In this article, we wanted to take a moment to try to answer some of the most common questions we get from folks applying for life insurance after undergoing some “type” of Bariatric Surgery to lose weight. The only problem is when it comes to discussing “bariatric surgery,” it seems like just about every other day, some new procedure becomes available that is either less invasive or traumatic than the one before it.

“Which is great!”

But most of the time, life insurance companies tend to be a “bit” slow in making changes to their underwriting guidelines, which is why in this article, we’re going to treat a wide variety of different bariatric procedures, including:

- Gastroplasty,

- Gastric Band Surgery,

- Gastric Bypass,

- Gastric Stapling,

- Intestinal Bypass,

And Sleeve Gastrectomy is the same because, with just a few exceptions, most “types” of bariatric procedures will receive the same “underwriting treatment” by most of the top-rated life insurance companies we are familiar with.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after undergoing Bariatric Surgery?

- Why do life insurance companies care if I’ve undergone Bariatric Surgery?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve undergone Bariatric Surgery?

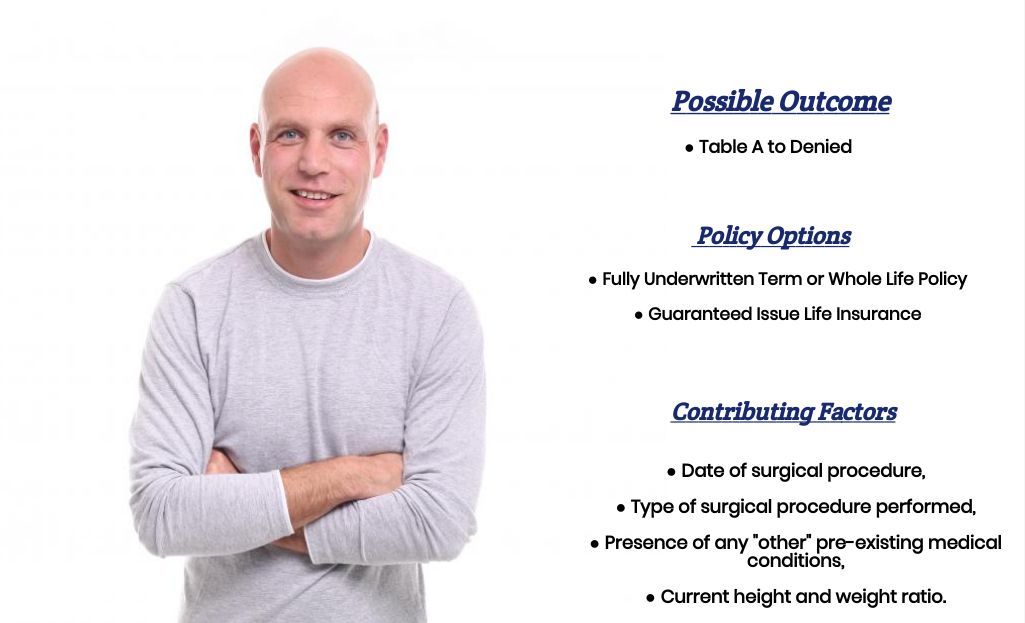

Yes, individuals can and often will be able to qualify for a traditional term or whole life insurance policy. And in some cases, they may even “technically” be eligible for a Preferred rate! Unfortunately, though, for an individual to qualify for any “kind” of surgical weight loss procedure, you typically need to have a body mass index (BMI) of 40 or higher!

Which…

As most doctors will tell you, it is extremely unhealthy. Now, we’re not stating this to make people feel bad. We’re simply stating it because in most situations, when we start the process of helping someone find a life insurance policy that they will be able to qualify for after having received a weight reduction surgery, we frequently encounter “other” pre-existing medical conditions as well.

Conditions such as:

- Elevated blood pressure or cholesterol levels,

- High blood sugar levels (type 2 diabetes),

- Sleep apnea,

- Gastroesophageal reflux disease (GERD),

- Heart disease,

- Cancer,

- Etc, etc…

This is why it may “technically” be possible for some folks who have had some “type” of bariatric surgery performed; it’s also highly unlikely.

Why do life insurance companies care if I’ve undergone Bariatric Surgery?

There are several reasons why a life insurance company will “care” if you have received bariatric surgery. The first reason is that it will help them place your current height and weight ratio into context because if you “barely” meet the minimum requirements for a traditional term or whole life insurance policy. It has been several years since your surgery; the insurance companies may want to take a closer look at your application than they might someone who has never received a weight-loss surgical procedure.

The second reason why…

A life insurance company might “care” if you have received such a surgical procedure because they may now want to take a look at your medical records leading up to your surgery so that they can get a better idea of just how “serious” your health was presumably before your procedure turned things around for you.

Lastly…

Just like any other surgical procedure, each “elective” weight loss procedure will come with a risk. A risk that the life insurance companies will want to know about and a risk that they will want to minimize as much as possible before making any decision about the outcome of your life insurance application.

This is why, before getting approved for coverage, you should be prepared to answer a wide range of questions about your procedure and how it has improved your health today.

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked may include:

- When did you undergo your bariatric surgery?

- What kind of surgery did you have?

- Gastroplasty?

- Gastric Band Surgery?

- Gastric Bypass?

- Gastric Stapling?

- Sleeve Gastrectomy?

- Did you experience any complications as a result of your surgery?

- What was your BMI before surgery?

- What is your current height and weight or BMI?

- Have you been diagnosed with any pre-existing medical conditions?

- Have you ever suffered from a heart attack or stroke?

- Are you currently taking any prescription medications?

- In the past 12 months, have you used any tobacco or nicotine products?

- Are you currently working now?

- In the past 12 months, have you applied for or received any disability benefits?

What rate (or price) can I qualify for?

As you can see, this can be important when it comes to understanding what kind of “rate” an individual might be able to qualify for. In many cases, the questions we listed above only represent the “tip” of the iceberg. This is because, with each procedure, a life insurance company may have its own set of questions that it still wants to ask, as well as a whole bunch of questions should you have any pre-existing medical conditions, on top of the fact that you elected for one of the “types” of surgeries.

The good news is…

In most cases, individuals who elect to have a weight-loss surgical procedure will significantly improve their overall health. This health improvement will usually be reflected in the “type” of life insurance they can qualify for and the “price” they will be expected to pay. That said, however, most of these individuals will still most likely be considered a “high-risk” applicant, making “who” they decide to apply with all the more important.

This is why we wanted to end our discussion here by providing you with a few helpful tips that we believe might make it easier for you to find the “best” life insurance policy you can qualify for.

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance professional who will work as an advocate for them.

Such an agent…

It will help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible for you. From there you’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

Before applying for coverage, you should be completely honest with your life insurance agent. By doing so, you will help them narrow down what options might be the “best. “

Now, will we be able to help out everyone who has been previously diagnosed with Gastric Bypass Surgery?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Top-Rated Final Expense Life Insurance Companies so that if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that they CAN qualify for.

So, if you’re ready to explore your options, call us!