In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after having been diagnosed with Histoplasmosis.

Questions that will be addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Histoplasmosis?

- Why do life insurance companies care if I have been diagnosed with Histoplasmosis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I have been diagnosed with Histoplasmosis?

Yes, individuals who have been diagnosed with Histoplasmosis can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, some may even be able to qualify for a no exam term life insurance policy at a Preferred rate.

The only problem is…

That most (if not all) of the best life insurance companies are going to want to make sure that you have made a full and complete recovery from your Histoplasmosis infection and that you aren’t someone who may be at risk of suffering from this condition again due to your exposure to certain environmental factors or due to some other pre-existing medical condition which could make you “higher-risk” applicant.

Why do life insurance companies care if I have been diagnosed with Histoplasmosis?

Life insurance companies are going to “care” if an individual has been diagnosed with Histoplasmosis because it is a somewhat unusual lung infection, which can cause some pretty serious complications if not treated correctly and/or promptly.

This is why…

We wanted to take a moment and actually briefly describe what Histoplasmosis so that we might gain a better understanding of exactly what a life insurance underwriter will be looking for when making his or her decision about your life insurance application.

Histoplasmosis Defined:

Histoplasmosis is a lung infection that is caused by inhaling Histoplasma capsulatum fungal spores which can be found within soil samples all throughout the central, southeastern, and mid-Atlantic states. It is believed that in these areas, certain types of birds and bats carry the Histoplasma capsulatum fungi and deposit it in the soil through their fecal dropping (Translation… we’re breathing in their droppings and getting sick!).

Symptoms…

Of Acute Histoplasmosis will usually appear around 2 to 4 weeks after the initial exposure (sometimes sooner) and usually include:

- Flu-like symptoms,

- Headaches,

- Muscle pain,

- Loss of appetite,

- Difficulty breathing,

- Fatigue,

- Chest pain,

- Etc…

Significant complications may include:

- Acute Respiratory Distress Syndrome or ARDS,

- Cardiac complication including pericarditis,

- Adrenal insufficiency,

- Meningitis,

- Etc…

Fortunately…

When treatment is deemed necessary in severe infection or disseminated cases, use of antifungal medications, including Itraconazole, fluconazole, and amphotericin B will usually be able to significantly reduce one’s symptoms and shorten the amount of time required to heal from this infection.

Now…

Before anyone gets too upset or beings complaining about the simplicity of the definitions that we’re using here, it’s important to understand that we here at IBUSA aren’t medical experts of doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like the ones described above find and qualify for coverage.

Which means that…

Because we’re not going to be the one “diagnosing” your condition and certainly not the one’s treating it, all we need to do is understand what Histoplasmosis is and how a life insurance underwriter is going to consider you as a potential “risk.” The good news is that despite how simply our definitions are, this is something that we actually have down pat!

Which is why…

When we are approached by an individual who has been diagnosed Histoplasmosis, we’re going to know right away what questions a life insurance underwriter is going to want to know the answers too before he or she will be willing to make any kind of decision about the outcome of your life insurance application.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked may include:

