In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after having been diagnosed with bone marrow failure.

- Can I qualify for life insurance if I have been diagnosed with bone marrow failure?

- Why do life insurance companies care if I have been diagnosed with bone marrow failure?

- What kind of information will the insurance companies ask me or be interested in?

- What “rate” can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I have been diagnosed with bone marrow failure?

Yes, individuals who have been diagnosed with Bone Marrow Failure can and sometimes will be able to qualify for a traditional term or whole life insurance policy. The only problem is that this will only apply to those who have recovered from their Bone Marrow Failure and can demonstrate that they have fully recovered for a minimum of one year.

Why do life insurance companies care if I have been diagnosed with bone marrow failure?

To understand why a life insurance company might “care” if any individual has been diagnosed with bone marrow failure, it’s important to understand that “bone marrow” is the place where new blood cells are produced.

Which means that…

When bone marrow failure occurs, there are a lot of “bad things” that can follow. Bad things such as:

- Energy loss,

- Difficulty breathing, or shortness of breath,

- Uncontrolled bleeding,

- Fatigue,

- Unexplained infections or increased susceptibility to infections,

- Etc…

Additionally…

While it may seem like the fact that one is suffering from bone marrow failure is the real problem, in many cases, bone marrow failure may only be a “symptom” of some kind of more serious pre-existing medical condition which will ultimately be the determining factor as to what “kind” of life insurance policy an individual might be able to qualify for and what “price” they may have to pay for that coverage.

Potential causes of bone marrow failure may include:

- Aplastic anemia,

- Myelodysplastic syndromes,

- Paroxysmal nocturnal hemoglobinuria,

- Large granular lymphocytic leukemia,

- Etc…

Which is why…

Before being approved for a traditional term or whole life insurance policy, even after it has been determined that you have recovered from your bone marrow failure, most (if not all) life insurance companies are going to want to ask you a series of medical questions about your bone marrow failure so that they can understand “why” you developed this condition as well as the likelihood of it one day returning thereby posing any “unacceptable” risk to them as the insurance company.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked about your bone marrow failure may include:

- When were you first diagnosed with bone marrow failure?

- Who diagnosed your bone marrow failure? A primary care physician or a specialist?

- What symptoms led to your bone marrow failure diagnosis?

- Are you currently suffering from any of these same symptoms?

- Do you know what caused your bone marrow failure?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you currently taking any prescription medications?

- Have you fully recovered from your bone marrow failure? If so, when was your last date of treatment?

- In the past two years, have you been hospitalized for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

Now, at this point…

We like to make a few things very clear about what services we offer here at IBUSA, because we want to give anyone the impression that we’re medical professionals or have any medical training. You see, all we are is a bunch of life insurance agents who just happen to be really good at helping folks find and qualify for the life insurance that they’re looking for!

So…

If you think you have a medical issue, don’t use us or the internet to diagnose yourself. After all, if you do and you’re correct, you’re still going to need to see the doctor, and if you’re wrong, the time you spend being your own doctor could really harm you!

All you want to…

Use this article for is to “prep” yourself for what it might be like to apply for a life insurance policy after you have been diagnosed with bone marrow failure… that’s it! This brings us to our next topic, which is…

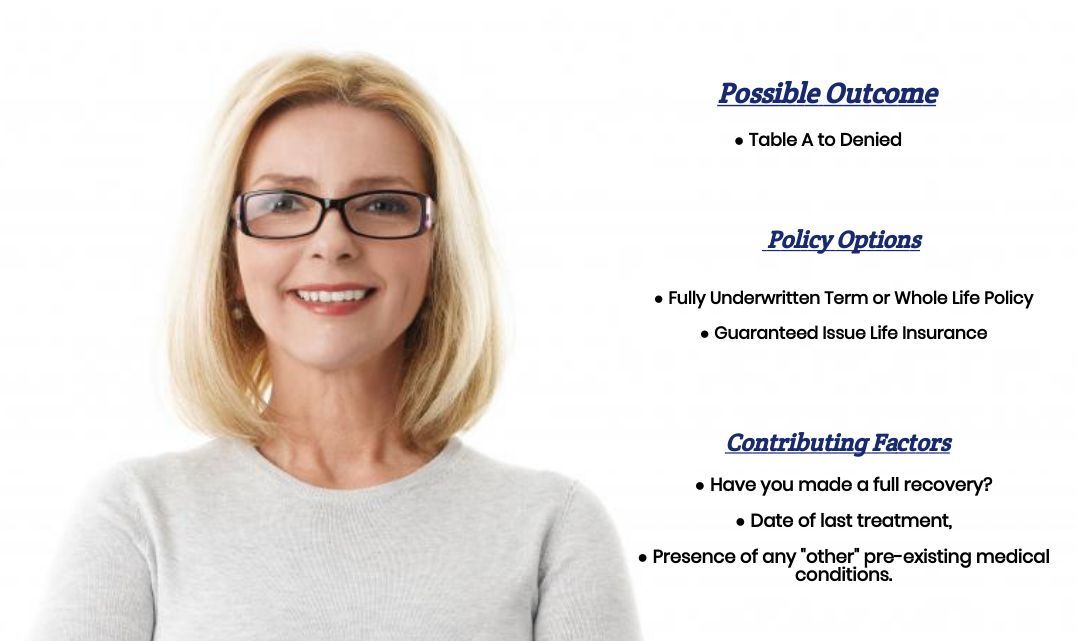

What “rate” can I qualify for?

When it comes time to determine what kind of “rate” an individual might qualify for after having been diagnosed with bone marrow failure, there are three main categories one might fall into:

Category One:

Are you still suffering from bone marrow failure? If so, or if you just recently recovered from your bone marrow failure (less than one year), what you’re generally going to find is that you will not be able to qualify for a traditional term or whole life insurance policy until you’ve reached that 1-year mark which means that you’ll either have to wait to apply for a traditional term or whole life insurance policy or seek out an “alternative product” like a guaranteed issue life insurance policy or an accidental death policy.

Category Two:

If your bone marrow failure is actually a symptom of some kind of “larger” more “serious” pre-existing medical condition, what you’re going to find is that this underlying medical condition that is causing you to suffer from bone marrow failure will ultimately be what determines the outcome of your life insurance application.

In cases like these…

We would encourage you to see if we have written a specific article about your condition or give us a call directly because without knowing “what” is causing you to suffer from bone marrow failure, we’re just not going to have any idea what you might be able to qualify for.

Category Three:

Folks in this category will have been diagnosed with and recovered from bone marrow failure over one year ago and not have some kind of “chronic” medical condition which will likely cause them to suffer from bone marrow failure again within the foreseeable future. In cases like these, they may be able to qualify for a traditional term or whole life insurance policy at a “high risk” rate.

Which isn’t…

The end of the world just means that these individuals will need to be more “selective” with which life insurance companies they ultimately decide to apply so that they can ensure their chances at being able to find the “best” life insurance policy for them.

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy that they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

And seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to help a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is exactly what you’re going to find here at IBUSA!