In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Levemir or its generic form, Insulin Detemir, to help treat individuals who have either been diagnosed with type 1 diabetes or type 2 diabetes.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Levemir?

- Why do life insurance companies care if I’ve been prescribed Levemir?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been prescribed Levemir?

Yes, individuals who have been prescribed Levemir can and often will be able to qualify for a traditional term or whole life insurance policy. But, we should warn you from the start that having been prescribed a medication like Levemir certainly complicates things.

Why do life insurance companies care if I’ve been prescribed Levemir?

There are three main reasons why a life insurance company is going to “care” if you’ve been prescribed a medication like Levemir.

The first reason is…

Because Levemir is a prescription medication that is used to help folks treat their diabetes, and regardless of what “kind” of diabetes you’re trying to treat, it will be something that all life insurance underwriters will be concerned about at least in the beginning.

The second reason…

Why life insurance companies “care” if you’ve been prescribed Levemir is because it’s used to help treat both “types” of diabetes. And, when it comes time to get approved for a traditional term or whole life insurance policy, one thing you’re going to find is that getting approved after having been diagnosed with type 1 diabetes is certainly going to be much more difficult than getting approved with type 2 diabetes (in general).

Finally…

Life insurance companies are going to “care” if you’ve been prescribed Levemir because Humalog is an “injectable” form of insulin, which, for some reason (presumably because it’s used to treat more difficult cases) most life insurance companies frown upon.

The good news is that over the past few years ago, there now seems to be an ongoing trend for several life insurance companies to become more “lenient” towards those who have been prescribed Levemir and/or been diagnosed with type 1 diabetes. That is, of course, if you’re speaking with a life insurance agent that has access to some of the different life insurance products which will consider a diabetic using Humalog to treat their diabetes still eligible for a traditional life insurance policy.

Fortunately…

Here at IBUSA, we work very hard to maintain relationships with dozens of different life insurance companies so that when a more “challenging” application approaches us, we should “theoretically” have several options for them to consider. That is, of course, if they’re able to meet the minimum requirements set by these different life insurance companies, which is why we’ll commonly ask many of the same questions you’ll likely encounter from the life insurance companies once you choose to “officially” apply for coverage.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked may include:

- When were you first diagnosed with diabetes?

- Who diagnosed your diabetes? A general practitioner or a specialist?

- What “kind” of diabetes have you been diagnosed with? Type 1 diabetes? Or Type 2?

- What symptoms (if any) led to you discovering the fact that you have diabetes?

- Are you currently experiencing any symptoms related to your diabetes right now?

- Are you currently taking any other prescription medications in addition to your Levemir?

- Have any of your prescription medications, including your Levemir prescription, changed in the past 12 months?

- How often do you see your primary care physician?

- How often do you check your daily blood sugar?

- What would you estimate your daily blood sugar average to be?

- When was the last time you had your A1C checked? What was that value?

- What is your current height and weight?

- In the past 12 months, have you used any tobacco or nicotine products?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

Now at this point…

We should probably mention that these will just be the questions related to the fact that you have been prescribed Levemir and diagnosed with a form of diabetes. Additionally, there will also be a wide variety of other health and lifestyle questions which will also be used to determine what kind of “rate” you might be able to qualify for.

And by “lifestyle”, we mean:

- Do you have any history of drug or alcohol abuse?

- Have you ever been convicted of a felony?

- Do you have any issues with your driving record?

- Do you have any set plans to travel outside of the United States within the next year?

- In the past 2 years, have you applied for bankruptcy?

- Do you currently participate or plan on participating in any dangerous hobbies?

