In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Meloxicam or one of the common brand names it is sold under, including:

- Comfort Pac-Meloxicam,

- Mobic,

Or Vivlodex to treat symptoms associated with either Osteoarthritis or Rheumatoid Arthritis. (See arthritis for more details)

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Meloxicam?

- Why do life insurance companies care if I’ve been prescribed Meloxicam?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been prescribed Meloxicam?

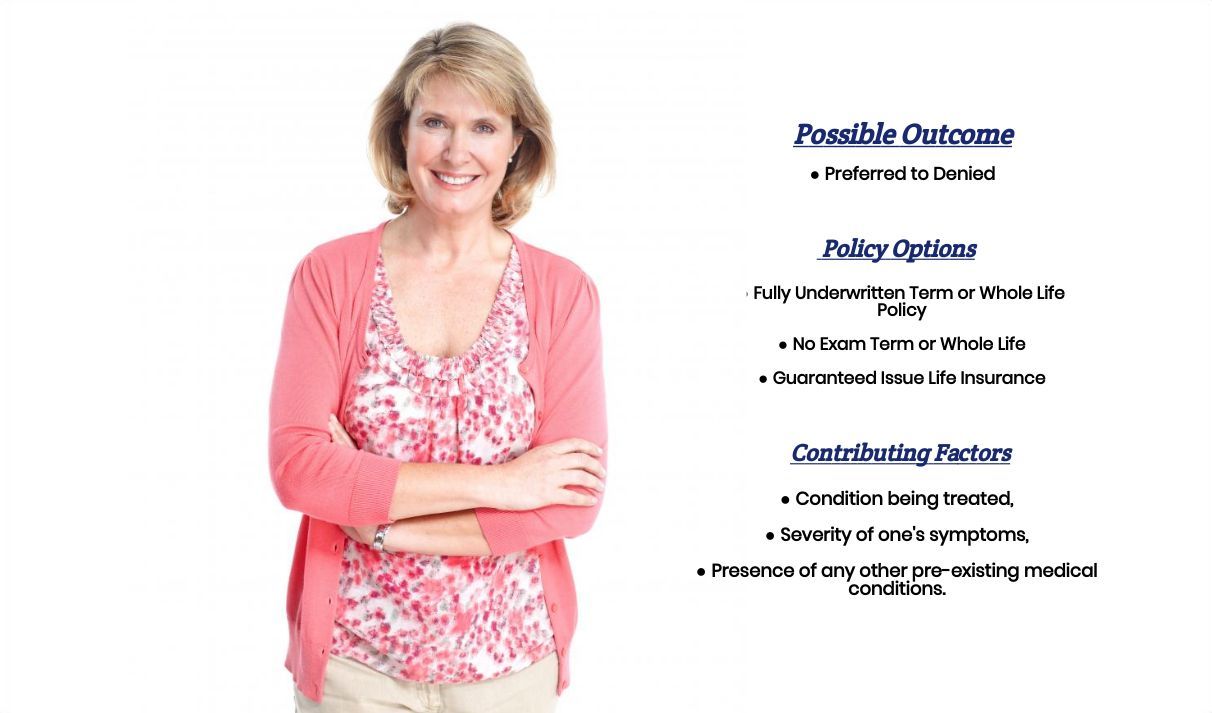

Yes, individuals who have been prescribed Meloxicam can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, they may even be able to qualify for a Preferred Plus. The problem is that because Meloxicam can be used to treat both osteoarthritis and rheumatoid arthritis, they are two very different pre-existing medical conditions that will be treated quite differently by most life insurance companies.

Why do life insurance companies care if I’ve been prescribed Meloxicam?

The main reason why most life insurance companies are going to “care” if you’ve been prescribed Meloxicam is because it is a prescription medication that can be used to help treat rheumatoid arthritis. And while most life insurance companies will be interested in those who have been prescribed Meloxicam to treat their osteoarthritis, it is those who have been diagnosed with rheumatoid arthritis that they will be the most nervous about.

This is why…

Prior to moving forward with your life insurance application, one should be prepared to answer a series of medical questions all about your Meloxicam prescription and about the underlying medical condition in which it is being used to treat.

What kind of information will the insurance companies ask me or be interested in?

- When were you first prescribed Meloxicam?

- Who prescribed your Meloxicam? A general practitioner or a specialist?

- Why have you been prescribed Meloxicam?

- Have been diagnosed with osteoarthritis?

- If so:

- How severe are your symptoms?

- Are you taking any additional medications to help you treat your arthritis?

- Have you been diagnosed with rheumatoid arthritits?

- If so:

- How severe are your symptoms?

- Are you taking any additional medications to help you treat your arthritis?

- Are you taking any NSAIDS medications?

- Have you also ever been prescribed Prednisone or Methotrexate?

- Do you have any issues with your driving record? Issues such as multiple moving violations, a DUI, or a suspended license?

- Have you used any tobacco or nicotine products in the past 12 months?

- Do you have any set plans to travel outside of the United States in the next year?

- Have you ever been convicted of a felony or misdemeanor?

- In the past 2 years, have you ever applied for bankruptcy?

- Are you currently working now?

- Have you ever applied for or received any form of disability benefits?

- If so:

- If so:

What rate (or price) can I qualify for?

Now as you can see, there are a lot of factors that can come into play when trying to determine what kind of “rate” an individual might be able to qualify for. This is why it’s pretty much impossible to know what kind of “rate” you might be eligible for without actually speaking with you directly.

That said however…

What we can tell you is that if you have only been diagnosed with osteoarthritis and you’re only using one or two medications to help you deal with it and you don’t seem to be suffering from too many “complications” as a result of your condition, there is a “reasonable” chance that you should still be considered “eligible” for a Preferred Plus rate.

Or, to put it another way…

Whatever rate you might have been eligible for PRIOR to being prescribed Meloxicam ought to be the same rate that you would be eligible for AFTER having been prescribed Meloxicam, which is great!

Where we run into trouble…

Is when an individual has been prescribed Meloxicam to help them treat their Rheumatoid Arthritis. In cases like these, it really doesn’t matter all that much that you’ve been prescribed Meloxicam because your Rheumatoid Arthritis diagnosis is going to be what ultimately determines what kind of rate you will be able to qualify for.

And unfortunately…

There really isn’t a test one can take to help a life insurance underwriter determine how “serious” your rheumatoid arthritis might be. This is why most life insurance companies will look at things like:

- What other medications, in addition to Meloxicam, have you been prescribed?

- How old were you when you were first diagnosed?

- And how debilitating has your condition become?

From there, they will make a “subjective” determination about what kind of “rate” you might be able to qualify for, typically limiting one to rates below what one would consider Standard.

This is why…

In cases like these, it becomes all the more important for an individual to make sure that they not only choose to work with an agent that is familiar with their disease but is also one that has plenty of options to choose from so they are limited to just one or two options particularly given the “subjective-ness” that can come into play with these “types” of cases. This brings us to the last topic that we wanted to take a moment and discuss with you here today, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance profession who will work as an advocate for you. Such an agent who can help guide you through the application process but also be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now does it?

Lastly…

You’ll want to make sure that you’re completely honest with your life insurance agent prior to applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best”

So, what are you waiting for? Give us a call today and see what we can do for you!