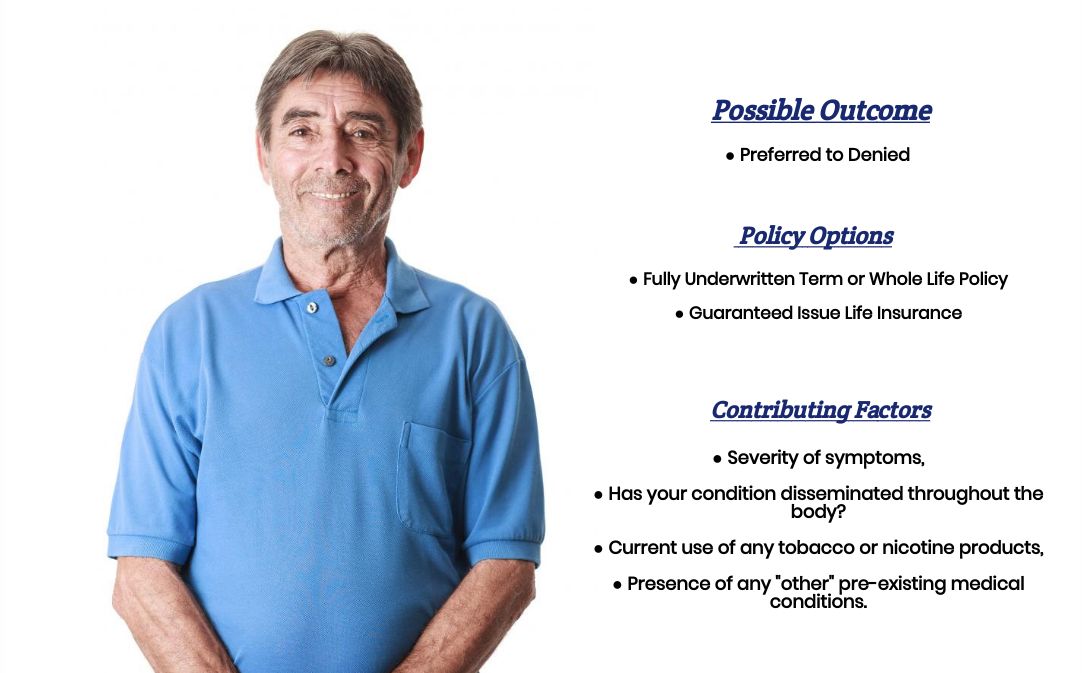

- When were you first diagnosed with Histoplasmosis?

- Who diagnosed your Histoplasmosis? A general practitioner or a specialist?

- What symptoms led to your diagnosis?

- Do you know how you contracted Histoplasmosis?

- Do you have a hobby or job that may put you at risk of being exposed to Histoplasmosis?

- How many times have you ever contracted Histoplasmosis?

- Have you been previously diagnosed with any pre-existing medical conditions which could put you at risk of developing Histoplasmosis?

- Conditions such as:

-

- HIV or AIDS?

- Previous organ transplant recipient?

- Use of any immunosuppressive medications?

- How did you treat your Histoplasmosis?

- Do you still suffer from any symptoms of your previous infection?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

-

What rate (or price) can I qualify for?

As you can see, there are a lot of factors that can come into play when trying to determine what kind of “rate” an individual might be able to qualify for after they have been diagnosed with Histoplasmosis. This is why it’s pretty much impossible to know what kind of “rate” you might be able to qualify for without first speaking with you directly.

That said however…

There are a few “assumptions” that we can make that will generally hold true about folks who have been diagnosed Histoplasmosis and are looking to qualify for a traditional life insurance policy.

For example…

I’s reasonable to assume that if you only suffered from a “mild” case of Histoplasmosis, that was limited to just a “lung infection” and you’ve remained symptom-free for a minimum of 6 months since your last date of treatment, you should “theoretically” still be able to qualify for a Standard or Better rate assuming that you would otherwise be eligible.

As for the rest…

Of folks who may have developed a more “serious” case of Histoplasmosis that may have disseminated to other portions of the body other than just the lungs, it’s still possible that you may be able to qualify for a traditional term or whole life insurance policy only now most (if not all) life insurance companies would prefer to see that you have remained symptom-free for a minimum of one year since your last date of treatment.

Additionally…

Folks in this situation will still likely only be able to qualify for a “sub-standard” rate at best. This means that these folks will need to be particularly careful with whom they ultimately decide to apply because not all life insurance companies are going to have similar pricing at these “high-risk” categories.

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy that they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that usually the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

And seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to helping a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is exactly what you’re going to find here at IBUSA.

Now, will we be able to help out everyone who has been previously diagnosed with Histoplasmosis?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that in the event that someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.