In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after being diagnosed with Kimmelsteil-Wilson Disease.

Questions that will be directly addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Kimmelsteil-Wilson Disease?

- Why do life insurance companies care if I have been diagnosed with Kimmelsteil-Wilson Disease?

- What kind of information will the insurance companies ask me or be interested in?

- What options might be available to me?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance if I have been diagnosed with Kimmelsteil-Wilson Disease?

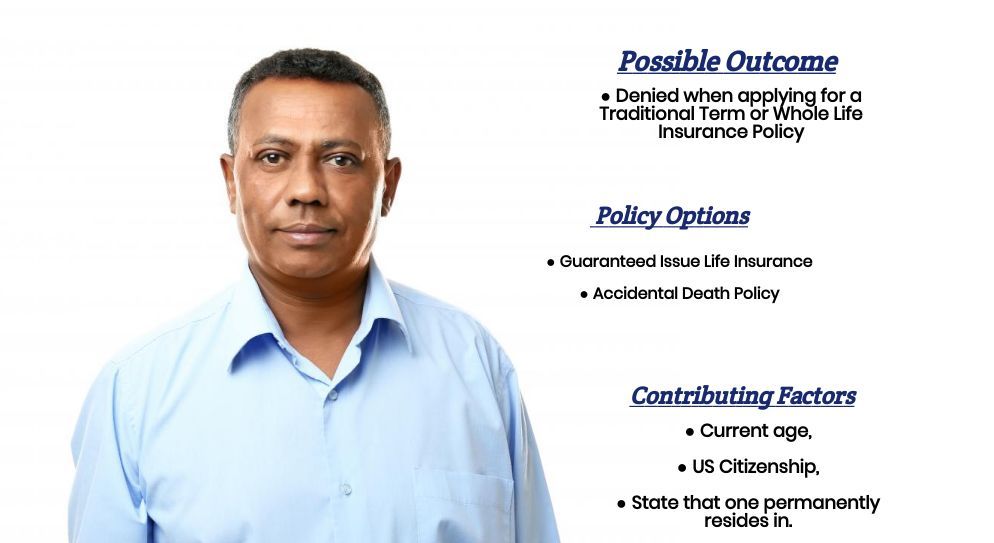

Unfortunately, when it comes to those who have been diagnosed with Kimmelsteil-Wilson Disease, what you’re generally going to find is that most (if not all) of the top-rated life insurance companies are going to “automatically” decline anyone applying for a traditional term or whole life insurance policy.

Which means that…

If you have been diagnosed with Kimmelsteil-Wilson Disease, you are going to need to pursue an “alternative” product that considers one’s health status as a requirement for approval.

Why do life insurance companies care if I have been diagnosed with Kimmelsteil-Wilson Disease?

The main reason why a life insurance company is going to “care” if you have been diagnosed with Kimmelsteil-Wilson Disease is that it is a condition that is usually associated with long term or long-standing diabetes whereby the tiny blood vessels or microvasculature system within the glomerulus begin to break down.

As a result…

Individuals will begin suffering from symptoms related to kidney impairment and may end up requiring dialysis or a kidney transplant. For this reason, most (if not all) life insurance companies are going to deny any applicant applying for a traditional term or whole life insurance policy if they have been diagnosed with Kimmelsteil-Wilson Disease.

Now at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any kind of “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like this one, find and qualify for the life insurance coverage that they are looking for.

But…

Not so great if you’re looking for answers to any specific medical questions. In cases like these, we would recommend that you contact a true medical professional who has the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What kind of information will the insurance companies ask me or be interested in?

What you’re generally going to find is that once a life insurance company determines that you’ve been diagnosed with Kimmelsteil-Wilson Disease, there isn’t a whole lot more they are going to need to know before denying your life insurance application. Even if you’ve subsequently received a new kidney and “technically” don’t suffer from this condition any longer.

This is mainly because…

Most life insurance agencies will usually be “geared” towards helping those who can qualify for a traditional term life insurance policy and won’t spend too much time focusing on smaller “alternative” products.

Fortunately…

Here at IBUSA we spend an incredible amount of time creating relationships with dozens of different life insurance companies so that we can minimize the number of times we have to apologize to a client that we just don’t have any options that they can qualify for.

This is why…

Were other agencies may inform you that you just can’t qualify for a life insurance policy because of your Kimmelsteil-Wilson diagnosis, we prefer to ask you three simple questions that could determine whether or not you might just be able to qualify for a Guaranteed Issue Life insurance policy.

Those three questions are:

#1. Are you a US Citizen?

#2. Are you between the ages of 40 and 85?

#3. What state do you live in?

What options might be available to me?

Now at this point, it’s important not to get too excited because while it is true that some folks may be able to qualify for a Guaranteed Issue Life Insurance policy or maybe even an Accidental Death Policy, it’s important to understand that just because you “can” qualify may not mean that you’ll “want” to qualify.

The reason for this…

Is because while these “types” of products may meet the needs for some, they are going to have some pretty serious disadvantages that may be a “deal-breaker” for some. Which is why after reading what we’re about to discuss we would invite you to then give us a call or visit one of our other articles that will go into greater detail about these “alternative products” so that you’ll know what you are “getting” should you decide to ultimately purchase one of these “types” of products.

