A liver failure diagnosis creates immediate concerns about family financial security, especially when conventional wisdom suggests that qualifying for life insurance has become impossible. But the truth is that the reality of the situation is much more nuanced than most people realize.

While liver failure significantly impacts insurance options, numerous coverage strategies may still exist depending on your specific condition, treatment response, and current health status. Our analysis of hundreds of cases reveals that individuals with liver failure can often secure meaningful coverage through specialized approaches that traditional life insurance agents rarely discuss.

This comprehensive guide examines every available option, from immediate coverage solutions to long-term strategies that maximize your family’s financial protection during one of life’s most challenging periods.

Important Medical Disclaimer

This article provides insurance guidance only and is not medical advice. Always consult with your healthcare provider about your specific condition and treatment options. If you’re experiencing a medical emergency, contact emergency services immediately.

About Our Team

The Insurance Brokers USA Team consists of licensed insurance professionals with extensive experience helping clients with complex health conditions find appropriate coverage. Our agents have worked with thousands of individuals facing liver disease challenges, specializing in alternative insurance solutions when traditional coverage isn’t available.

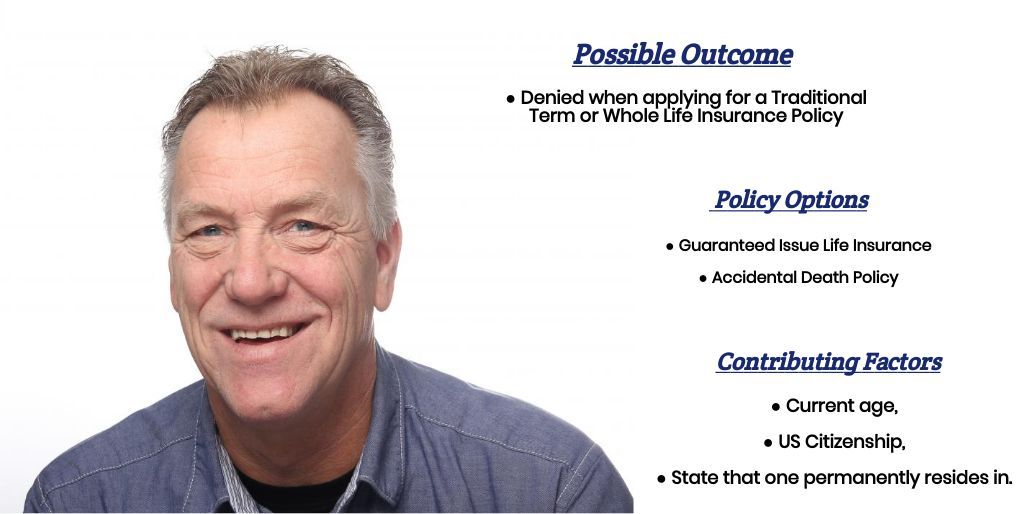

How Does Liver Failure Impact Life Insurance Eligibility?

Key insight: Insurance companies evaluate liver failure cases based on underlying cause, current function level, treatment response, and prognosis rather than applying blanket denials.

Liver failure represents one of the most complex medical conditions from an insurance underwriting perspective. Companies must assess not only the current severity but also the underlying cause, treatment options, and long-term prognosis. This multifaceted evaluation creates both challenges and opportunities for applicants.

“We’ve seen dramatic differences in coverage options based on the specific type of liver condition. A person with compensated cirrhosis may qualify for modified coverage, while someone with acute liver failure faces more limited options.”

– Senior Underwriter – InsuranceBrokers USA

Insurance companies typically categorize liver failure into several distinct groups:

- Acute liver failure cases receive the most restrictive underwriting, as the condition often develops rapidly and carries significant mortality risk. However, individuals who demonstrate stable recovery may find coverage options after a waiting period.

- Chronic liver failure with compensated function often allows for coverage consideration, particularly when the underlying condition remains stable under medical management.

