When your doctor mentions an “irregular heartbeat” or arrhythmia, the first concern is naturally treatment and lifestyle. But soon after, many people worry: will this heart condition make it impossible to get life insurance to protect my family?

The good news is that the life insurance industry has changed a lot in recent years. What might once have meant automatic denial now often leads to multiple coverage options—depending on the type of arrhythmia, your treatment response, and overall heart health. Our review of hundreds of cases shows that most people can secure meaningful coverage when they understand the process and work with knowledgeable agents.

This guide walks you through every option, from standard policies for well-managed conditions to specialized products for more complex cases. With clear insights, you can confidently choose coverage that safeguards your family’s financial future.

Table of Contents

- What Do Insurance Companies Need to Know About Your Arrhythmia?

- How Do Different Types of Arrhythmia Affect Coverage?

- What Coverage Options Are Available?

- How to Apply Successfully with Arrhythmia?

- What Will Life Insurance Cost with Arrhythmia?

- What Medical Records Do You Need?

- Which Companies Offer the Best Rates?

- Frequently Asked Questions

What Do Insurance Companies Need to Know About Your Arrhythmia?

Insurance underwriters evaluate arrhythmia cases based on specific medical factors that determine your cardiovascular risk profile. Understanding these evaluation criteria helps you prepare a stronger application and set realistic expectations for coverage outcomes.

Key Medical Factors Underwriters Examine

- Type and severity of arrhythmia: Companies distinguish between benign conditions like occasional PACs (premature atrial contractions) and serious disorders like ventricular tachycardia. The specific diagnosis significantly impacts your coverage classification.

- Underlying heart condition: Arrhythmias caused by structural heart disease receive different treatment than those with no identifiable cause. Underwriters carefully review echocardiograms, stress tests, and cardiac catheterization results.

- Treatment response and stability: Well-controlled arrhythmias with consistent medication response demonstrate lower risk than unstable conditions requiring frequent medication adjustments or hospitalizations.

Bottom Line

Insurance companies focus on your arrhythmia’s impact on life expectancy rather than just the diagnosis itself. Stable, well-managed conditions often qualify for standard or near-standard rates.

“Most people with well-controlled atrial fibrillation can get standard life insurance rates if they’ve been stable for at least 12 months and show good adherence to their treatment plan.”

– InsuranceBrokers USA – Management Team

How Do Different Types of Arrhythmia Affect Coverage?

Each type of arrhythmia presents unique considerations for life insurance underwriting. Our experience with hundreds of cases reveals clear patterns in how companies evaluate different heart rhythm disorders.

Arrhythmia Coverage Impact by Type

| Condition | Typical Rating | Key Factors |

|---|---|---|

| Atrial Fibrillation | Standard to Table 4 | Control level, stroke risk |

| PACs/PVCs (occasional) | Standard | Frequency, symptoms |

| Ventricular Tachycardia | Table 6+ or decline | Cause, ICD placement |

| Bradycardia with pacemaker | Table 2 to Table 6 | Pacemaker dependency |

| Supraventricular Tachycardia | Standard to Table 2 | Treatment success, episodes |

Atrial Fibrillation: The Most Common Scenario

Atrial fibrillation represents the majority of arrhythmia cases we handle. Key insight: Insurance companies primarily focus on your stroke risk assessment (CHADS2 or CHA2DS2-VASc score) rather than just the AFib diagnosis.

- Factors that improve your rates: Successful cardioversion, consistent INR levels on warfarin, or effective rate control with minimal symptoms. Recent studies show that patients in persistent AFib who maintain good rate control can often secure standard rates.

- Challenges for coverage: Poorly controlled AFib with frequent rate spikes, multiple cardioversions, or high stroke risk scores typically result in higher premiums or coverage limitations.

