In this article, we wanted to take a moment and answer some of the most common questions we get from folks applying for life insurance after being prescribed Warfarin or one of the familiar brand names it sold under, including Coumadin or Jantoven to help treat and prevent blood clots.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Warfarin?

- Why do life insurance companies care if I’ve been prescribed Warfarin?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Warfarin?

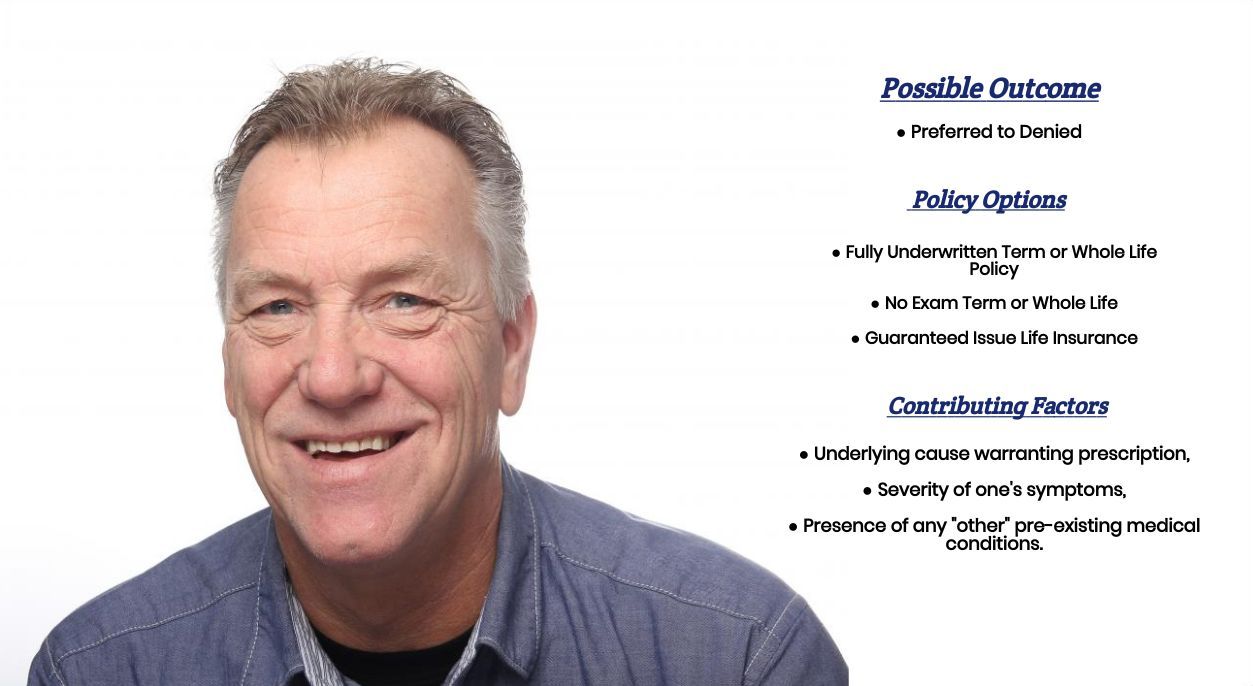

Yes, individuals who have been prescribed Warfarin in the past or who are using Warfarin presently can and often will qualify for a traditional term or whole life insurance policy. In fact, some applicants may even be able to qualify for a Preferred rate.

The problem is, because Warfarin is a prescription medication that is specifically designed to help folks either treat existing blood clots or function as a preventative step against developing future blood clots, it has a “tendency” to be prescribed to folks with a wide range of pre-existing medical conditions. Some of which can be quite serious.

Why do life insurance companies care if I’ve been prescribed Warfarin?

Life insurance companies “care” if an individual has been prescribed Warfarin because it is a prescription medication specifically used to help folks treat existing blood clots and/or help prevent developing new ones—two conditions that can make a life insurance underwriter a bit nervous.

The good news is…

Although being diagnosed with a blood clot is difficult, many life insurance companies understand that once a clot has been discovered and an individual hasn’t suffered from any “major” complications due to having developed it, treatment options tend to be quite favorable.

This is why some individuals may not be able to qualify for a traditional term or whole life insurance policy, while many others may be able to qualify for a Standard or “normal” rate. Heck, some may even be able to qualify for a Preferred rate!

That said, however…

Because there are many reasons an individual might develop a blood clot, one thing you can count on is that before being approved for coverage, the insurance companies will want to ask you a series of questions about your Warfarin prescription and why your doctor felt you needed to begin taking it.

What kind of information will the insurance companies ask me or be interested in?

- When were you first prescribed Warfarin?

- Who prescribed your Warfarin for you? A general practitioner or a cardiologist?

- What led you to receive a Warfarin prescription?

- Have you been diagnosed with a blood clot or blood clots?

- Have you ever suffered from a heart attack or a stroke?

- Is your Warfarin being used as a preventative measure?

- Are you taking any additional prescription medications?

- In the past 12 months, have any of your prescription medications changed in any way?

- In the past 12 months, have you visited or been admitted to a hospital?

- Are you currently working now?

- In the past 12 months, have you applied for or received any disability benefits?

Now, in fairness, we do need to point out that these questions that we just listed are likely only the beginning of the questions that you may need to answer before getting approved for a traditional term or whole life insurance policy because if you have suffered from a heart attack or stroke in the past or have been admitted to a hospital within the last year or so, there is a perfect chance that an insurance underwriter will want to know all about these events as well.

What rate (or price) can I qualify for?

Without knowing the full details of “why” an individual has been prescribed Warfarin, it is essentially impossible to know what “kind” of rate an individual will qualify for. That said, however, there are a few things that we can point out that can help you get a general idea of what you might find once you do decide to apply for coverage.

First off…

Individuals who have been diagnosed with blood clots and who may have suffered from a heart attack or stroke in the past won’t “automatically” be denied coverage. These individuals will still be “considered” eligible, provided their health has improved, and they don’t suffer any lingering effects of their pre-existing medical condition.

Now…

These individuals probably won’t be able to qualify for a Preferred rate. Still, given that most individuals who apply for a traditional term or whole life insurance policy are absent, any pre-existing medical condition won’t qualify for such a rate either; we don’t want you to get too hung up on that.

Instead…

These individuals will more likely be lumped into a “high-risk” category, making the importance of “shopping” one’s options before actually applying for a life insurance policy all the more important. The good news is that if you choose to apply for a life insurance policy with a company like IBUSA, we’ll help you shop dozens of different life insurance companies simultaneously so that this “process” doesn’t become daunting!

This brings us to the last topic we wanted to discuss today, which is…

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true life insurance professional who will work as an advocate for them. Such an agent should be able to guide you through the application process and be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly, you’ll want to ensure you’re completely honest with your life insurance agent before applying for coverage. By doing so, you will be helping them narrow down what options might be the “best.”

Now, will we be able to help out everyone who has been prescribed Warfarin?

No, probably not. But we can tell you that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies.

This way…

If someone can’t qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, call us!

I am interested Life Insurance Policy.

Lillie,

We’d love to help, just give us a call.

Thanks,

InsuranceBrokersUSA

I’m interested in getting a quote

John,

We will have an agent reach out to you shortly.

Thanks,

InsuranceBrokersUSA

I’m on warfarin and I’m looking for good life insurance

Sylvia,

We’d be happy to try and help, just give us a call.

Thanks,

InsuranceBrokersUSA