In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance with Otosclerosis.

Questions that will be addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Otosclerosis?

- Why do life insurance companies care if I’ve been diagnosed with Otosclerosis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I’ve been diagnosed with Otosclerosis?

Yes, individuals who have been diagnosed with Otosclerosis can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, some may even be able to qualify for some of the best no medical exam life insurance companies at a Preferred rate!

The only problem is…

That any time someone suffers from a chronic medical condition that can potentially have a very significant effect on one’s life and lifestyle, most life insurance companies are going to want to know a little bit that “particular” pre-existing medical condition before they will be willing to make any kind of definitive decision about the outcome of your life insurance application.

Why do life insurance companies care if I’ve been diagnosed with Otosclerosis?

The main reason why a life insurance company is going to “care” if you have been diagnosed with Otosclerosis is that in extreme cases, it can potentially cause someone to go completely deaf. And while going completely deaf isn’t going to kill someone, it could potentially affect what they can do for a living and a host of other things that tend to make a life insurance company nervous.

This is why…

We wanted to take a moment to discuss what Otosclerosis is and highlight some of the most common symptoms/complications of this disease so that we might gain a better understanding of what a life insurance underwriter will be looking for when making his or her decision about your application.

Otosclerosis Defined:

Otosclerosis is a disease that occurs when one of the bones within the middle ear (usually the stapes) begins to grow “abnormally” and fixates itself onto the oval window, thereby interfering with the way that sound waves pass into the inner ear. Typically, what occurs is that this “abnormal” growth will first occur in one ear then shortly after that appear in the other non-affected ear.

Common symptoms may include:

- Tinnitus,

- Dizziness,

- Difficult hearing low-pitched sounds or whispers,

- Balance problems,

- Etc…

Serious complications may include:

- Changes to one’s taste palate,

- Increased risk of infection,

- Permanent hearing loss.

Fortunately…

Otosclerosis is a condition that can either be treated through the use or a hearing aid, or having a surgical procedure known as a stapedectomy performed whereby a prosthetic device is implanted within the middle ear allowing one to bypass the abnormal bone thus allowing sound waves to travel freely into the inner ear.

Now at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any kind of “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like this one, find and qualify for the life insurance coverage that they are looking for.

But…

Not so great if you’re looking for answers to any specific medical questions. In cases like these, we would recommend that you contact a true medical professional who has the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What kind of information will the insurance companies ask me or be interested in?

Because Otosclerosis isn’t considered a “life-threatening” medical condition, and because it can usually be treated/cured through via surgery or through the use of a hearing aid, most (if not all) life insurance companies aren’t going to need to ask an applicant all that many questions about their Otosclerosis other than:

- Have you had your Otosclerosis treated?

- And can you hear properly now?

Besides that, there really aren’t any other symptoms or side effect that a life insurance company is going to be all that worried about.

Which then just…

Leaves us with the “usual” questions that most life insurance companies will ask of any applicant looking to qualify for a traditional term or whole life insurance policy which will typically look something like this:

- Date of birth?

- Current height and weight?

- Aside from your Otosclerosis, have you been diagnosed with any other pre-existing medical conditions?

- Have you ever been diagnosed with cancer, heart disease, diabetes, or depression?

- Have you ever suffered from a heart attack or stroke?

- Have any of your immediate family members (mother, father, brother, or sister) ever been diagnosed with cancer, heart disease, diabetes?

- Have any of your immediate family members ever suffered from a heart attack or stroke?

- Are you currently taking any prescription medications?

- In the past 12 months, have you used any tobacco or nicotine products?

- In the past two years, have you been hospitalized for any reason?

- Do you have any issues with your drivers’ license? Issues such as multiple driving violations, a DUI, or a suspended license?

- Do you have any “set” plans to travel outside of the United States?

- Do you actively participate or plan on participating in any dangerous hobbies?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

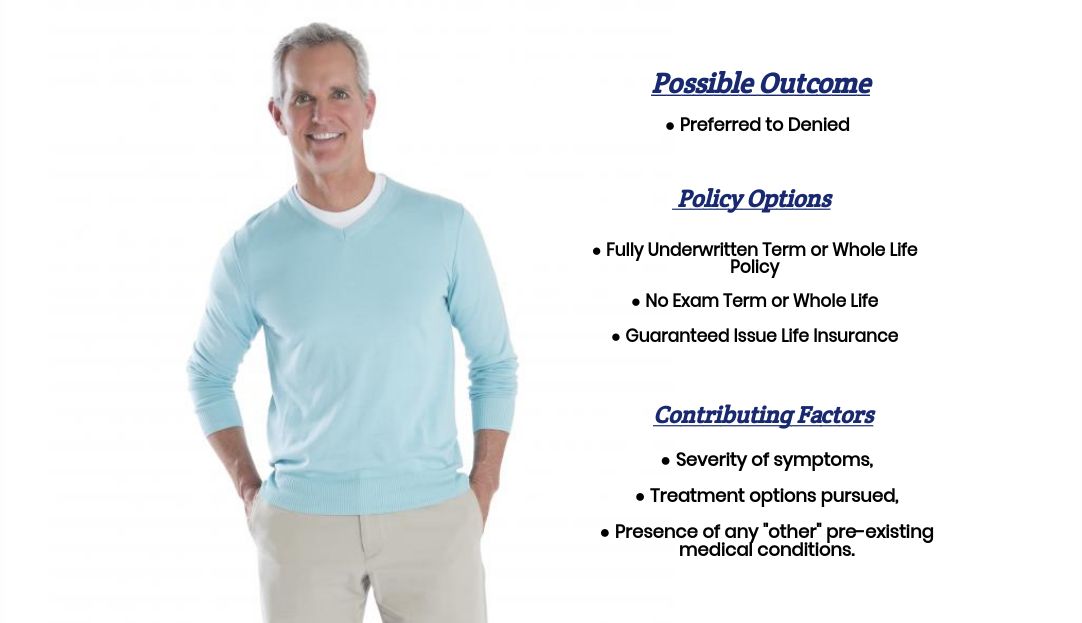

What rate (or price) can I qualify for?

As you can see, there are a lot of variables that can come into play when trying to determine what kind of “rate” an individual might be able to qualify for. This is why it’s almost impossible to know what kind of “rate” you might qualify for without first speaking with you directly for a few minutes.

That said however…

There are a few “assumptions” that we can make concerning how an individual’s Otosclerosis will be viewed by most life insurance companies that will generally hold true.

For example, if you have been diagnosed with Otosclerosis, and it has begun to affect your hearing, and you have either obtained a hearing aid or have had a stapedectomy performed chances are you’re Otosclerosis diagnosis isn’t going to play any role in the outcome of your life insurance application.

Meaning that…

Whatever rate you would have been able to qualify for PRIOR to being diagnosed with Otosclerosis should be the same rate that you would be able to qualify for AFTER being diagnosed with Otosclerosis.

Now as for those…

Who have been diagnosed with Otosclerosis, and are suffering from hearing difficulties but have not yet obtained a hearing aid or had a stapedectomy performed, you too may still be able to qualify for a Preferred rate only now, most life insurance companies will be looking for “clues” or “signs” that your hearing loss could be becoming an issue (an example being you are currently receiving a disability benefit due to your hearing loss).

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy that they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

And seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to helping a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is exactly what you’re going to find here at IBUSA!

Now, will we be able to help out everyone who has been previously diagnosed with Otosclerosis?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that in the event that someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to see what options might be available to you, just give us a call!