditis diagnosis to discriminate against them, provided they don’t suffer from any lingering effects of their last diagnosis.

Category #2.

Applicants in this category will be those who have only suffered from a single episode of Pericarditis; however, they have also been diagnosed with some “other” pre-existing medical condition, which could potentially place them at risk of developing Pericarditis again in the future. These individuals “may” be able to qualify for a traditional term or whole life insurance policy; however, the underlying pre-existing medical condition will typically be the determining factor on whether that will be possible or not. When eligible, they will usually only be able to qualify for a “high risk” or “sub-standard” life insurance rate.

Category #3.

The last group of applicants that we’ll commonly encounter will include those who have suffered from multiple episodes of Pericarditis. In cases like these, what we’ll typically find is that the underlying pre-existing medical condition that is causing one to develop Pericarditis will be the primary determinant of what type of “rate” an individual will or won’t be able to qualify for and, when eligible, most will only be able to qualify for a “high risk” or “sub-standard” life insurance rate.

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with pre-existing medical conditions like yours. We are committed to helping all our clients find the “best” life insurance policy they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

How can I help ensure I get the “best life insurance”?

In our experience here at IBUSA, we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

Seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to help a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is precisely what you’ll find here at IBUSA!

Now, can we help out everyone previously diagnosed with Pericarditis?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well so that if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, call us!