In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after having been diagnosed with Cranial Arteritis, Temporal Arteritis, or Giant Cell Arteritis.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been diagnosed with Cranial Arteritis?

- Why do life insurance companies care if I’ve been diagnosed with Cranial Arteritis?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been diagnosed with Cranial Arteritis?

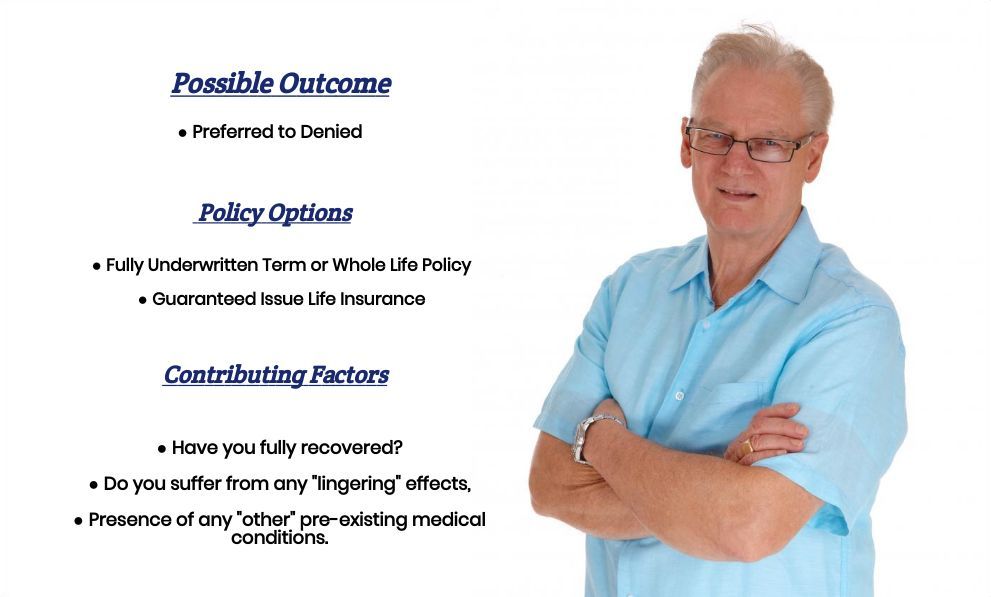

Yes, individuals can and often will be able to qualify for a traditional term or whole life insurance policy after they have been diagnosed with Cranial Arteritis, Temporal Arteritis, or Giant Cell Arteritis.

But, we’ve got to warn you that any time an individual is trying to apply for a life insurance policy after they’ve been diagnosed with a potentially serious pre-existing medical condition like this one, what you’re generally going to find is that your life insurance application is likely to become pretty complicated pretty quickly!

Which is why…

You may want to consider avoiding applying for a no medical exam term life insurance policy and seeing how these policies tend to be more difficult to qualify for after someone has been diagnosed with a pre-existing medical condition like Cranial Arteritis.

Why do life insurance companies care if I’ve been diagnosed with Cranial Arteritis?

Probably the easiest way to answer this question is to simply take a moment to define exactly what Cranial Arteritis is and review some of the most common symptoms associated with this disease. This should give us a pretty good idea why most (if not all) of the best term life insurance companies are going to be a bit hesitant about just immediately approving one’s application after having been diagnosed with this condition.

Cranial Arteritis, Temporal Arteritis, and Giant Cell Arteritis Defined:

Cranial Arteritis is a pre-existing medical condition where the temporal arteries, which are responsible for providing the brain a steady flow of oxygen-rich blood, become inflamed and/or damaged.

Symptoms of Temporal Arteritis may include:

- Double vision,

- A sudden and often permanent loss of vision in one eye,

- Severe throbbing headaches,

- Fatigue,

- Weakness,

- Unexplained loss of appetite,

- Jaw pain,

- Etc…

Fortunately…

Temporal Arthritis can be treated and is often curable, assuming that one has access to proper medical care and does not ignore their condition. This explains why, even though this may become a very serious medical condition, many life insurance companies will still consider someone who has been diagnosed with Giant Cell Arthritis (GAC) still “potentially” eligible for coverage.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked may include:

- When were you first diagnosed with Cranial Arteritis?

- Who diagnosed your Cranial Arteritis?

- What symptoms (if any) led to your diagnosis?

- What treatment options have you pursued to treat your Cranial Arteritis?

- Are you still experiencing symptoms due to your Cranial Arteritis?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you currently taking any prescription medications?

- In the past two years, have you been admitted to a hospital for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

Now at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any kind of “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like this one, find and qualify for the life insurance coverage that they are looking for.

But…

It’s not so great if you’re looking for answers to any specific medical questions. In cases like these, we recommend that you contact a true medical professional who has the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What rate (or price) can I qualify for?

As you can see, many factors can come into play when trying to determine what kind of “rate” an individual might be able to qualify for after having been diagnosed with Cranial Arteritis. That’s why it’s pretty much impossible to know for sure what kind of “rate” you might be able to qualify for without first speaking with you for a few minutes.

After all…

It’s important to understand that beyond just the questions that we’ve listed above, which will focus on the fact that you have been diagnosed with Cranial Arteritis, insurance companies are also going to be interested in your:

- Family medical history,

- Driving record,

- Travel history,

- Hobbies,

- Etc…

That said, however…

There are a few “assumptions” that will generally hold true about most people who have been diagnosed with Cranial Arteritis. These assumptions may help you get a better idea about what kind of rate you might be able to qualify for.

For example…

While it is true that individuals who have been diagnosed with Cranial Arteritis can and often will be able to qualify for a traditional term or whole life insurance policy, they will typically not qualify for a Standard or Better rate.

Which means that…

In most cases, you will automatically be considered a “higher-risk” applicant. As a result, you’ll most likely need to submit your medical records along with your life insurance application prior to any insurance company being willing to make any kind of decision about your application.

The good news is…

This is something that we here at IBUSA work with every day, so it’s not something that we’re unfamiliar with or that we won’t be able to facilitate for you. This brings us to the last topic that we wanted to take a moment and discuss with you, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true life insurance professional who will work as an advocate for them.

Such an agent…

Will not only help guide you through the application process but also be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

You should be completely honest with your life insurance agent before applying for coverage. By doing so, you will help him or her narrow down what options might be the “best.”

So, what are you waiting for? Give us a call today and see what we can do for you!

Now, will we be able to help out everyone who has been previously diagnosed with Cranial Arteritis?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, just give us a call!