In this article, we wanted to take a moment to answer some of the most common questions we get from people applying for life insurance after being diagnosed with Mallory-Weiss Syndrome (MWS).

Questions that will be directly addressed will include:

- Can I qualify for life insurance if I have been currently diagnosed with Mallory-Weiss Syndrome?

- Why do life insurance companies care if I currently have Mallory-Weiss Syndrome?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance if I have currently been diagnosed with Mallory-Weiss Syndrome?

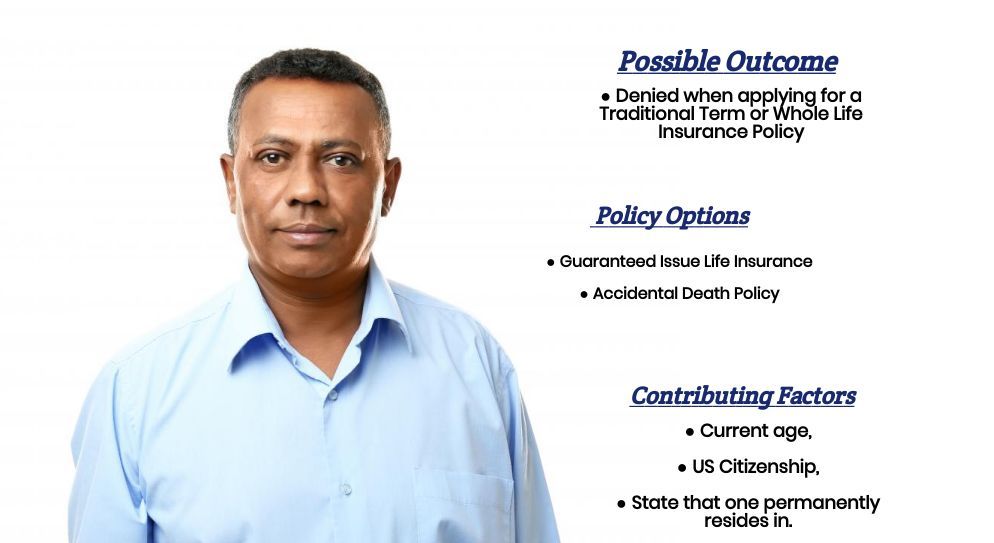

Unfortunately, for those who are currently being treated for Mallory-Weiss Syndrome, what you’re generally going to find is that most (if not all) life insurance companies are going to want to make sure that fully recover from your condition prior to making any kind of decision about your life insurance application.

This is why if you do end up applying for a traditional term or whole life insurance policy and are currently suffering from this condition, most life insurance companies will simply “postpone” your application until you have made a full recovery.

It’s also why…

You may want to consider avoiding applying for a no medical exam term life insurance policy as well, seeing how these policies tend to be more difficult to qualify for after someone has been diagnosed with a pre-existing medical condition like Mallory-Weiss Syndrome.

Why do life insurance companies care if I currently have Mallory-Weiss Syndrome?

The main reason a life insurance company will “care” if an individual has been diagnosed with Mallory-Weiss Syndrome is that, at the end of the day, while an individual is “fighting” this disease/syndrome, many “potential” complications may arise, mostly centering around the possibility of infections.

Additionally…

Because Mallory-Weiss is a condition most commonly caused by violent coughing and/or vomiting, it only makes sense that a life insurance company would want to uncover “why” an individual has developed Mallory-Weiss Syndrome and see if this might also be a cause of concern when considering you as a possible new client. This is why it only makes sense to briefly define what the Mallory-Weiss Syndrome is, as well as highlight a few of the most common symptoms that a life insurance underwriter will be looking for when making his or her decision about your life insurance application.

Mallory-Weiss Syndrome (MWS) Defined:

Mallory-Weiss Syndrome is a condition that is defined by a rip or tear in the mucous membrane at the point where the esophagus meets the stomach. Fortunately, most “tears” will heal on their own without any medical treatment within approximately 7 to 10 days.

Common symptoms may include:

- Abdominal pain,

- Previous history of a persistent cough,

- Previous history of severe vomiting,

- Hematemesis (vomiting blood),

- Dark stools (Melenic stools).

The good news is…

That in most cases, once the underlying pre-existing medical condition which has caused someone to develop Mallory-Weiss Syndrome has resolved, the prognosis of these tears is very good. In fact, nearly 80-90% of them will stop bleeding on their own or with minimal therapy within 48 to 72 hours. This is why we usually don’t have individuals applying for a life insurance policy while currently suffering from this condition unless it manifests itself during the application process.

What kind of information will the insurance companies ask me or be interested in?

Common questions you may be asked may include:

- When were you first diagnosed with Mallory-Weiss Syndrome?

- Are you currently treating it now?

- What symptoms led to your diagnosis?

- Do you know what has caused you to suffer from this condition?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you currently taking any prescription medications?

- In the past two years, have you been admitted to the hospital for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

What rate (or price) can I qualify for?

When trying to determine what kind of “rate” an individual who has previously been diagnosed with Mallory-Weiss Syndrome can qualify for, what you’re generally going to find is that most applicants will fall into one of three categories.

Category #1.

Those who are currently suffering from Mallory-Weiss Syndrome will automatically have their application either denied or postponed until which point they have made a full recovery.

Category #2.

Those who have recovered from their Mallory-Weiss Syndrome yet suffer from some other pre-existing medical condition, which caused them to develop their MWS, which will now be the primary factor determining what kind of “Rate” they will be able to qualify for.

Category #3.

Category 3 applicants will be those who have recovered from their Mallory-Weiss Syndrome and don’t suffer from any other pre-existing medical condition that caused one to develop MWS in the first place. These would be folks who, maybe, developed their Mallory-Weiss Syndrome as a result of a serious case of:

- The stomach flu,

- Food poisoning,

- Whooping cough,

- Etc…

In cases like these, you’ll typically find that once an individual has made a full recovery, their previous Mallory-Weiss Syndrome diagnosis probably won’t play a role in the outcome of their life insurance application. This means that whatever “rate” they would have been able to qualify for PRIOR to being diagnosed with MWS should be the same “rate” that they would be able to qualify for AFTER being diagnosed with MWS!

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy that they can qualify for. This brings us to the last topic that we wanted to take a moment and discuss, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

Seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to help a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is exactly what you’re going to find here at IBUSA!

Now, will we be able to help out everyone who has been previously diagnosed with Mallory-Weiss Syndrome?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well so that in the event that someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, just give us a call!