Key Takeaways

- Benign arrhythmias like occasional PACs rarely affect premiums

- Well-controlled AFib can qualify for standard rates after 12+ months stability

- Serious ventricular arrhythmias typically require specialized underwriting

- Pacemaker patients need detailed device reports for optimal rates

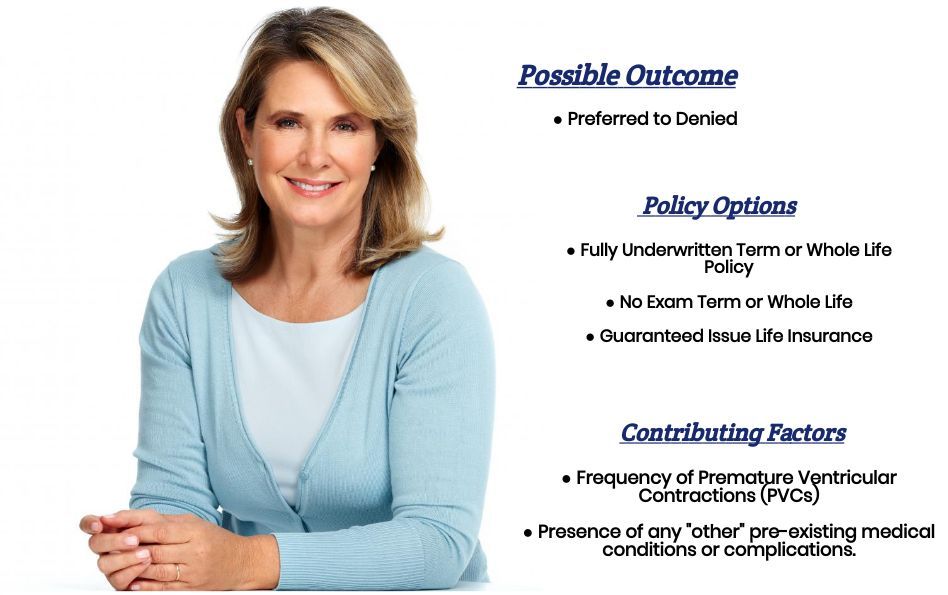

What Coverage Options Are Available?

Individuals with arrhythmia have access to multiple coverage pathways, each designed for different health profiles and coverage needs. Understanding these options helps you choose the most appropriate and cost-effective solution.

Traditional Fully Underwritten Policies

Best for: Stable arrhythmias with good medical records and at least 12 months of consistent treatment. These policies offer the lowest premiums for qualified applicants.

The application process includes comprehensive medical underwriting with attending physician statements, possible medical exams, and detailed review of your cardiac history. Most companies require 12-24 months of stable treatment before considering standard rates.

Simplified Issue Life Insurance

Coverage amounts: Typically $25,000 to $300,000 depending on age and company. These policies ask health questions but don’t require medical exams or extensive medical records review.

Key insight: Several major carriers now accept well-controlled atrial fibrillation through simplified issue applications, provided you haven’t been hospitalized for heart problems in the past two years.

“For clients with stable AFib who need coverage quickly, simplified issue policies can provide meaningful protection while they work toward qualifying for fully underwritten coverage later.”

– InsuranceBrokers USA – Management Team

Guaranteed Issue Life Insurance

These policies accept all applicants regardless of health conditions but come with significant limitations. Coverage amounts typically cap at $25,000, and most policies include a two-year waiting period where only premiums paid plus interest are returned if death occurs from natural causes.

Strategic use: Guaranteed issue works well as immediate coverage while pursuing other options, or for final expense needs when other coverage isn’t available.

Group Life Insurance Through Employers

Employer-provided group life insurance often represents the most accessible coverage for individuals with arrhythmia. Most group policies accept all eligible employees without health questions, though coverage amounts may be limited.

Maximization strategy: Take full advantage of guaranteed issue amounts through your employer, then supplement with individual coverage as your health condition stabilizes.

Bottom Line

Most people with arrhythmia can get life insurance. The key is matching your current health status with the right type of policy and working with experienced agents who understand cardiac underwriting.

