In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after they have been diagnosed with Cystic Fibrosis (CF).

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been diagnosed with Cystic Fibrosis?

- Why do life insurance companies care if I’ve been diagnosed with Cystic Fibrosis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been diagnosed with Cystic Fibrosis?

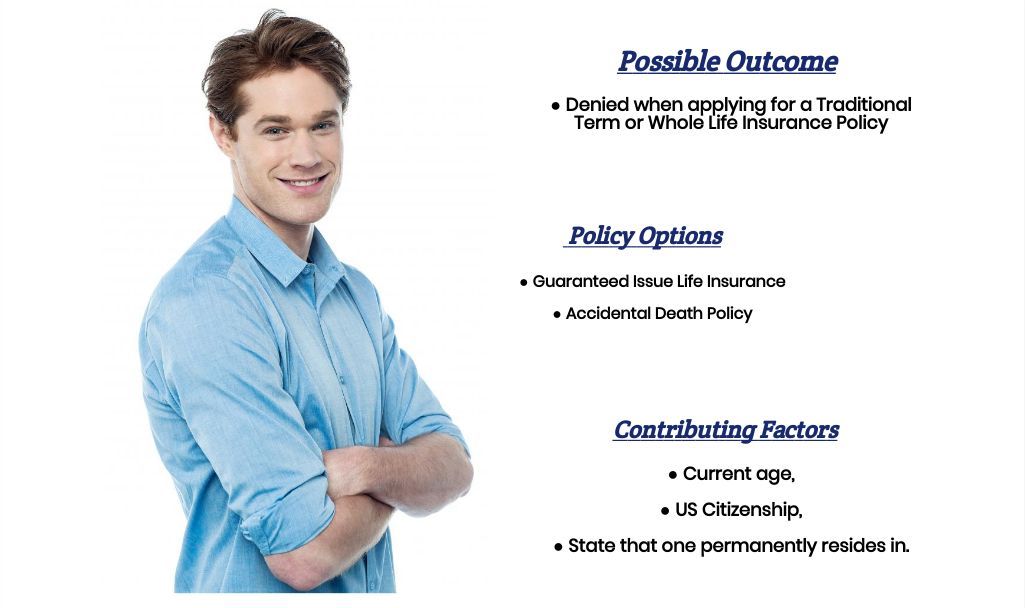

This is a tough one because if you had asked us a few months ago, we would have said “NO.” Individuals who have been diagnosed with Cystic Fibrosis will not be able to qualify for a traditional term or whole life insurance policy. The truth is this is still pretty much the case because the vast majority of life insurance companies are going to deny anyone who a “traditional” life insurance policy if they have been diagnosed with Cystic Fibrosis, which in the past would only leave someone two different options to consider.

The first would be…

A guaranteed-issue life insurance policy wouldn’t require someone to take a medical exam or answer any medical questions. It would also contain a GRADED DEATH BENEFIT and only allow those between the ages of 50 and 85 to apply (in most cases), which would usually be a deal-breaker for most folks with Cystic Fibrosis.

The second option….

We would usually turn to an Accidental Death Policy, which typically isn’t the greatest option either because these “types” of products aren’t TRUE life insurance policies because they provide coverage for ACCIDENTS. This means that if you were to die from a “natural” cause of death like a heart attack, a stroke, or, say, a complication associated with having been diagnosed with Cystic Fibrosis, these types of products would not pay a death benefit to your family.

This is why, when we would get a call from someone who has been diagnosed with Cystic Fibrosis, we here at IBUSA would find ourselves in a bit of a pickle because the truth was, we really wouldn’t have much that we could offer them that would meet their true needs.

That said, however…

Things have begun to change a “bit” within the life insurance industry. Now, we have some potential options that may be available to certain individuals diagnosed with Cystic Fibrosis, provided that they meet a rather “strict” criteria list and are only looking for a somewhat limited amount of TRUE life insurance coverage.

As a result…

Even though most life insurance companies are going to be unwilling to insure an individual who has been diagnosed with Cystic Fibrosis. That said, we here at IBUSA still like to cover all bases and see if there may be a chance for you to be still able to qualify for coverage with the one or two different insurance companies willing to provide coverage to those with CF.

Why do life insurance companies care if I’ve been diagnosed with Cystic Fibrosis?

