In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Cymbalta or its generic form Duloxetine to treat one’s depression or diabetic nerve pain.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Cymbalta?

- Why do life insurance companies care if I’ve been prescribed Cymbalta?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Cymbalta?

When it comes to understanding whether an individual will be able to qualify for a traditional life insurance policy after they have been prescribed Cymbalta (or its generic form Duloxetine), its really all going to come down to “why” an individual has been prescribed Cymbalta in the first place.

Was it…

Because you’ve been diagnosed with depression, in which case the insurance companies are going to want to know how serious your depression is and how it is affecting other aspects of your life.

Or were you…

Prescribed Cymbalta because you suffer from diabetic nerve pain, in which case the insurance companies are going to want to know more about why you are suffering from this symptom of diabetes and if its because your diabetes is simply out of control right now. Which brings us to our next question, which is…

Why do life insurance companies care if I’ve been prescribed Cymbalta?

The truth of the matter is that most life insurance companies aren’t really worried about the fact that you’ve been prescribed Cymbalta because, on its own, it is a pretty “safe” prescription medication that doesn’t have any “serious” side effects and is not the “type” of medication that one might abuse for the wrong reasons.

What makes insurance companies…

Nervous about folks who have been prescribed Cymbalta is the underlying medical condition being treated. You see, because Cymbalta can be used to treat both depression and/or diabetic never pain (two medical conditions which make life insurance companies nervous) what you’re generally going to find is that most (if not all) life insurance companies are going to want to know more about these underlying medical conditions prior to them being willing to approve one’s life insurance application. This brings us to our next question, which is…

What kind of information will the insurance companies ask me or be interested in?

The first thing that an insurance company is going to want to know about your Cymbalta use is:

“Why have you been prescribed Cymbalta?”

From there, they’ll then want to learn more about the underlying cause of why you have been prescribed Cymbalta so that they can get a better understanding of the “root” cause and make determinations from there.

Which means that…

If you’ve been diagnosed with depression, most life insurance companies are going to want to ask you questions like:

- When were you first diagnosed with depression?

- Who diagnosed your depression? A general practitioner or a psychiatrist?

- Is Cymbalta the only medication/treatment that you’re using to treat your depression?

- How often do you take your Cymbalta?

- How effective is it at treating your symptoms?

- In the past 12 months, has your prescription for Cymbalta changed?

- Have you ever been hospitalized for your depression?

- Have you ever considered or attempted suicide?

- Are you currently working now?

- In the past 12 months, have you applied for or received any forms of disability benefits?

Now, if you’re using your Cymbalta to treat diabetic nerve pain that is a direct result of your diabetes, what you’re going to find is that most (if not all) life insurance companies are going to want to ask you more specific questions directly related to your diabetes. Questions such as:

- What type of diabetes do you have?

- How old were you when you were first diagnosed with diabetes?

- What is your current height and weight?

- Do you use any tobacco or nicotine products?

- Do you test your daily blood sugar levels? And if so, what would you say your daily average is?

- When did you last have your A1C level tested, and what was that score?

- Aside from nerve pain, are you suffering from any other symptoms related to your diabetes?

- How well is Cymbalta working to control your diabetic nerve pain?

