In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Ativan or its generic form Lorazepam to treat their Anxiety.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Ativan?

- Why do life insurance companies care if I’ve been prescribed Ativan?

- What kind of information will the insurance companies ask me or be interested in?

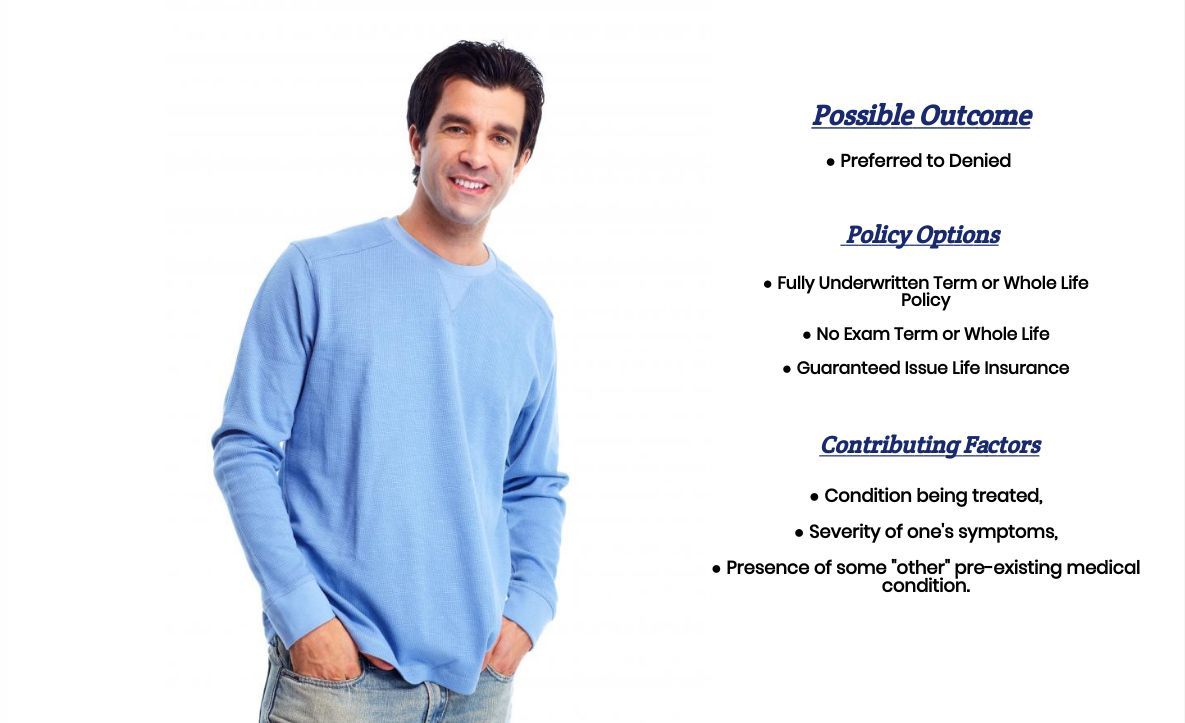

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Ativan?

The nice thing about being prescribed Ativan or its generic form Lorazepam is that it is not one of those “kinds” of medications that will automatically hurt your chances of qualifying for “traditional” life insurance. This means that even though you may have been prescribed Ativan in the past or are currently using Ativan right now, you should still “theoretically” be able to qualify for a Preferred or Preferred Plus rate class assuming that you would otherwise be healthy enough to qualify for such a rate.

The only difference now is that before “automatically” being considered eligible for such a “preferred” rate, most (if not all) life insurance companies are going to want to know a little bit more about your Ativan prescription prior to making any decisions about your life insurance application.

Why do life insurance companies care if I’ve been prescribed Ativan?

Life insurance companies aren’t all that concerned about the fact that you’ve been prescribed Ativan, what they are more concerned about is the underlying medical condition which Ativan is being used to treat. Mainly your Anxiety.

You see…

Folks who have been diagnosed with Anxiety may experience a wide variety of symptoms, including (but not limited too):

- Fatigue,

- Restlessness,

- Hypervigilance or irritability,

- Excessive worrying,

- Excessive fear,

- Feeling of impending doom,

- Insomnia

- Etc…

And while not everyone who has been diagnosed with Anxiety or been prescribed Ativan will experience any or all of these symptoms, it’s understandable why a life insurance company would want to know which symptoms you have before making a decision about your life insurance application… right?

This is why…

What you’re typically going to find is that once an insurance company learns that you’ve been prescribed Ativan in the past or have been diagnosed with Anxiety, they’re going to want to ask you a series of questions so that they might have a better understanding about how mild or severe your Anxiety may be.

What kind of information will the insurance companies ask me or be interested in?

In some situations, you may find that some life insurance companies may want to order medical records from your doctors prior to making a decision about your life insurance application.

This process is…

Both time consuming for the insurance company as well as costly since they are the ones that need to pay for the man-hours to acquire these forms as well as pay any type of “administrative fee” that is charged by a doctor’s office.

This is why…

The first thing that most life insurance companies will do is first ask you a series of questions about your Anxiety so that they may be able to better understand your condition prior to needing to actually order any medical records from your doctors. Common questions you might be asked may include:

- When were you first prescribed Ativan?

- Who prescribed your Ativan to you? A primary care physician or a specialist?

- How long have you been taking your Ativan?

- Is Ativan the only medication that you are taking to treat your Anxiety?

- In the past 12 months, has your Ativan prescription changed at all?

- Have you ever been hospitalized due to any of your anxiety symptoms?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

From here, most insurance companies will generally have a pretty good idea about whether or not they will need to order medical records before making a decision about your life insurance application. They’ll also have a pretty good idea about what “rate” you’ll probably qualify for.

What rate (or price) can I qualify for?

As we’ve previously stated, individuals using Ativan to treat mild to moderate cases of Anxiety should still theoretically be able to qualify for a “Preferred” life insurance rate provided that they choose to apply with a life insurance company that is known to be “lenient” when it comes to underwriting applicants who are applying with pre-existing medical conditions such as Anxiety.

Now for folks with more severe cases, what you’re generally going to find is that it’s all going to come down to “how severe” your case is. Things that will come into play are whether or not you’ve ever been hospitalized for your condition and whether or not you’ve been able to maintain steady employment over the years (if applicable).

What can I do to help ensure that I get the “best life insurance” for me?

Easily the best thing that you can do for yourself to help improve your chances of being able to find the best life insurance policy that you can qualify for is to first find a life insurance professional who is experienced at helping folks with anxiety qualify for coverage.

And…

Be sure that he or she has access to a wide variety of insurance products offered by a wide variety of insurance companies so that he or she isn’t limited to just a few options for you.

The good news…

Is that here at IBUSA, our insurance professionals have a ton of experience helping folks with a wide variety of pre-existing medical conditions like Anxiety find the coverage that they’re looking for at a great price because not only do they have the experience necessary, they also have access to dozens of different life insurance companies.

Which means that…

When it comes time to trying to find the “best life insurance company” for you, we don’t have to rely on just one or two different life insurance companies. We can simultaneously shop dozens of different options, thereby significantly increasing your odds of success!

Now, will we be able to help out everyone who has been prescribed Ativan?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well.

This way…

If someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to see what options might be available to you, just give us a call!