In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after they have been diagnosed with Arteriovenous Malformation (AVM).

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been diagnosed with an Arteriovenous Malformation (AVM)?

- Why do life insurance companies care if I’ve been diagnosed with an Arteriovenous Malformation (AVM)?

- What kind of information will the insurance companies ask me or be interested in?

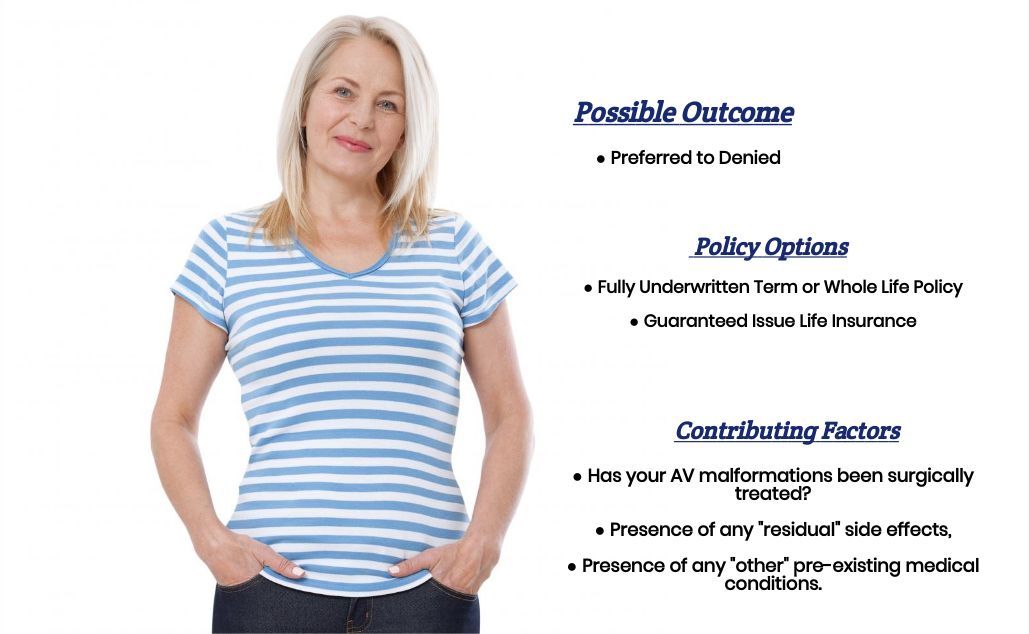

- What rate (or price) can I qualify for?

- How can I help ensure I get the “best life insurance”?

So, without further ado, let’s dive right in!

Can I qualify for life insurance after I’ve been diagnosed with an Arteriovenous Malformations (AVM)?

Yes, individuals who have been diagnosed with an Arteriovenous Malformation can and often will be able to qualify for a traditional term or whole life insurance policy. The only problem is that to do so, it (or they) will first need to have dealt with their “malformation” before being considered eligible for coverage.

Why do life insurance companies care if I’ve been diagnosed with an Arteriovenous Malformation (AVM)?

The best way to understand why a life insurance company is likely to “care” if an individual has been diagnosed with an arteriovenous malformation would be to first look at how these pre-existing medical conditions are defined…

Arteriovenous Malformation (AVM) Defined

An AVM is clinically defined as an abnormal “tangle” or “jumble” of blood vessels connecting arteries and veins. Thus, normal blood flow and oxygen circulation become disrupted.

As a result, the oxygen-rich blood that should be reaching the brain becomes “diluted,” causing a variety of different symptoms depending on how severe the “tangle” or “jumble” is. Symptoms such as:

- Dizziness,

- Headaches,

- Internal bleeding,

- Nausea and vomiting,

- Seizures,

- Muscle weakness and/or even possible partial paralysis,

As well as even the potential for progressive loss of neurological functioning. This is why it’s no wonder that a life insurance underwriter will want to know more about your situation before making any definitive decisions about your life insurance application.

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked may include:

- When were you first diagnosed with Arteriovenous Malformations?

- Who diagnosed your Arteriovenous Malformations? A general practitioner or a specialist?

- What symptoms (if any) led to your diagnosis?

- How have you treated your AVM?

- Medications?

- Surgery?

- Will you require any further treatments?

- If you’ve had a surgical procedure to correct your AVM, when was that?

- Are you currently suffering from any symptoms related to your condition?

- Have you been diagnosed with any other “serious” pre-existing medical conditions?

- Have you ever suffered from a heart attack or stroke?

- In the past 12 months, have you used any tobacco or nicotine products?

- In the past two years, have you been hospitalized for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

Now, at this point, we usually remind folks that nobody here at IBUSA is a medical professional, and we’re certainly not doctors. This is why, if you have any specific medical questions you would like to have answered, the last thing that we would recommend that you do is ask us!

After all…

We’re just a bunch of life insurance agents who are good at helping folks find and qualify for the “type” of life insurance they’re looking for. So, we recommend calling a doctor if you’re looking for medical answers. But if you’re looking for answers you may have about how your AVM might affect your chances of qualifying for a quality life insurance policy, keep on reading!

What rate (or price) can I qualify for?

As you can see above, many factors can come into play when determining what kind of “rate” an individual might qualify for when applying for a traditional term or whole life insurance policy. This is why it’s pretty much impossible to know for sure what kind of “rate” you might qualify for without first speaking with you for a few minutes.

That said, however there are a few “assumptions” that we can make about those who have been diagnosed with Arteriovenous Malformations and either haven’t received any surgical procedure to fix it or have just very recently had surgery performed.

For example…

Suppose you recently had your AVM surgically treated; most life insurance companies. In that case, even No Medical Exam Life Insurance Policies will want to wait at least six months before they will be willing to consider you “potentially” eligible for coverage. Then, at that point, they will want to see that you aren’t suffering from any “serious” lingering effects from your AVM, at which point you may then become eligible for a “substandard” or “high risk” rate.

That’s the good news…

The bad news is that if your AVM is located within the brain and you haven’t or aren’t able to have it surgically corrected, most (if not all) life insurance companies are going to consider you ineligible for a traditional term or whole life insurance policy. In cases like these, we here at IBUSA will first want to exhaust all “traditional” options before we suggest possibly looking at either a guaranteed issue life insurance policy or an accidental death policy.

This brings us to the last topic that we wanted to take a moment and discuss with you here today, which is…

How can I help ensure I get the “best life insurance”?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance profession who will work as an advocate for you. Such an agent who can help guide you through the application process and help you be perfectly “frank” about what options may or may not be possible.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now do

Lastly, before applying for coverage, you’ll want to be completely honest with your life insurance agent. By doing so, you will be helping them narrow down what options might be the “best.”

Now, can we help out everyone previously diagnosed with an AVM?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to see what options might be available, call us!