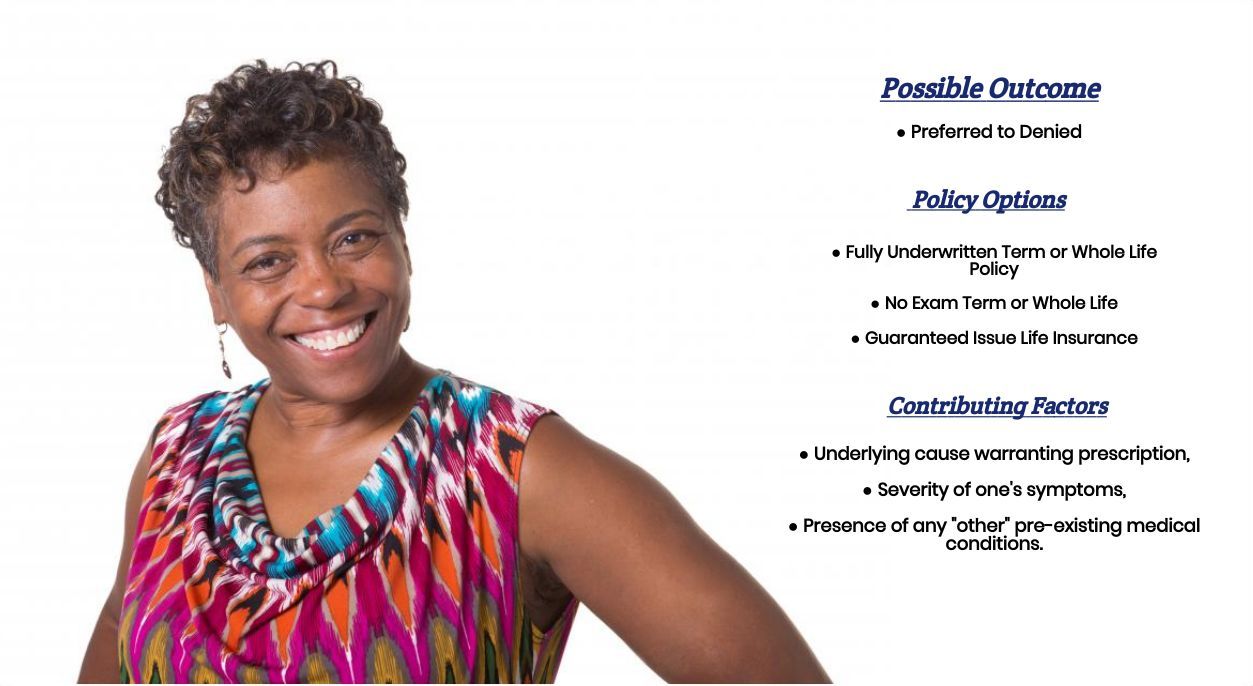

What rate (or price) can I qualify for?

When it comes time to determine what “rate” you may be able to qualify for once, it’s been determined that you’ve been prescribed Cymbalta, again it’s going to all come down to…

“why”

You’ve been prescribed Cymbalta and how well it is working towards controlling your symptoms of that underlying pre-existing medical condition.

The good news is…

That if you’re Cymbalta is being used to treat symptoms associated with depression, not only should you “theoretically” qualify for a traditional term or whole life insurance policy, you might even be able to qualify for a Preferred rate.

This is because...

Insurance companies have come to the understanding that there are a lot of folks out there who turn to prescription medications to help them deal with symptoms of depression who aren’t necessarily suffering from a “life-threatening” condition. They are simply using these medications to help improve the quality of their lives.

This is why…

We’ll often find many life insurance companies will approve folks who have been diagnosed with depression at a Preferred or at least a Standard rate assuming that their depression is under control, with a steady work history and haven’t required the need to be hospitalized. Now for those who do suffer from more severe cases of depression, it may still be possible to qualify for a traditional term or whole life insurance policy however, these cases will certainly be more challenging and will often require the need of having one’s full medical records review prior to approval.

Now, as for those taking Cymbalta to treat their diabetes…

What you’re usually going to find is that if you’re currently using Cymbalta to treat for diabetic nerve pain, its probably because you currently don’t have your diabetes well maintained. In cases like these, it’s going to be very difficult (if not impossible) to qualify for a traditional term or whole life insurance policy.

Now…

We could be wrong, and you’re simply using Cymbalta as a preventive medication to avoid any undesired pain associated with your diabetes. In which case, an insurance company will make consider this.

However…

In our experiences here at IBUSA, once someone has begun to suffer from these more “serious” symptoms associated with diabetes, its usually because they have very high blood sugar levels indicative of A1C level well and above 7.0 in which case being able to qualify for a traditional life insurance policy will be difficult even without having been prescribed Cymbalta.

But don’t fret…

Because here at IBUSA, we’re often surprised by the rates some of our clients may receive from an insurance company after we’ve submitted their life insurance application.

This is because…

When we quote our clients, we like to keep everyone’s expectations well-grounded and not make unrealistic promises only to be disappointed later down the road. It’s also why we work so hard to continually educate ourselves about the different life insurance products out there so that if there is an option that one might qualify for, we’re certainly going to do our best to be able to be able to offer it!

This brings us to our next question, which is…

What can I do to help ensure that I get the “best life insurance” for me?

Probably the best thing that you can do as a consumer to ensure that you’re able to find the “best” life insurance policy that you can qualify for is to be sure that you not only find a life insurance agent that is familiar with helping folks qualify for life insurance coverage after they’ve been diagnosed with a pre-existing medical condition like depression and/or diabetes (because it’s quite possible you might even have both) and has access to dozens of different life insurance companies to choose from.

This is because…

When it comes time to helping you find the “best” life insurance policy that you can qualify for, do you really want your life insurance agent to be limited to just a few options? Or would you rather that he or she had access to dozens of different companies, each competing for your business? In our experience having more options is almost always a better option.

Now, will we be able to help out everyone who has been prescribed Cymbalta?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well.

This way…

If someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to see what options might be available to you, just give us a call!