In this article, we wanted to take a moment and try to answer some of the most common questions we get from folks applying for life insurance with Chorea, whether it be Huntington’s Chorea or Sydenham’s Chorea.

- Can I qualify for life insurance if I have been diagnosed with Chorea?

- Why do life insurance companies care if I have been diagnosed with Chorea?

- What kind of information will the insurance companies ask me or be interested in?

- What “rate” can I qualify for?

- How can I help ensure I get the “best life insurance” for me?

So, without further ado, let’s dive right in!

Can I qualify for life insurance if I have been diagnosed with Chorea?

When trying to determine whether or not an individual will be able to qualify for a traditional term or whole life insurance policy, it’s important to understand that there are actually two “types” of Chorea, each of which will be treated quite differently by the life insurance industry.

This is why when an individual asks us if they can qualify for a traditional life insurance policy after being diagnosed with Chorea, the first question we will ask is…

“What kind of Chorea?”

If you’ve been diagnosed with Huntington’s Chorea, there are only a couple of life insurance companies that will consider you eligible for a traditional life insurance policy.

So..

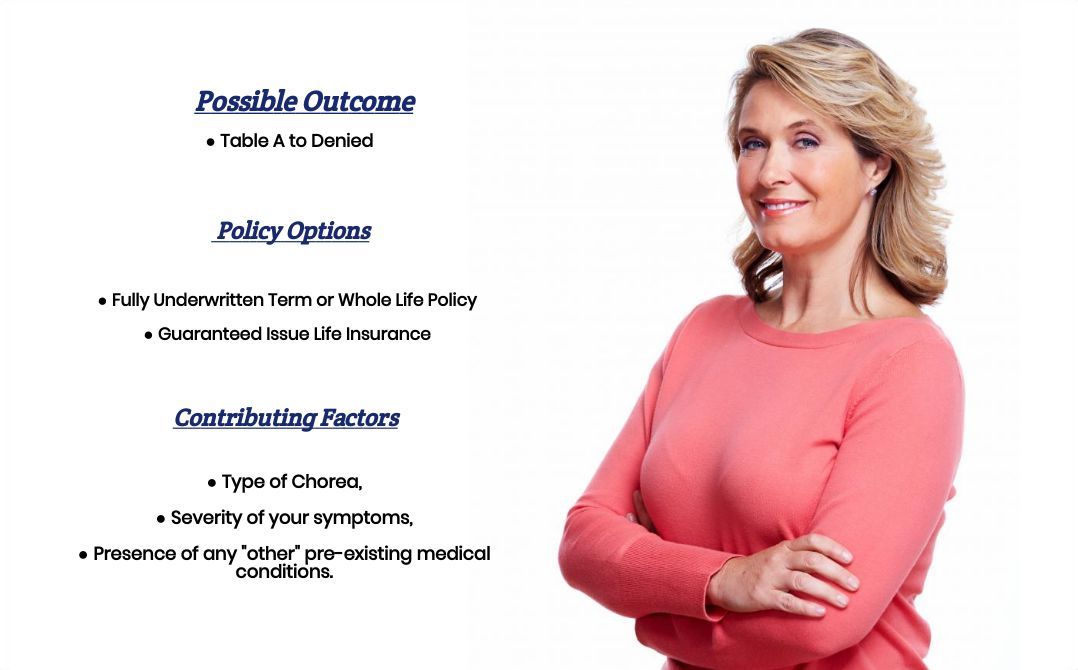

You’re going to need to be very “selective” about which life insurance companies you apply with; otherwise, if you’d still like to purchase some protection for your family, you will need to pursue some “alternative” product, such as a guaranteed issue life insurance policy or an accidental death policy. And as for those who have been diagnosed with Sydenham’s Chorea, the good news is that you may qualify for a traditional term or whole life insurance policy. In fact, you may even be eligible for a no-medical-exam life insurance policy as well.

The only problem is that…

Most of the top-rated life insurance companies we are familiar with will want to ensure that you have fully recovered from your condition before moving forward with your life insurance application.

Why do life insurance companies care if I have been diagnosed with Chorea?

The easiest way to understand why a life insurance company will “care” if an individual has been diagnosed with Chorea is to look at exactly what Chorea is and how Sydenham’s Chorea is going to differ from Huntington’s Chorea.

Chorea Defined:

Chorea is a movement disorder that causes its victims to suffer from involuntary, unpredictable body movements.

- Sydenham’s Chorea Defined:

- Sydenham’s cholera, also commonly referred to as cholera minor or St Vitus’ Dance, is a disease characterized by rapid, uncoordinated “jerky” movements that primarily affect a patient’s face, hands, and/or feet. Additional symptoms may include slurred speech, headaches, muscle weakness, and seizures.

It is believed…

A strain of streptococcal bacteria causes Sydenham’s Chorea, and while some individuals may have a genetic proponent that may make them more “susceptible” to this disease, Sydenham’s Chorea itself does not seem to be a “genetic” disorder one should necessarily worry about passing to any future generations.

