In this article, we wanted to take a moment to try to answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Dilantin or its generic form, Phenytoin, to treat various types of seizure disorders.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Dilantin?

- Why do life insurance companies care if I’ve been prescribed Dilantin?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Dilantin?

Because Dilantin is a prescription medication that is solely used to help folks who are suffering from a “seizure type” disorder, for the most part, it’s safe to assume that if you have been prescribed Dilantin in the past or are currently taking Dilantin now, you should still be considered eligible for a traditional life insurance product.

In fact, some may even be eligible for a no-medical exam life insurance policy at a preferred rate! This begs the question, why do life insurance companies even care if someone is taking Dilantin if it’s really not going to have much of an effect on their life insurance application?

Why do life insurance companies care if I’ve been prescribed Dilantin?

Unlike other prescription medications that can be habit-forming or have potentially serious side effects, Dilantin (for the most part) is a pretty safe medication for folks to take. And sure, it may not be all that pleasant to experience some of the side effects of this medication, such as:

- Headaches,

- Nausea,

- Constipation,

- Dizziness,

- Slurred speech,

- Etc…

Insurance underwriters (for the most part) aren’t necessarily going to be worried about any of these causing any serious harm.

Rather…

Life insurance underwriters are going to be much more concerned about “why” you’ve been diagnosed to treat Dilantin and whether this underlying pre-existing medical condition is something that they ought to be worried about or not. This is why before making any decision about the outcome of your life insurance application, they will first want to know answers to a series of questions so that they can get a better idea about the severity of your condition.

What kind of information will the insurance companies ask me or be interested in?

Before making any decisions about your life insurance application, insurance underwriters are going to want to ask you a series of questions so that they can first determine what kind of seizure disorder you may have as well as try and ascertain how “serious” it might be and how well it is being managed.

In order to accomplish this, most (if not all) life insurance companies are likely to ask you a question somewhat similar to this:

- How old were you when you first suffered from a seizure?

- What “type” of seizures do you suffer from?

- How often do you suffer from seizures?

- In the past 12 months, have you suffered from a seizure? And if so, how many seizures have you suffered from in the past 12 months?

- Is Dilantin the only medication that you’re using to treat your seizures?

- In the last 12 months, has your Dilantin prescription changed at all?

- Do you currently hold a valid driver’s license?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

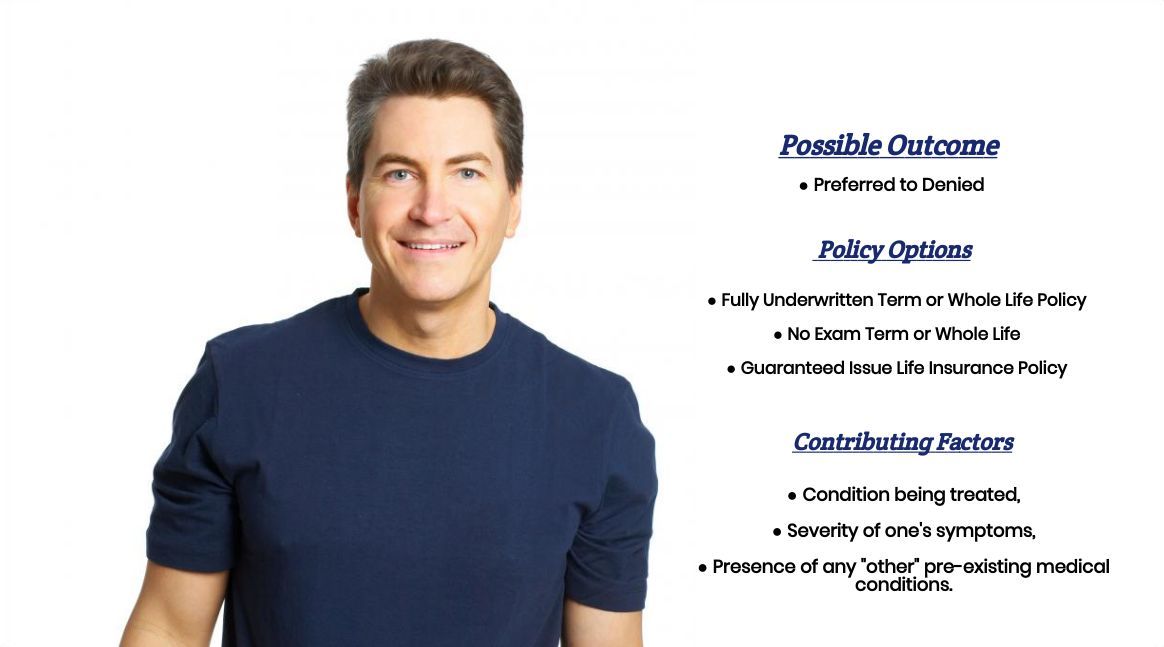

What rate (or price) can I qualify for?

Now, at this point, with the answers to these questions in hand, we here at IBUSA and the insurance underwriters will generally have a pretty good idea of both the “type” of life insurance you’ll be able to qualify for as well as what rate that you might be expected to pay.

And…

As we stated before, one of the “nice” things about being diagnosed with a “seizure disorder” is that provided that the condition isn’t preventing you from living a “normal” life, in theory, you should still be able to qualify for a Preferred rate.

Now we should note…

That just being able to qualify for a Preferred rate absent any pre-existing medical conditions such as a seizure disorder isn’t all that easy to do, but assuming that you would otherwise be eligible, having been prescribed Dilantin to treat seizures isn’t automatically going to preclude you from being able to qualify.

So, if your seizure disorder is making normal things like holding a full-time job or being able to retain your driver’s license; chances are you’re not going to qualify for a Preferred rate. In cases like these, we’d be more inclined to hope for a Standard rate or a high table rating at best. This brings us to the next section of our article, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experiences here at IBUSA, what we have found that seems to offer our clients the best opportunity for success is having plenty of options to choose from. That and having plenty of experience helping folks with pre-existing medical conditions find coverage that they can afford.

Additionally…

It’s important to be completely honest with the life insurance agent that you choose to apply for coverage with so that he or she can fully understand your situation and what you’re trying to achieve by purchasing a life insurance policy in the first place and be sure that this same agent has plenty of companies to pick and choose from when it comes time to apply.

After all…

The last thing that you want to have happened is for a great life insurance agent to try and place you with a life insurance company that just isn’t the “best” for you.

Now, will we be able to help out everyone who has been prescribed Dilantin?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well. This way, if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, just give us a call!