Simply put, the main reason why life insurance companies are going to “care” if an individual has been diagnosed with Cystic Fibrosis is that Cystic Fibrosis is a severe pre-existing medical condition. And can potentially affect the lifespan of those affected by it.

Cystic Fibrosis Defined:

Cystic Fibrosis is a hereditary disease that affects the CFTR gene, which is responsible for making a protein that helps control the movement of salt and water in and out of one’s cells. As a result, those suffering from this condition will tend to have “issues” that will affect both their lungs and digestive system.

Common symptoms of Cystic Fibrosis may include:

- Salty tasting skin,

- Frequent coughing, wheezing,

- Increased susceptibility to pneumonia or sinusitis,

- Difficulty breathing,

- Large, smelly, and greasy bowel movements,

- Difficult gaining weight and/or failure to thrive.

But what really worries…

Most life insurance companies say that Cystic Fibrosis is a chronic progressive disease, which statistically shows that the majority of individuals suffering from this condition will encounter severe complications due to their disease by their late 30s or early 40s.

Now, before anyone gets upset or complains about the simplicity of the definitions we’re using here, it’s important to understand that we here at IBUSA aren’t medical experts in doors. All we are is a bunch of life insurance agents who are really good at helping folks with pre-existing medical conditions like Cystic Fibrosis find coverage they can qualify for.

Which means that…

Because we won’t be the ones “diagnosing” your condition and certainly not the ones helping you treat it, all we need to do is have a very “basic” understanding of your condition and what the life insurance companies will be most interested in.

What kind of information will the insurance companies ask me or be interested in?

If you have cystic Fibrosis, insurance companies will typically ask for detailed information about your medical history, including your diagnosis and treatment history, when you apply for life insurance. They will also likely ask about any other health issues you have and your lifestyle, including your diet, exercise habits, and any risky behaviors such as smoking or excessive alcohol consumption. Insurance companies will then use this information to assess your risk profile and determine the most appropriate coverage and premiums.

Having cystic Fibrosis may be considered a negative factor in this assessment, as it increases the risk of respiratory and digestive issues and can impact life expectancy. As a result, you may be charged higher premiums to compensate for the increased risk or be denied traditional coverage entirely.

Being honest and transparent when completing a life insurance application is important. Providing accurate and complete information will help the insurance company assess your risk profile and determine the most appropriate coverage and premiums for your situation.

It’s a good idea to know what is in your medical records and discuss your health history with your doctor before completing the application to ensure you have all the necessary information. When it comes time to “qualify” for coverage, your Cystic Fibrosis diagnosis will likely be the most significant factor in the underwriting process. And the truth is, the process for getting approved with Cystic Fibrosis can be somewhat “subjective.”

Which is why…

What we usually like to do is review some of the pros and Cons of the different life insurance companies that will be willing to provide coverage to those who have been diagnosed with Cystic Fibrosis and go over some of the “pricing” first to determine if one of these options might be a good fit for you.

From there…

We’ll usually try to get a better idea about how “serious” your cystic Fibrosis is and reach out to an underwriter to determine if you’ll have a realistic chance at qualifying for coverage. This way, you won’t need to spend a lot of time and energy if it doesn’t look like you have a realistic opportunity for success!

This brings us to the last topic we wanted to discuss in this article…

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true life insurance professional who will work as an advocate for them. Such an agent will help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

It would be best if you were completely honest with your life insurance agent before applying for coverage. By doing so, you will help them narrow down what options might be the “best.”

So, what are you waiting for? Give us a call today and see what we can do for you!

I am very interested in speaking with an agent.

Melissa,

We would love to have an opportunity to assist you in your needs, so please call us at 888-211-6171.

Thanks,

InsuranceBrokersUSA

My name is Ms Dabney . I’m looking to start a life insurance policy for my 18 years old son that had Cystic Fibrosis and Ashma and a 45000 dollar policy . If you help me out with this . Can you email me back with all the information for a 45000 dollar policy.

Ms. Dabney,

Thank you for reaching out. We understand the importance of securing a life insurance policy, especially given your son’s health condition. Please feel free to call us to discussw what types of insurance policies you son may be eligible for.

We’re here to help, and we look forward to assisting you.

InsuranceBrokersUSA