- Liver failure secondary to alcohol use faces additional scrutiny regarding sobriety maintenance and lifestyle factors, but coverage remains possible with demonstrated long-term recovery.

Bottom Line

Liver failure doesn’t automatically disqualify you from life insurance, but the specific cause, current status, and treatment response significantly influence available options and pricing.

What Types of Coverage Are Available?

Key insight: Multiple coverage categories exist specifically designed for individuals with serious health conditions, each offering different benefits and limitations.

Coverage Options by Health Status

| Coverage Type | Eligibility Requirements | Typical Coverage Amount |

|---|---|---|

| Guaranteed Issue | Ages 50-85, no health questions | $5,000-$25,000 |

| Simplified Issue | Limited health questions | $10,000-$300,000 |

| Graded Death Benefit | Immediate coverage with restrictions | $5,000-$50,000 |

| Modified Traditional | Full underwriting with exclusions | $25,000-$500,000 |

Guaranteed issue life insurance provides the most accessible option, requiring no medical questions or exams. While coverage amounts remain limited and premiums are higher, this option ensures immediate acceptance, regardless of the severity of the liver condition.

Simplified issue policies ask basic health questions but typically exclude individuals with current liver failure. However, those in stable remission or with well-managed chronic conditions may qualify depending on specific carrier guidelines.

“The key strategy is matching your specific situation to the right type of coverage. Someone with stable, compensated cirrhosis might qualify for simplified issue, while someone with decompensated liver disease should focus on guaranteed issue options.”

– Insurance Brokers USA Team Lead Agent

Graded death benefit policies offer immediate coverage but limit full benefits during the initial years. These policies typically provide partial benefits (often return of premiums plus interest) if death occurs from natural causes during the first two to three years.

Key Takeaways

- Multiple coverage types exist specifically for high-risk applicants

- Guaranteed issue provides certainty, but with coverage limitations

- A simplified issue may work for stable, well-managed conditions

- Graded benefit policies offer immediate partial protection

- Coverage amounts vary significantly between policy types

How Should You Approach the Application Process?

Key insight: Strategic application preparation and complete medical documentation significantly improve approval chances and coverage terms.

The application process for individuals with liver failure requires careful preparation and complete transparency about your medical history. Insurance companies will eventually discover any undisclosed conditions through medical records requests, making honesty the foundation of successful applications.

Pre-application preparation involves:

Gathering comprehensive medical records from all treating physicians, including gastroenterologists, hepatologists, and primary care providers. Complete documentation helps underwriters understand your condition’s stability and management effectiveness.

Organizing laboratory results chronologically to demonstrate trends in liver function tests, including ALT, AST, bilirubin, albumin, and clotting factors. Stable or improving numbers strengthen your application significantly.

Documenting treatment compliance and lifestyle modifications, particularly abstinence from alcohol if applicable. Insurance companies view compliance as a strong predictor of future health outcomes.

“Applications succeed when we can paint a complete picture of stability and medical management. Underwriters want to see that the condition is well-understood and properly controlled.”

– InsuranceBrokers USA – Management Team

Application timing considerations include:

Avoiding applications during acute phases or immediately following diagnosis. Most carriers prefer to see at least 6-12 months of stable function before considering coverage.

Coordinating applications with regular medical monitoring schedules. Recent lab work and physician assessments strengthen applications by demonstrating current condition status.

Bottom Line

Complete honesty, thorough documentation, and strategic timing maximize your chances of approval and favorable coverage terms.

What Will Coverage Cost?

Key insight: Premium costs vary dramatically based on coverage type, health status, and specific policy features, but affordable options exist across all risk categories.

Life insurance premiums for individuals with liver failure reflect the increased mortality risk associated with the condition. However, understanding the cost structure helps you budget appropriately and identify the most cost-effective coverage options.