Accidental Death and Guaranteed Issue Life Insurance Policies Defined

Accidental Death Policies

Here at IBUSA, we tend to think that when explained properly, Accidental Death Policies tend to be a bit easier to understand than Guaranteed Issue Life Insurance Policies, which is why we want to begin by discussing what an Accidental Death Policy is.

The problem is…

That a lot of times, these “types” of products aren’t fully explained or more commonly aren’t explained in a way that specifically points out what these types of policies won’t provide coverage for. This is why we here at IBUSA, want to begin our discussion of an Accidental Death Policy by specifically stating that these “types” of policies NOT TRUE LIFE INSURANCE POLICIES.

This is why…

You don’t need to be a licensed life insurance agent to sell them and why they aren’t going to provide you with any coverage in the event that you die of a “natural” cause of death.

Now at this point…

You may be asking yourself…

“What do you mean by NATURAL CAUSE of death?”

When we use the term “natural cause of death” we’re referring to an “illness-based” death like you would experience as a result of:

- Heart disease,

- Cancer,

- Stroke,

Or from some kind of complication that one might experience as a result of long-standing diabetes such as Kimmelsteil-Wilson Disease.

These types of products…

Are only going to provide a death benefit to your family in the event that you die from an accidental cause or any cause of death that isn’t “illness based”. Examples that would typically qualify as an Accidental Cause of death would typically include:

- A motor vehicle accident,

- A slip and fall accident

- A natural disaster,

- Victim of crime,

- Etc…

Which is nice…

But typically, this isn’t what someone is looking for after they have been diagnosed with Kimmelsteil-Wilson Disease. On the plus side, these “types” of products are generally pretty affordable and will allow someone to purchase a large amount of ACCIDENT insurance for a relatively small amount of money. This brings us to our next possible option, which is a…

Guaranteed Issue Life Insurance

A Guaranteed Issue Life Insurance policy, on the other hand, is A TRUE LIFE INSURANCE PRODUCT. This means that you do need to be a licensed life insurance agent to sell them, and “ultimately,” they will provide individual true-life insurance coverage. Now we say “ultimately” because when you purchase a Guaranteed Issue Life Insurance Policy, you’re purchasing a life insurance policy that has a “catch” to it.

And…

In our experience here at IBUSA, we’ve found that the best way to discuss these types of life insurance policies is by analyzing the three major disadvantages that these “types” of life insurance policies have aside from the fact that you generally have to be over the age of 50 and live in a state where these “types” of life insurance policies are available.

So, let’s dive right in…

Problem #1.

Guaranteed issue life insurance policies are only going to provide a limited amount of life insurance coverage and will usually “cap out” right around $25,000 dollars in coverage. This means that if you’re looking to purchase more than $25,000 dollars in coverage, a guaranteed issue life insurance policy might not be right for you!

(Yes, individuals can purchase several different guaranteed issue life insurance policies from several different companies, but as we will now discuss, this can get expensive).

Problem #2.

Dollar for dollar, guaranteed issue life insurance policies aren’t always the most affordable when compared to other “types” of life insurance policies out there. Now we don’t want to imply that these “types” of life insurance policies are going to cost a fortune, it’s just that if you can qualify for another “kind” of life insurance policy, that coverage will usually cost less dollar for dollar than a guaranteed issue life insurance policy will.

Problem #3.

Guaranteed issue life insurance policies contain a clause most commonly referred to as a Graded Death Benefit.

Graded Death Benefit Defined:

Graded Death Benefits are “clauses” written into most (if not all) guaranteed issue life insurance policies which state that a guaranteed issue life insurance policy won’t begin to cover an individual from “natural causes” of death until a certain waiting period has elapsed. This “waiting period” will usually last 2 to 3 years and is designed to make sure that someone who knows that they are very close to death from being able to purchase these “types” of life insurance policies.

And while…

This may seem extremely unfair; it’s important to remember that a guaranteed issue life insurance policy isn’t going to require you to take a medical exam or answer any health-related questions. So, at the end of the day, a graded death benefit really is the only thing that allows insurance companies to be able to offer one of these “types” of life insurance policies.

The good news is…

That while you may have to wait for 2 to 3 years for one a Guaranteed Issue Life Insurance policy to provide you true life insurance protection, these “types” of life insurance policies will provide immediate coverage for any “accidental causes” of death and may also provide some kind of “return of premium” to the beneficiaries insured applicants who do end up dying from natural causes before their Graded Death Benefit expiring. It’s like buying a small Accidental Death Policy that will ultimately “turn into” a true-life insurance policy after a period of time.

So, have we confused you yet?

If so, don’t fret we the purpose of this article wasn’t to try to make you an insurance expert. It was just to give you an idea of what questions you’ll want to pursue prior to making any decisions. This brings us to the last topic that we wanted to discuss here in this article, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance professional who will work as an advocate for you.

Such an agent…

Will not only help guide you through the application process but also be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

You’ll want to make sure that you’re completely honest with your life insurance agent before applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best.”

So, what are you waiting for? Give us a call today and see what we can do for you!