How to Apply Successfully with Arrhythmia?

Strategic application preparation significantly improves your chances of securing coverage at the best possible rates. Our systematic approach, refined through hundreds of successful arrhythmia cases, maximizes approval odds while minimizing delays.

Timing Your Application

Optimal timing window: Apply 12-24 months after your arrhythmia diagnosis has stabilized with consistent treatment. This timeframe allows you to demonstrate treatment effectiveness while maintaining urgency for family protection.

Avoid applying during periods of medication changes, recent cardiac procedures, or symptom fluctuations. Insurance companies view stability as the primary risk indicator, making timing crucial for optimal rates.

Medical Record Preparation

Comprehensive medical documentation strengthens your application significantly. Request copies of all relevant records before applying, including cardiology consultation notes, ECGs, echocardiograms, stress tests, and medication lists with dosages.

Documentation that helps your case: Normal ejection fraction reports, successful rhythm control documentation, medication compliance records, and any lifestyle modifications you’ve made post-diagnosis.

Working with Multiple Insurance Companies

Different carriers have varying appetites for arrhythmia cases. Some companies specialize in cardiac conditions while others avoid them entirely. Our experience shows that applying to 3-4 carefully selected companies simultaneously often yields better rate offers.

Application Success Strategies

- Complete applications during stable health periods, not acute episodes

- Gather comprehensive medical records before starting the process

- Work with agents experienced in cardiac condition placements

- Consider multiple companies simultaneously for rate comparison

- Be prepared to provide additional medical information promptly

What Medical Records Do You Need?

Comprehensive medical documentation forms the foundation of successful arrhythmia underwriting. Insurance companies require specific reports to assess your cardiovascular risk accurately, and missing documentation often delays or derails applications.

Essential Cardiac Testing Reports

- Electrocardiograms (ECGs): Recent ECGs showing current rhythm status are fundamental. Companies want to see both your initial diagnosis ECG and current rhythm documentation, particularly if you’ve achieved rate or rhythm control.

- Echocardiogram results: Ejection fraction measurements and structural heart assessments significantly influence underwriting decisions. Normal ventricular function often offsets arrhythmia concerns substantially.

- Holter monitor or event recorder data: These extended monitoring reports provide detailed information about arrhythmia frequency and pattern, helping underwriters assess symptom burden and treatment effectiveness.

Physician Documentation Requirements

Cardiology consultation notes offer critical insights into your prognosis and treatment plan. These reports should detail your specific arrhythmia type, underlying causes, treatment response, and long-term management strategy.

Key elements underwriters seek: Treatment timeline, medication effectiveness, symptom improvement, functional capacity, and physician’s assessment of long-term outlook.

Treatment and Procedure Records

If you’ve undergone cardiac procedures like ablation, cardioversion, or device implantation, detailed procedure reports become essential documentation. Success rates and complications significantly influence coverage decisions.

Medical Records Checklist

- Most recent ECG and rhythm strips

- Complete echocardiogram report with ejection fraction

- Holter monitor or event recorder summaries

- Cardiology consultation notes (last 2 years)

- Stress test results if performed

- Medication list with dosages and compliance notes

- Procedure reports for any cardiac interventions

Which Companies Offer the Best Rates?

Different insurance companies have varying underwriting philosophies for arrhythmia cases. Some carriers specialize in cardiac conditions while others avoid them entirely. Understanding company preferences helps target your applications effectively.

Companies with Favorable Arrhythmia Underwriting

Carriers known for competitive cardiac rates: Several major insurers have developed specialized underwriting protocols for heart rhythm disorders, often resulting in better rate classifications for stable cases.

These companies typically employ medical directors with cardiology backgrounds and utilize sophisticated risk assessment models that consider treatment advances and improved outcomes for arrhythmia patients.

Specialized Placement Strategies

Our team maintains relationships with over 50 life insurance carriers, allowing us to match your specific arrhythmia profile with companies most likely to offer competitive rates. This targeted approach often saves months of application time and significantly improves rate outcomes.