- Etc…

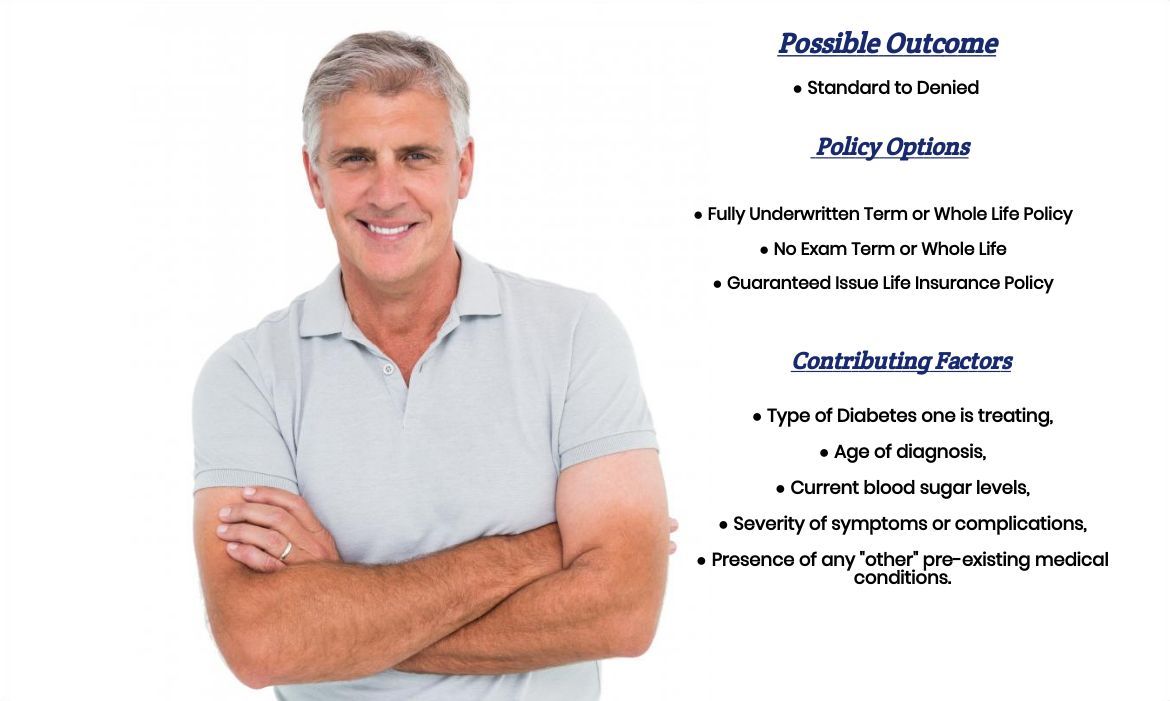

What rate (or price) can I qualify for?

As you can see, there are a lot of factors that can come into play when determining what kind of “rate” you might be able to qualify for. This is why, unfortunately, without knowing more about your particular situation, we would not be able to know for sure what kind of “rate” you would be able to qualify for.

That said, however…

Because you have been diagnosed with a form of diabetes and because you have been prescribed an “injectable” form of insulin, we feel pretty safe in discussing what kind of “rates” you won’t be eligible for, which is why we want to take a moment and actually discuss how life insurance rate work.

In total, there are approximately 14 different life insurance life insurance rates an individual might be able to qualify for. The “best” rate would be a Preferred Plus followed by Preferred, Standard Plus, and then Standard. These are the rates that are typically reserved for individuals who aren’t necessarily categorized as “high risk”.

From there…

You then begin to fall into the “higher risk” rates, which are commonly referred to as Table Rates and range from Table A (which would be considered the “best” or least expensive table rate) all the way to Table J (which would be considered the “worst” or most expensive table rate).

Now with this information in mind, let’s apply this knowledge to what we know about individuals who have been prescribed Levemir. First of all, type 1 diabetics will have a more difficult time being able to qualify for a traditional term or whole life insurance policy. In fact, there are many life insurance companies that won’t be willing to offer coverage to a type 1 diabetic regardless of how well they are managing their condition.

The good news is that…

There are a few companies out there that will provide traditional life insurance coverage to a well-controlled type 1 diabetic, albeit at a “Low” Table Rate, usually around Table F or lower (think Table F-J). And while there are a lot of folks out there who aren’t going to be pleased by receiving such a rate, given the alternative, which would be getting denied, we here at IBUSA would much rather be able to tell someone that they have been approved at a higher premium and try to adjust their coverage or term amount so that their premiums would be affordable then tell them they are “out of luck” altogether.

Now for those…

Who have been diagnosed with type 2 diabetes, what you’re generally going to find is that because you have been prescribed an “injectable” form of insulin, you probably won’t be able to qualify for a Standard rate, but there is a decent chance that you might be able to qualify for a Table Rate somewhere between B-D.

This, of course, is…

Assuming that you were originally diagnosed with type 2 diabetes after the age of 50, that your diabetes has been well under control for at least a year, and that you’re currently not suffering from any kinds of “symptoms” of your disease. Now if this is not the case, you may still be able to qualify for a traditional life insurance policy only now you’ll more likely only be able to qualify for rates below Table D.

The real trick…

Will be “knowing” which life insurance company is going to provide you with the “best” opportunity for success, which is something that we here at IBUSA can help you try and determine, which is why we wanted to take a moment and shift gears a little bit and move on to the last topic we wanted to take a moment and discuss which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance profession who will work as an advocate for you. Such an agent who can help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now does it?

Lastly, you’ll want to make sure that you’re completely honest with your life insurance agent prior to applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best”

So, what are you waiting for? Give us a call today and see what we can do for you!