In this article, we wanted to take a moment and try and answer some of the most common questions we get from folks applying for life insurance after being diagnosed with Empyema.

Questions that will be directly addressed will include:

- Can I qualify for life insurance if I have been diagnosed with Empyema?

- Why do life insurance companies care if I’ve been diagnosed with Empyema?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance if I have been diagnosed with Empyema?

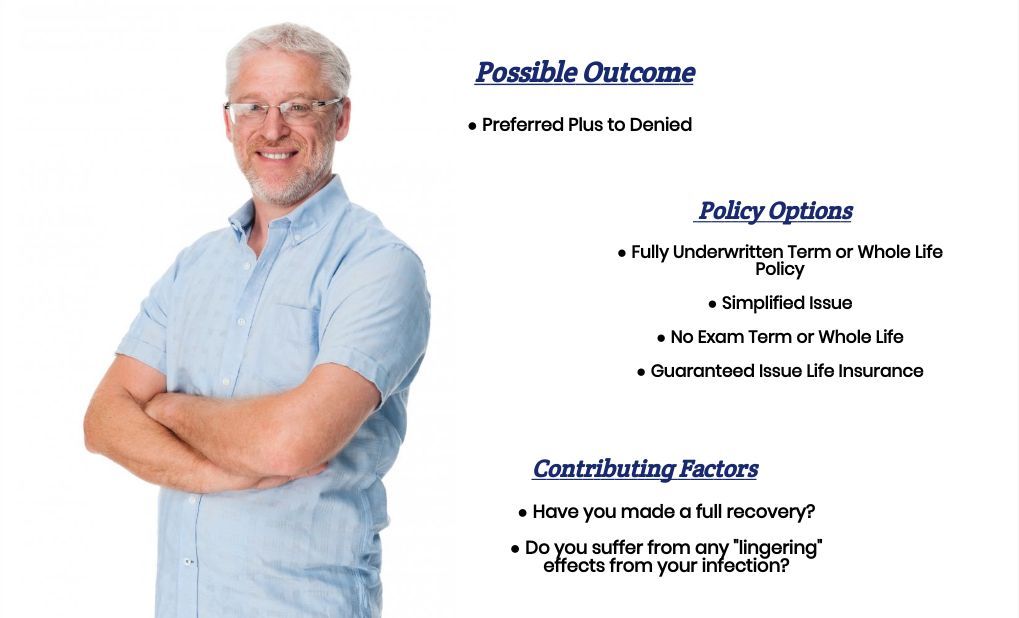

Yes, individuals who have been diagnosed with Empyema can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, they may even be able to qualify for a life insurance policy that won’t require a medical exam at a Preferred rate!

The only problem is…

That before an individual will be able to qualify for a traditional term or whole life insurance policy most (if not all) of the best life insurance companies (in our humble opinion) are going to want to make sure that the applicant has completely recovered from their Empyema and they also will want to fully understand “why” an individual developed Empyema in the first place.

Why do life insurance companies care if I’ve been diagnosed with Empyema?

Pretty much any time an individual develops a “serious” infection, it’s pretty safe to assume that a life insurance company would be interested in learning a little more about that “infection” prior to making any kind of definitive decision about their life insurance application.

Which is why…

It shouldn’t be a huge surprise that when an individual is diagnosed with Empyema, most life insurance underwriters know why this occurred? They’re also going to be interested in whether or not their Empyema caused any permanent damage to your lungs. For this reason, we wanted to take a brief moment and describe what Empyema is as well as take a moment or two and list some of the most common symptoms of Empyema which the life insurance companies are going to be most interested in.

Empyema Defined:

Empyema is a condition where pus collects or gathers in the space between the lungs and the inner surface of the chest wall in an area commonly referred to as the pleural space. For this reason, Empyema can also frequently be referred to as pyothorax or purulent pleuritis.

Common causes of Empyema include:

- Bacterial pneumonia,

- Tuberculosis,

- Lung abscess,

- Chest injuries,

- Chest surgery.