Key insight: Company appetite for arrhythmia cases changes frequently based on claims experience and medical director preferences. Working with experienced brokers who track these changes provides substantial advantages.

“We regularly place clients with well-controlled AFib at standard rates with companies that understand modern arrhythmia management. The key is knowing which carriers to approach and how to present the case effectively.”

– InsuranceBrokers USA – Placement Strategy

For personalized company recommendations based on your specific arrhythmia type and health profile, contact our specialized cardiac placement team at 888-211-6171. Our experience with hundreds of successful arrhythmia placements helps identify the carriers most likely to offer competitive rates for your situation.

Additionally, consider reviewing our comprehensive guides on the top 10 best life insurance companies in the U.S. and life insurance approvals with pre-existing medical conditions for broader context on company selection strategies.

Frequently Asked Questions

Can I get life insurance if I have atrial fibrillation?

Yes, most people with atrial fibrillation can obtain life insurance coverage. The key factors are how well your AFib is controlled, your overall heart function, and stroke risk factors. Well-controlled AFib with normal heart function often qualifies for standard rates after 12-18 months of stable treatment. More complex cases may require table ratings but still remain insurable.

How long should I wait after my arrhythmia diagnosis to apply?

The optimal waiting period is typically 12-24 months after diagnosis and treatment stabilization. This timeframe allows you to demonstrate treatment effectiveness and symptom control. However, if you have dependents who need immediate protection, consider temporary coverage through simplified issue or guaranteed issue policies while working toward fully underwritten coverage later.

Will having a pacemaker automatically disqualify me from coverage?

No, having a pacemaker does not automatically disqualify you from life insurance. Many individuals with pacemakers secure coverage, though rates depend on your dependency level, underlying heart condition, and pacemaker function. Pacemaker patients typically receive table ratings ranging from Table 2 to Table 6, with less dependent individuals receiving better rates.

What happens if my arrhythmia worsens after getting a policy?

Once your life insurance policy is issued and in force, changes in your health condition cannot affect your coverage or premiums. This includes worsening arrhythmia, additional cardiac procedures, or new heart conditions. Your policy remains guaranteed as long as you pay premiums, making early coverage particularly valuable for progressive conditions.

Should I mention occasional heart palpitations on my application?

Yes, you must disclose all cardiac symptoms and diagnoses honestly on your application. Occasional palpitations, especially if medically evaluated, should be reported. However, benign palpitations like infrequent PACs (premature atrial contractions) rarely affect coverage decisions when properly documented. Failure to disclose could void your policy later.

How do blood thinners affect my life insurance application?

Blood thinner use indicates stroke risk management and is generally viewed favorably by underwriters. Consistent INR levels (for warfarin users) or proper adherence to newer anticoagulants like apixaban demonstrate good medical management. The underlying condition requiring blood thinners matters more than the medication itself for underwriting purposes.

Can I get no-exam life insurance with arrhythmia?

Yes, several no-exam life insurance options are available for individuals with arrhythmia. Simplified issue policies typically accept well-controlled AFib without recent hospitalizations. Coverage amounts range from $25,000 to $300,000 depending on age and company. While rates may be higher than fully underwritten policies, no-exam options provide faster coverage for immediate protection needs. Consider our guide to the top 10 best no-exam life insurance companies for specific options.

Ready to Secure Your Coverage?

Our specialized team has helped hundreds of individuals with arrhythmia secure the life insurance protection they need. We understand cardiac underwriting and work with companies that offer competitive rates for heart rhythm conditions.

Call 888-211-6171 today for a personalized consultation. We’ll review your specific situation, recommend the most appropriate coverage options, and help you navigate the application process successfully.

Disclaimer: This information is for educational purposes only and does not constitute medical or insurance advice. Consult with qualified professionals for personalized guidance regarding your specific health condition and insurance needs.