In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Namenda or its generic form, Memantine, to help treat those suffering from moderate to severe dementia commonly associated with Alzheimer’s disease.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Namenda?

- Why do life insurance companies care if I’ve been prescribed Namenda?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been prescribed Namenda?

For the purposes of this discussion, we are going to limit the focus of this article to those who are simply using Namenda to treat symptoms associated with moderate to severe Alzheimer’s. Now, if you or a loved one is using Namenda for purposes not listed on its “official” medical guide, it’s possible that what we’re now going to discuss may not be applicable to you.

Which is important…

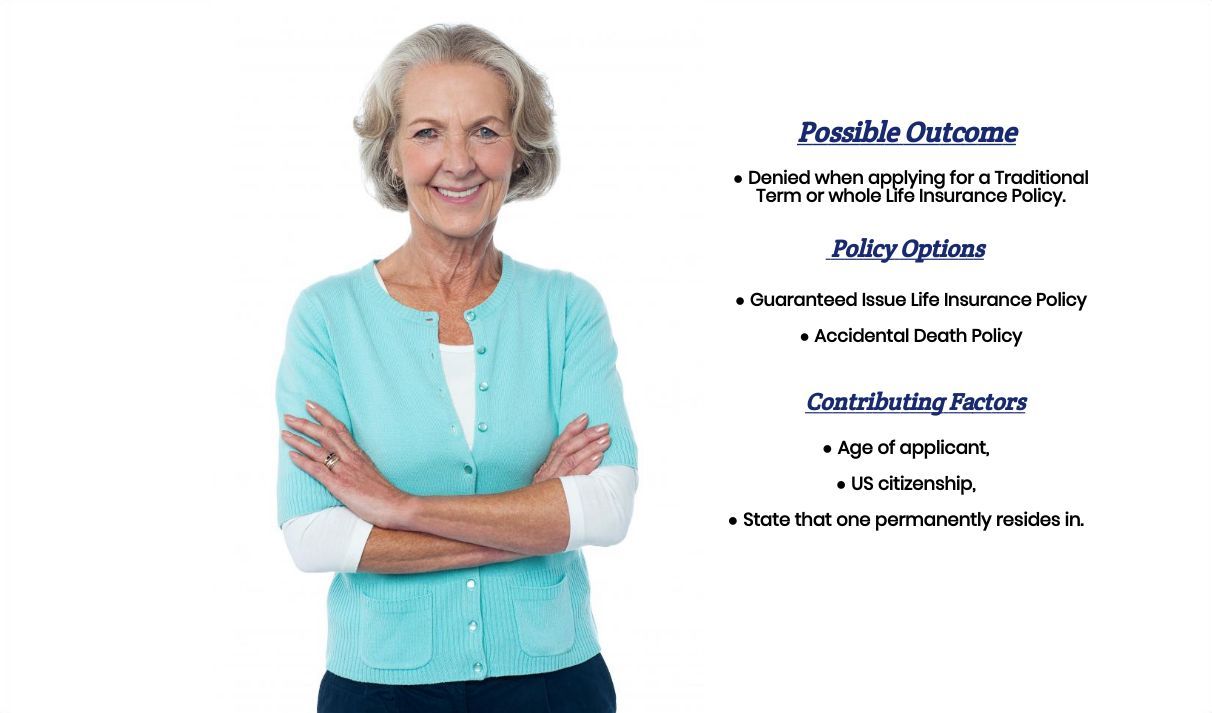

Because Namenda is one of those medications that will typically “trigger” an automatic decline by an insurance underwriter once it appears on your prescription database check. This means that if you have been prescribed Namenda in the past or are currently taking Namenda, you will not be considered eligible for a traditional term or whole life insurance policy.

Why do life insurance companies care if I’ve been prescribed Namenda?

Life insurance companies care that an individual has been prescribed Namenda because it is an easy and cost-effective way to rule out any individuals who have been diagnosed with or are suffering from symptoms that may be related to dementia and/or Alzheimer’s disease. Two medical conditions which most (if not all) traditional life insurance companies will immediately deny coverage for.

What rate (or price) can I qualify for?

Now because most (if not all) life insurance companies are going to immediately deny anyone applying for “traditional” life insurance coverage after having been prescribed Namenda, the next possible option one might want to pursue an “alternative” product such as a guaranteed issue life insurance policy or an accidental death policy.

Two totally…

Different types of products will have their “Pros” and “Cons” associated with each, and ones that should be considered, particularly a guaranteed issue life insurance policy, which can provide coverage up to approximately $25,000 dollars in coverage for death by natural causes once the “graded death benefit” has expired.

The problem is…

Like any other “contract” where two parties agree to provide one another a service for one another, each party must be of sound mind. And in the case where one party may be suffering from a mental impairment, we here at IBUSA feel super uncomfortable “selling” any kind of policy to them. It’s not that we don’t want to help our folks or families who may be suffering from this kind of illness; it’s just that we don’t want to “appear” like we’re taking advantage of anyone.

This brings us to the next segment of our discussion here, which is…

What can I do to help ensure that I get the “best life insurance” for me?

Our advice to anyone who is considering purchasing an alternative product, such as a guaranteed issue life insurance policy or an accidental death policy, is to first take a look at our two articles, which provide the pros and cons of each, and then call on one of the insurance companies that we mention by name directly.

This way, you’ll be better prepared to know if one of these products is right for you and you’ll be working directly with the insurance companies who will be better prepared to determine whether or not the potential insured is fully aware of what he or she is considering purchasing.

You can also…

Feel free to give us a call, and we’ll be more than happy to answer any questions that you may have and point you in the right direction. We just wouldn’t want to actually process any application which could later be “challenged” by an insurance company simply because the insured wasn’t fully aware of the inherent limitations of one of these “alternative products”.