Common symptom may include:

- A dry and persistent cough,

- Chest pain,

- Excessive sweating, night sweats,

- Fatigue,

- Difficulty breathing,

- Labored breathing,

- Unexplained weight loss,

- Fever and chills.

Fortunately…

Empyema is a treatable condition that typically won’t cause any permanent or lasting damage to one’s body provided that an individual seeks out medical treatment once he or she realizes they may be suffering from a respiratory infection. That said, however, the development of fibrosis within the lung damage can sometimes occur. This is why most life insurance companies will want to know that you have fully recovered from your infection before approving your life insurance application.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked may include:

- When were you first diagnosed with Empyema?

- What symptoms (if any) led to your Empyema diagnosis?

- Who diagnosed your Empyema? A primary care physician or a specialist?

- Do you know “why” you developed Empyema?

- Have you been diagnosed with:

-

- Bacterial pneumonia?

- Tuberculosis?

- Lung abscess?

- Chest injuries?

- Chest surgery?

- How did you treat your Empyema?

- Are you currently taking any prescription medications?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you suffering from any “lingering” effects from your Empyema?

- Have you been diagnosed with any lung damage or other respiratory diseases?

- In the past 12 months, have you used any tobacco or nicotine products?

- In the past 12 months, have you applied for or received any form of disability benefits?

-

Now at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any “official” medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who just happen to be really good at helping folks with pre-existing medical conditions like this one, find and qualify for the life insurance coverage that they are looking for.

But…

Not so great if you’re looking for answers to any specific medical questions. In cases like these, we would recommend that you contact a true medical professional who has the training to help. For everyone else, you’re in luck because now we’re going to get into some of the “nitty-gritty” about what you may or may not be able to qualify for.

What rate (or price) can I qualify for?

When it comes time to help an individual diagnosed with Empyema, we usually find ourselves categorizing each applicant into one or two groups. The first group will be those who have simply developed Empyema due to some “condition,” which, once resolved, is likely not to return.

Cases such as:

- Traumatic injuries,

- Surgical procedures,

- Bacterial infections.

The second group…

Would then include cases where the Empyema might not actually be considered the “true” pre-existing medical condition. Rather it is more of a symptom of some larger issue, which will usually be what dictates what kind of life insurance policy and/or rate one would be able to qualify for.

We do this because…

In cases where an individual as developed Empyema but has fully recovered from there infection and doesn’t “seem” to be at risk of suffering from this condition again, chances are your previous Empyema diagnosis isn’t going to play a role in the outcome of your current life insurance application. Or to put it another way, whatever “rate” that you would have been able to qualify for PRIOR to being diagnosed with Empyema should be the same “rate” that you would be able to qualify for AFTER having been diagnosed with Empyema.

“Which is great!”

Now as for those…

Who have developed Empyema as a symptom of some “other” condition which might occur again, what we would encourage you to do is check out our Life Insurance With Pre-Existing Conditions page where we might have an article focusing exclusively on this condition which has caused you to develop Empyema.

The good news is…

That regardless of your situation, we here at IBUSA can help because we have tons of experience helping folks with all sorts of pre-existing medical conditions like yours and are committed to helping all of our clients find the “best” life insurance policy that they can qualify for.

This brings us to the last topic that we wanted to take a moment and discuss, which is…

What can I do to help ensure that I get the “best life insurance” for me?

In our experience here at IBUSA, what we have found that usually, the folks who seem to find the “best” life insurance policy for them are those that:

- Take their time reviewing their options.

- Ask a lot of questions.

And seek out those life insurance agents who not only have experience working with individuals who have been diagnosed with a wide variety of pre-existing medical conditions but also have access to dozens of different life insurance companies so that when it comes time to helping a more “challenging” case, they don’t have to rely on a…

“One size fits all approach!”

The good news is that this is exactly what you’re going to find here at IBUSA!

Now, will we be able to help out everyone who has been previously diagnosed with Empyema?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Guaranteed Issue Insurance Companies as well so that in the event that someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.