Estimated Monthly Premiums by Age and Coverage Type

| Age/Coverage | Guaranteed Issue ($10K) | Simplified Issue ($25K) | Graded Benefit ($15K) |

|---|---|---|---|

| Age 50 | $45-65 | $85-120 | $55-75 |

| Age 60 | $65-90 | $125-175 | $80-110 |

| Age 70 | $95-130 | $200-280 | $120-160 |

*Estimates based on non-smoking males. Actual premiums vary by carrier, health status, and policy features.

Factors affecting premium costs include:

Underlying cause of liver failure significantly impacts pricing. Alcohol-related liver disease often carries higher premiums than viral hepatitis or genetic conditions, reflecting different risk profiles and prognoses.

Current liver function status, measured through laboratory values and clinical assessment, directly influences premium calculations. Stable, compensated function receives more favorable pricing than decompensated conditions.

Treatment response and compliance with medical recommendations demonstrate risk management to insurers. Individuals who follow treatment protocols typically qualify for better premium rates.

“We often recommend starting with guaranteed issue coverage for immediate protection, then reassessing options as health stabilizes. This strategy provides family security while keeping future opportunities open.”

– InsuranceBrokers USA – Management Team

Key Takeaways

- Premiums reflect increased mortality risk but remain manageable

- Guaranteed issue offers predictable costs regardless of health status

- Simplified issue provides better rates for stable conditions

- Age significantly impacts premium costs across all coverage types

- Starting with basic coverage allows future upgrade opportunities

When Is the Best Time to Apply?

Key insight: Application timing can significantly impact approval chances and coverage terms, with specific windows offering optimal opportunities for different condition stages.

The timing of your life insurance application plays a crucial role in determining available options and premium costs. Understanding optimal application windows helps maximize your chances of approval while securing the best possible terms.

Immediate application makes sense when:

You’re considering guaranteed issue coverage, which accepts applicants regardless of current health status. These policies provide immediate protection without medical underwriting, making timing less critical for approval but important for family financial planning.

Your condition appears stable and well-managed under current treatment protocols. Some carriers consider applications from individuals with compensated liver function, particularly when supported by strong medical documentation.

Delayed application benefits include:

Allowing time to demonstrate condition stability and treatment response. Most underwriters prefer seeing 6-12 months of stable liver function tests and consistent medical management before considering coverage.

Building a stronger application through improved health metrics and lifestyle modifications. Documented sobriety periods, weight management, and treatment compliance strengthen applications significantly.

“The sweet spot for applications often occurs 12-18 months after initial diagnosis, when patients have established stable treatment routines and demonstrated consistent health metrics.”

– InsuranceBrokers USA – Management Team

Consideration of multiple applications:

Some individuals benefit from a staged approach, starting with guaranteed issue coverage for immediate protection while working toward qualification for higher coverage amounts through simplified or traditional underwriting.

This strategy ensures family protection during the most vulnerable period while preserving opportunities for improved coverage as health conditions stabilize or improve.

Bottom Line

Optimal timing balances immediate protection needs with maximizing approval chances – guaranteed issue provides immediate security while waiting periods may improve options for higher coverage amounts.

What Alternative Protection Options Exist?

Key insight: When traditional life insurance proves challenging, multiple alternative financial protection strategies can provide meaningful security for your family’s future.

Individuals with liver failure who face limitations in traditional life insurance coverage can explore various alternative protection strategies that address similar financial security needs through different approaches.

Accidental Death Insurance

Accidental death insurance provides coverage specifically for deaths resulting from accidents, excluding illness-related mortality. While this limitation reduces comprehensive protection, accidental coverage often remains available regardless of existing health conditions and can provide substantial benefits at affordable premiums.

This option particularly appeals to individuals with liver failure who want to ensure family protection against unexpected accident-related losses while working toward traditional life insurance qualification.

Final Expense Insurance

Final expense insurance focuses specifically on covering burial, funeral, and immediate end-of-life costs rather than comprehensive income replacement. These policies typically offer guaranteed issue acceptance with coverage amounts ranging from $5,000 to $25,000.

