In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after being diagnosed with Gastritis.

Questions that will be directly addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Gastritis?

- Why do life insurance companies care if I’ve been diagnosed with Gastritis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I have been diagnosed with Gastritis?

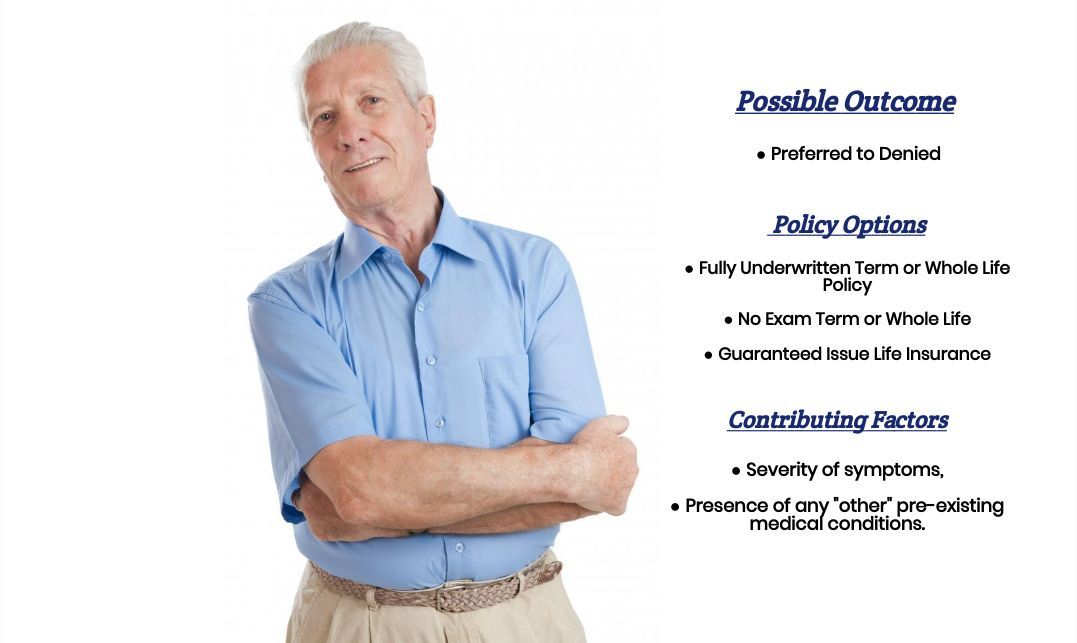

Yes, individuals who have been diagnosed with Gastritis can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, they may even be eligible for no exam term life insurance policy at a Preferred rate!

The only problem is that Gastritis isn’t always a pre-existing medical condition in and of itself. Instead, it can be a symptom of some other more “serious” pre-existing medical condition, which could potentially prevent you from being able to qualify for a traditional term or whole life insurance policy.

For this reason…

Most, if not all, of the best life insurance companies, will want to ask you a series of medical questions about your Gastritis so that they can get a better idea about whether your Gastritis is something they need to worry about!

Why do life insurance companies care if I’ve been diagnosed with Gastritis?

As a general rule of thumb, most life insurance companies aren’t worried that you’ve been previously diagnosed with Gastritis. After all, ask anyone who has suffered from Gastritis, and they’ll be sure to tell you that it’s not a whole lot of fun! This is why most folks who are diagnosed with Gastritis do an excellent job at treating their condition and minimizing the effects that it has on them on a daily basis!

It’s also why…

Rather than be concerned about the fact that you have been diagnosed with Gastritis, what worries a life insurance company more is “why” have you been diagnosed with Gastritis or “what” is causing you to suffer from Gastritis? Is it because you’ve been “infected” by the H. pylori bacteria? Or is it because you’ve been diagnosed with some other kind of pre-existing medical condition, such as:

Or isolated granulomatosis? That’s the real question and why we want to take a brief moment and discuss precisely what Gastritis is and highlight some of the most common symptoms that a life insurance underwriter will be looking for while making their decision.

Gastritis Defined:

Gastritis is a term used to describe an inflammation of the stomach’s protective lining. Individuals may suffer from Acute Gastritis, whereby their inflammation “comes on” suddenly, or they may suffer from Chronic or Erosive Gastritis.

Erosive Gastritis…

It is the least common of the third and generally considered the most “serious” because it will often cause more damage to the stomach lining and will usually manifest itself with bleeding within the stomach itself.

Common symptoms of Gastritis may include:

- Abdominal pain,

- Abdominal bleeding,

- Burning or “gnawing” feeling in the stomach between meals or while sleeping,

- Indigestion,

- Hiccups,

- Nausea or vomiting,

- Loss of appetite,

- Etc…

Fortunately, Gastritis is a condition that can be treated. In most cases, those suffering from Acute Gastritis will often be able to make a complete recovery with little or no complications. As for those who may suffer from Chronic Gastritis, what you’ll commonly find is that symptoms and the severity of symptoms will vary significantly from one patient to the next, which is why it’s important always to seek frequent medical advice when trying to treat this condition.

“This brings us to an important point we think we ought to mention.”

First…

If you have a medical issue, don’t use the internet to diagnose yourself. After all, if you do and you’re correct, you’re still going to need to see the doctor, and if you’re wrong, the time you spend being your doctor could harm yourself!

Second…

Nobody here at IBUSA is medically trained; we’re certainly not doctors. We are all a bunch of life insurance agents who just happened to be good at helping individuals find and qualify for the life insurance they’re looking for. So please don’t mistake any of the medical information we discuss as medical advice because it’s not!

We’re just trying to “prep” you for what it might be like to apply for a life insurance policy after you have been diagnosed with Gastritis, that’s it! This brings us to our next topic, which is…

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked may include:

- When were you first diagnosed with Gastritis?

- Who diagnosed your Gastritis? A general practitioner or a specialist?

- What symptoms led to your diagnosis?

- Have you been diagnosed with a specific “type” of Gastritis?

- Do you know what caused or is causing your Gastritis?

- What treatment options have you pursued?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you currently taking any prescription medications?

- In the past two years, have you been admitted to a hospital for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any disability benefits?

What rate (or price) can I qualify for?

Now, as you can see, there are a lot of factors that can come into play when trying to determine what kind of “rate” you might be able to qualify for after being diagnosed with Gastritis. This is why it’s pretty much impossible to know what kind of “rate” you might be able to qualify for without first speaking with you for a few moments.

That said, however…

There are a few “assumptions” that we can make about someone who has been diagnosed with Gastritis, which will “generally” hold. For example, suppose you have been diagnosed with Acute Gastritis, which an H. pylori bacterial infection has probably caused, and you don’t suffer from any other pre-existing medical conditions. In that case, you may be eligible for a Preferred rate. Or, more accurately stated it would be best if you were considered eligible for whatever rate you would have been able to qualify for before being diagnosed with Gastritis.

As for the rest…

Of those who have either been diagnosed with Chronic or Erosive Gastritis, what you’re generally going to find is that the “best” case scenario for you will likely be being able to qualify for a Standard or “Normal” life insurance rate. However, we should point out that locking in a Standard rate will by no means be an “automatic” foregone conclusion. A lot of individuals in this situation will probably have to settle for a “high-risk” table rating.

The good news is…

Regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

And seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to help a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

Fortunately, this is precisely what you’ll find here at IBUSA!

Now, can we help out everyone previously diagnosed with Gastritis?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.