In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after being diagnosed with Erythema Multiforme (recovered).

Questions that will be directly addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Erythema Multiforme?

- Why do life insurance companies care if I’ve been diagnosed with Erythema Multiforme?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance if I have been diagnosed with Erythema Multiforme?

Yes, individuals can and often will be able to qualify for a traditional term or whole life insurance policy after they have been diagnosed with Erythema Multiforme. In fact, they may even be able to qualify for a no exam life insurance policy at a Preferred Plus rate!

The problem is…

That most, if not all of the best life insurance companies are going to want to make sure that you have fully recovered from your Erythema Multiforme “infection” and that you don’t suffer from some “other” pre-existing medical condition which could make you susceptible to these types of outbreaks.

Why do life insurance companies care if I’ve been diagnosed with Erythema Multiforme?

At the end of the day, most life insurance companies aren’t really going to “care” if you have previously been diagnosed with Erythema Multiforme provided that you are no longer suffering from this condition and that you don’t seem to have any serious “lingering effects” from your infection.

This is mainly because…

While Erythema Multiforme is a condition that is caused by one’s own body “over-reacting” to an infection, the “over-reaction” isn’t one that causing any potential life-threatening symptoms. It’s just going to cause someone to suffer from some pretty “horrific” skin lesions that will take a while to disappear!

And since…

Most life insurance companies are going to want to make sure that you fully recover from an Erythema Multiforme outbreak before they are willing to process your life insurance application.

Which is why…

It makes sense for us to briefly describe what Erythema Multiforme is a mention some of the most common symptoms of this disease so that you’ll have a better idea about what a life insurance underwriter will be looking for when considering your application.

Erythema Multiforme Defined:

Erythema Multiforme is a condition that occurs when one’s own body becomes hypersensitive to some kind of external environmental factor. The most common cause will usually involve an infection by the herpes simplex virus (HSV).

The “bad part” about…

Erythema Multiforme is that it will usually present itself as a skin lesion, usually in the form of a “target” like shape. The “good part” about Erythema Multiforme is that these lesions will usually heal by themselves. Still, some folks will benefit by taking an antihistamine, an analgesic, and or anti-itching creams.

Common symptoms may include:

- Circular “target” like sores,

- Red patches and blisters usually centered on palms of the hand, face, and soles of the feet,

- Fatigue,

- Cold sores,

- Joint pain,

- Fever,

- Etc…

Now at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any kind of “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like this one, find and qualify for the life insurance coverage that they are looking for.

But…

Not so great if you’re looking for answers to any specific medical questions. In cases like these, we would recommend that you contact a true medical professional who has the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What kind of information will the insurance companies ask me or be interested in?

Erythema Multiforme is one of those “kinds” of pre-existing medical conditions, which is only going to play a role in the outcome of one’s life insurance application if you are applying for coverage with an “active” infection.

This is because…

Once you have recovered from your Erythema Multiforme “attack,” most life insurance companies aren’t going to hold this previous diagnosis against you. That is, of course, assumes that you don’t have some other “kind” of pre-existing medical condition that might make you more susceptible to suffering from a viral infection, which might trigger the “over-reaction,” which is the ultimate cause of Erythema Multiforme. This is why you may be asked the following questions about your Erythema Multiforme in addition to the “normal” life insurance application questions that just about everyone will be asked.

Common questions such as:

- When were you first diagnosed with Erythema Multiforme?

- How many times have you suffered from Erythema Multiforme?

- Have you been diagnosed with any other pre-existing medical conditions?

- Have you fully recovered your “attack”?

- Do you suffer from any lingering effects from your “attack”?

- Are you taking any prescription medications now?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

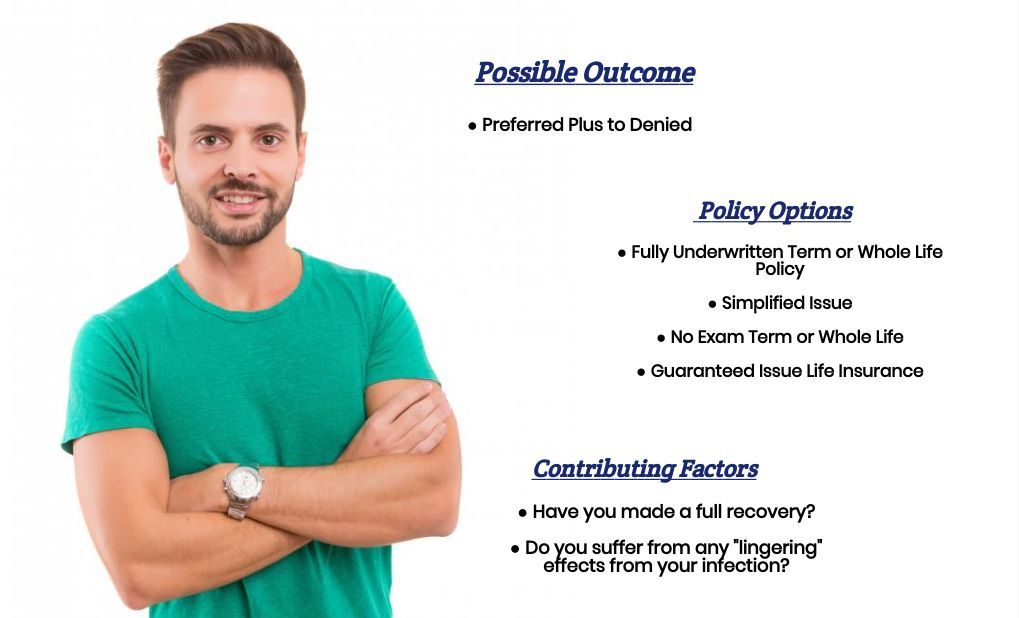

What rate (or price) can I qualify for?

Because there are so many factors that can come into play when trying to determine what kind of “rate” that an individual might be able to qualify for, it’s pretty much impossible to know for sure what kind of “rate” that you might be able to qualify for without first actually speaking with you.

That said however…

It’s fair to say that if you have fully recovered from y our Erythema Multiforme and you don’t seem to be suffering from any kind of pre-existing medical condition which could make you more susceptible to suffering from Erythema Multiforme, what you’re most likely going to find is that whatever rate that you would have been able to qualify for PRIOR to being diagnosed with Erythema Multiforme should be the same “rate” that you will be able to qualify for AFTER having been diagnosed with Erythema Multiforme.

“Which is great!”

And segues very nicely into the last topic that we wanted to discuss here in this article, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true-life insurance professional who will work as an advocate for you.

Such an agent…

Will not only help guide you through the application process but also be perfectly “frank” with you about what options may or may not be possible for you.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly…

You’ll want to make sure that you’re completely honest with your life insurance agent before applying for coverage. By doing so, you will be helping him or her narrow down what options might be the “best.”

So, what are you waiting for? Give us a call today and see what we can do for you!

Now, will we be able to help out everyone who has been previously diagnosed with Erythema Multiforme?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Burial Life Insurance Companies as well so that in the event that someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.