“Many families find peace of mind combining a small guaranteed issue policy for immediate expenses with systematic savings for larger financial goals. This approach provides certainty while building additional protection.”

– Insurance Brokers USA Team Estate Planning Specialist

Self-insurance

Self-insurance through savings involves systematically setting aside funds that would have gone toward life insurance premiums into dedicated accounts earmarked for family financial security. While this approach requires discipline and time to build meaningful balances, it provides complete control and guaranteed availability.

Employer-sponsored benefits

Employer-sponsored benefits often include group life insurance coverage that may remain available despite individual health conditions. While coverage amounts typically remain limited to one or two times annual salary, employer plans frequently provide guaranteed issue acceptance for basic coverage levels.

Additionally, many employers offer supplemental voluntary life insurance that allows increased coverage through payroll deduction, often with simplified underwriting that proves more accessible than individual policies.

For families seeking comprehensive guidance on combining these alternative strategies with traditional insurance options, professional consultation can help develop integrated protection plans tailored to specific circumstances and goals. Contact our team at 888-211-6171 to discuss how multiple protection strategies can work together for your family’s security.

Key Takeaways

- Multiple alternatives exist when traditional coverage faces limitations

- Accidental death insurance provides partial protection regardless of health

- Final expense policies focus on immediate end-of-life costs

- Employer benefits may offer accessible group coverage options

- Self-insurance through savings provides complete control and certainty

- Combined strategies often provide more comprehensive protection than single approaches

How Can Professional Guidance Help?

Key insight: Specialized insurance professionals who understand liver conditions can identify coverage opportunities that general agents often miss while navigating complex underwriting requirements effectively.

Working with insurance professionals experienced in high-risk medical conditions provides significant advantages when seeking life insurance with liver failure. These specialists understand carrier-specific underwriting guidelines and can match your situation to the most appropriate coverage options.

Specialized knowledge includes:

Understanding which carriers offer the most favorable underwriting for specific types of liver conditions. Different companies show varying degrees of flexibility regarding viral hepatitis, alcohol-related liver disease, and genetic conditions.

Knowing optimal application strategies for different carriers, including timing recommendations, required documentation, and presentation approaches that maximize approval chances.

Identifying carriers that specialize in guaranteed issue or simplified issue products designed specifically for individuals with serious health conditions.

“The difference between working with a general agent and a specialist can be the difference between getting declined everywhere and finding multiple coverage options. We know which carriers to approach and how to present each case effectively.”

– InsuranceBrokers USA – Senior Life Agent

Professional services typically include:

Comprehensive case analysis that evaluates your specific medical history, current health status, and financial goals to recommend optimal coverage strategies.

Application preparation assistance including medical records organization, physician letter coordination, and strategic presentation of your case to underwriters.

Ongoing advocacy throughout the underwriting process, including communication with insurance company medical directors and negotiation of coverage terms when possible.

Choosing the right professional:

Look for agents or brokers with specific experience in high-risk medical conditions and documented success working with individuals facing liver disease challenges. Ask about their carrier relationships and specialized product knowledge.

Many individuals with liver failure benefit from working with our specialized team, which has developed specific expertise in navigating coverage options for complex medical conditions. Our approach combines comprehensive carrier knowledge with personalized service focused on your family’s unique needs and circumstances.

Bottom Line

Professional guidance significantly improves your chances of securing appropriate coverage by leveraging specialized knowledge, carrier relationships, and application expertise that general agents typically lack.

Frequently Asked Questions

Can I get life insurance immediately after a liver failure diagnosis?

Direct answer: Yes, guaranteed issue life insurance provides immediate coverage regardless of diagnosis timing, though coverage amounts remain limited.

Guaranteed issue policies accept applicants without medical questions or waiting periods related to diagnosis timing. While traditional underwriting typically requires stability periods, guaranteed issue coverage ensures immediate family protection when you need it most. Coverage amounts typically range from $5,000 to $25,000, with premiums based on age rather than health status.

Will my liver transplant status affect my eligibility?