Treatment options…

It may include various medications, including prophylactic penicillin, antipsychotic and anticonvulsant medications, and immunomodulatory therapy. The good news is that nearly 50% of those diagnosed with acute Sydenham’s Chorea may spontaneously recover after just a few weeks of suffering from this condition.

Huntington’s Disease Defined:

Unlike Sydenham’s cholera, which seems to be caused by a bacterial infection, Huntington’s cholera is an inherited disorder that results in the death of brain cells. Unfortunately, there is no cure for Huntington’s Disease or Huntington’s cholera, which is why most (if not all) life insurance companies won’t offer traditional life insurance policies to those who have been diagnosed with this condition.

Common symptoms may include:

- Impaired gait, posture, and balance,

- Dystonia,

- Involuntary “jerky” movements,

- Slow or abnormal eye movements,

- Difficulty speaking and or swallowing.

What kind of information will the insurance companies ask me or be interested in?

Typical questions you’ll likely be asked may include:

- When were you first diagnosed with Chorea?

- What “kind” of Chorea have you been diagnosed with?

- Huntington’s Disease?

- Sydenham’s Chorea?

- Who diagnosed your Chorea? A general practitioner or a specialist?

- What symptoms (if any) led to your diagnosis?

- What treatment options (if any) are you pursuing?

- Do you still suffer from any symptoms of your Chorea?

- Over the past 12 months, have your symptoms improved? Worsened? Or remained Stable?

- In the past two years, have you been hospitalized for any reason?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

Now, at this point…

We usually like to take a moment and remind folks that nobody here at IBUSA has any medical training, and we’re certainly not doctors. All we are is a bunch of life insurance agents who are really good at helping folks with pre-existing medical conditions like Chorea find and qualify for the life insurance coverage they are looking for. So, without further ado, let’s look at what rates an individual diagnosed with Chorea might qualify for!

What “rate” can I qualify for?

One of the first things that we want to point out is that many “factors” can come into play when trying to determine what kind of “rate” an individual might qualify for. And, the list of questions that we listed above is just a “few” that are going to specifically relate to the fact that you’ve been diagnosed with some form of Chorea. There will also be a whole “bunch” of additional questions that an insurance underwriter is also going to want to ask, which will be similar to questions everyone gets invited, such as:

- How old are you?

- What are your current height and weight?

- Do you use any tobacco products?

- Have you been diagnosed with any other pre-existing medical conditions?

- Do you have a family history of heart disease or cancer?

- Etc…

For this reason, it’s pretty much impossible for us to know for sure what kind of “rate” you might be able to qualify for without first speaking with you directly.

That said, however…

There are a few “assumptions” that we can make on the fact that you have been diagnosed with Chorea that will generally hold true. For example, if you have been diagnosed with Huntington’s Chorea or Huntington’s Disease, most life insurance companies are going to “automatically” deny your application for traditional coverage.

Which means that…

If you’ve been diagnosed with Huntington’s Chorea. In that case, you’re going to need to be very “selective” with which life insurance companies you choose to apply; otherwise, you will need to pursue some “alternative” product such as a guaranteed issue life insurance policy or accidental death policy if you’d still like to purchase some protection for your family.

Now, as for those…

Who have been diagnosed with Sydenham’s Chorea, what you’re generally going to find is that there ought to be more life insurance companies willing to approve your life insurance application; however, most (if not all) will only be willing to do so at a “higher-risk” classification which means that when you are “shopping” of coverage, you’ll want to start your search with companies that are known to provide some of the most competitive pricing at these rates so that you don’t end up paying too much for your insurance!

This brings us to the last topic we wanted to discuss here in this article, which is…

How can I help ensure I get the “best life insurance” for me?

In our experience here at IBUSA, what works best for folks who have been diagnosed with a pre-existing medical condition where the “severity” of the condition is often “subjective” is for the applicant to make sure that they first find a true life insurance professional who will work as an advocate for them. Such an agent who can help guide you through the application process and be perfectly “frank” with you about what options may or may not be possible.

From there…

You’ll also want to make sure that the very same agent you have chosen has access to dozens of different life insurance companies because, after all, it really doesn’t matter how “great” of a life insurance agent you might have if they don’t have access to the “best” life insurance policy for you! Now, does it?

Lastly, before applying for coverage, it would be best to be completely honest with your life insurance agent. By doing so, you will help them narrow down what options might be the “best. ” So, what are you waiting for? Give us a call today and see what we can do for you!

I have been tested positive for HD Huntingtons Disease. Im not symptomatic (chorea) I’m 34yrs old. Im interested in purchasing life insurance and need help.

Jessica,

We’ll have an agent reach out to you via email so that hopefully we’ll be able to help you find what you are looking for.

Thanks,

InsuranceBrokersUSA.