In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Lantus or its generic form, Glargine, to help treat their diabetes, whether it be type 1 or type2 diabetics.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Lantus?

- Why do life insurance companies care if I’ve been prescribed Lantus?

- What kind of information will the insurance companies ask me or be interested in?

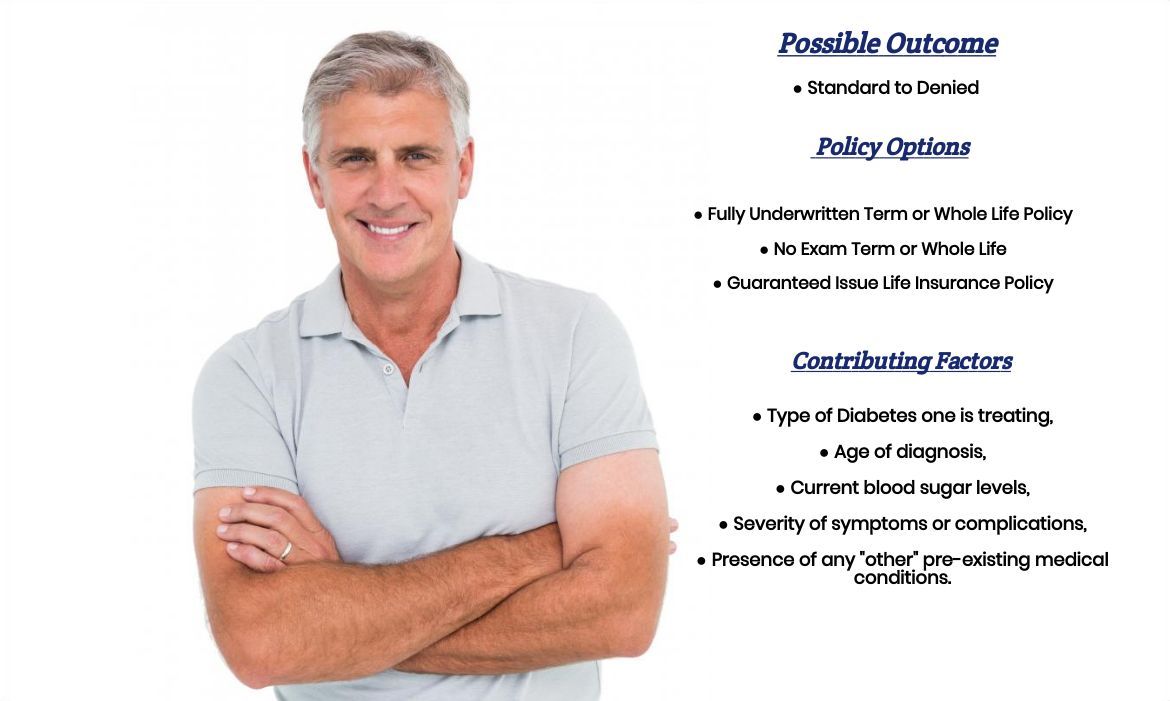

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been prescribed Lantus?

Yes, individuals can and often will be able to qualify for a traditional term or whole life insurance policy after they have been prescribed Lantus. Still, we’ve got to be honest with you, having been prescribed Lantus is certainly going to complicate matters.

Why do life insurance companies care if I’ve been prescribed Lantus?

There are three major reasons why a life insurance company is going to “care” that you’ve been prescribed Lantus.

The first reason is that…

Lantus is a prescription medication that is used to help folks treat their diabetes, which is a pre-existing medical condition that life insurance companies are certainly going to be interested in.

The second reason is that…

Unlike many other “types” of diabetic medications that are specifically designed to either treat type 1 or type 2 diabetes, Lantus can and often is used to treat both type 1 and type 2 diabetes, which is why life insurance companies are going to want to know what “kind” of diabetes you have prior to moving forward with your life insurance application.

And the last reason why…

Life insurance companies are going to “care” if you’ve been prescribed Lantus because Lantus is an injectable form of insulin, which in the “world of life insurance” tends to be more discriminated against than oral forms. Now, we here at IBUSA aren’t entirely sure why this is the case; presumably, it must mean that these must be more “serious” cases of diabetes, but what we can tell you is that. Fortunately, this presumed prejudice is slowly changing among some life insurance companies, which is why you’ll want to be sure that you’re aware of how a life insurance company views “injectable” forms of insulin vs “oral” forms of insulin prior to actually applying for coverage.

One thing that we can say for sure is…

That there was probably a really good reason why your doctor chose Lantus over any other diabetic medication, so the last thing that you would want to do is make any treatment changes simply for the purpose of applying for a life insurance policy. Instead, you’ll just want to make sure that you work with a professional who is aware of these differences and knows what “kind” of questions a life insurance company is likely to ask so that they can help guide you to the insurance company that will provide you with the “best” opportunity for success!

What kind of information will the insurance companies ask me or be interested in?

What you’re going to find is that regardless of what “kind” of diabetes you’ve been diagnosed with, the questions you’ll be asked will typically look the same and focus on the following:

- When were you first diagnosed?

- What symptoms you’ve experienced?

- And how well is your diabetes being managed?

To obtain these basic answers, you’ll probably be asked questions similar to the following:

- What “type” of diabetes have you been diagnosed with?

- At what age were you first diagnosed with Diabetes?

- Who diagnosed your diabetes? A general practitioner or a specialist?

- What symptoms, if any, have you experienced as a result of your diabetes?

- In addition to Lantus, what other prescription medications are you currently taking?

- Have any of your prescription medications changed in any way over the past 12 months?

- How often do you see your primary care physician?

- How often do you check your daily blood sugar?

- What is your daily blood sugar average?

- When was the last time you had an A1C test performed? What was that value?

- Have you been diagnosed with any other serious pre-existing medical condition like kidney disease or heart disease?

- What is your current height and weight?

- In the past 12 months, have you used any tobacco or nicotine products?

- Are you currently working?

- In the past 12 months, have you applied for or received any form of disability benefits?

What rate (or price) can I qualify for?

As you can see, there are a lot of factors that are going to come into play when determining what kind of “rate” an individual will be able to qualify for or in determining whether or not any individual will be able to qualify for coverage at all!

This is why, without knowing the specifics in one’s case, it’s really impossible to make any kind of educated guess as to what the outcome of one’s life insurance application might be. That said, however, there are some things that we can definitely tell you for sure.

Things such as:

- There will be a few life insurance companies that will tell you that Type 1 Diabetics are “uninsurable.” This is false because some life insurance companies will insure Type 1 Diabetics.

Now, will you be able to qualify for one of their policies? Who knows? All we can tell you is that there is a chance, so if someone tells you that Type 1 Diabetics can’t qualify for a traditional term or whole life insurance policy as a whole, you’ll know that it’s time to move on and find another life insurance agent.

- Additionally, there are some life insurance companies that will consider “injectable” forms of insulin as a cause for denying one’s life insurance application regardless of what “kind” of diabetes an individual has been diagnosed with.

So, suppose you’ve been told that you can’t qualify for a traditional term or whole life insurance policy specifically because you have been prescribed a medication like Lantus despite the fact that it is controlling your diabetes very well. In that case, you will definitely want to seek a second opinion prior to making any decisions about seeking out an “alternative” product, such as a guaranteed issue life insurance policy or an accidental death policy.

This brings us to the last topic that we wanted to take a moment and discuss with you here today, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance profession who will work as an advocate for you. Such an agent who can help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly you’ll want to make sure that you’re completely honest with your life insurance agent prior to applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best”

So, what are you waiting for? Give us a call today and see what we can do for you!