Direct answer: Liver transplant recipients can qualify for coverage, particularly through guaranteed issue policies, with some carriers considering simplified issue applications after successful transplant periods.

Successful liver transplant recipients often find more coverage options available than individuals with ongoing liver failure, as the transplant addresses the underlying condition. Many carriers will consider applications 12-24 months post-transplant, provided there are no rejection episodes and organ function remains stable. The key factors include transplant success, medication compliance, and absence of complications.

How does alcohol-related liver disease impact my options?

Direct answer: Alcohol-related liver disease requires demonstrated sobriety for optimal coverage options, but guaranteed issue remains available regardless of alcohol history.

Insurance companies place significant emphasis on sobriety duration and maintenance when evaluating alcohol-related liver conditions. Many carriers prefer seeing 12-24 months of documented sobriety before considering simplified issue applications. However, guaranteed issue policies provide immediate coverage options regardless of alcohol history, ensuring family protection while you work on building a stronger application profile for higher coverage amounts.

What medical records will insurance companies request?

Direct answer: Companies typically request complete medical records from all treating physicians, recent laboratory results, and detailed treatment history spanning the past 5-10 years.

Comprehensive medical record requests usually include gastroenterology and hepatology records, primary care physician notes, hospital admission records, laboratory trends including liver function tests, imaging studies results, and documentation of medication compliance. For simplified issue applications, some carriers may only require physician statements or simplified medical questionnaires rather than complete records.

Can I increase my coverage amount later?

Direct answer: Some policies offer coverage increase options, and you can apply for additional coverage as your health status improves or stabilizes over time.

Many guaranteed issue and graded benefit policies include provisions for coverage increases at specific intervals without additional medical underwriting. Additionally, individuals who demonstrate improved health status may qualify for additional policies through different carriers or product types. Starting with basic coverage and systematically adding protection as opportunities arise often results in more comprehensive family financial security than waiting for ideal circumstances.

What happens if my condition worsens after getting coverage?

Direct answer: Once approved and in force, life insurance coverage cannot be cancelled or benefits reduced due to health changes, provided premiums remain current.

Life insurance contracts provide guaranteed coverage as long as premiums are paid as required. Insurance companies cannot cancel policies, increase premiums, or reduce benefits based on health deterioration after the coverage effective date. This protection makes securing coverage during stable periods particularly valuable, as it locks in your insurability regardless of future health changes.

Are there waiting periods for full death benefits?

Direct answer: Guaranteed issue and graded benefit policies typically include 2-3 year waiting periods for full natural death benefits, while simplified issue policies usually provide immediate full coverage.

Graded death benefit policies often return premiums plus interest if death occurs from natural causes during the initial 2-3 years, with full death benefits available thereafter. Accidental death typically receives full benefits immediately, regardless of waiting periods. Simplified issue policies that require medical underwriting usually provide full death benefits from the policy’s effective date. Understanding these waiting periods helps set appropriate expectations for family financial planning.

Get Expert Help with Your Life Insurance Application

Don’t navigate the complex world of life insurance with liver failure alone. Our specialized team understands the unique challenges you face and knows which carriers offer the best options for your specific situation.

What We Provide:

- Comprehensive analysis of your coverage options

- Strategic application preparation and submission

- Direct relationships with carriers specializing in high-risk cases

- Ongoing advocacy throughout the underwriting process

- No-cost consultation and policy comparison

Call 888-211-6171 for your free consultation

Licensed in all 50 states • Specialized in high-risk medical conditions • No obligation consultation

Related Coverage Options

Individuals with liver conditions often benefit from exploring comprehensive coverage strategies beyond traditional life insurance:

- Best Final Expense Insurance Companies of 2025 – Specialized coverage for immediate end-of-life expenses

- Life Insurance Approvals with Pre-Existing Medical Conditions – Comprehensive strategies for high-risk applicants

- Top 10 Best No Exam Life Insurance Companies – Simplified application processes for complex health conditions