In this article, we wanted to take a moment to answer some of the most common questions we get from folks applying for life insurance after they have been prescribed Guaifenesin or one of the common brand names it is sold under, including:

- Allfen,

- Diabetic Tussin EX,

- Geri-Tussin

- Guaifenex PSE (Pseudoephedrine-Guaifenesin),

- Mucinex,

- Refenesen,

- Siltussin SA,

- Tussin Expectorant,

- Tussin Mucus-Chest Congestion,

- Tussin Honey,

Along with a host of other brands, all designed to help folks recover from colds involving mucus development in the head, throat, and lungs.

Questions that will be directly addressed will include:

- Can I qualify for life insurance after I’ve been prescribed Mucinex?

- What kind of information will the insurance companies ask me or be interested in?

- What rate (or price) can I qualify for?

- What can I do to help ensure that I get the “best life insurance” for me?

So, without further ado, let’ dive right in!

Can I qualify for life insurance after I’ve been prescribed Mucinex?

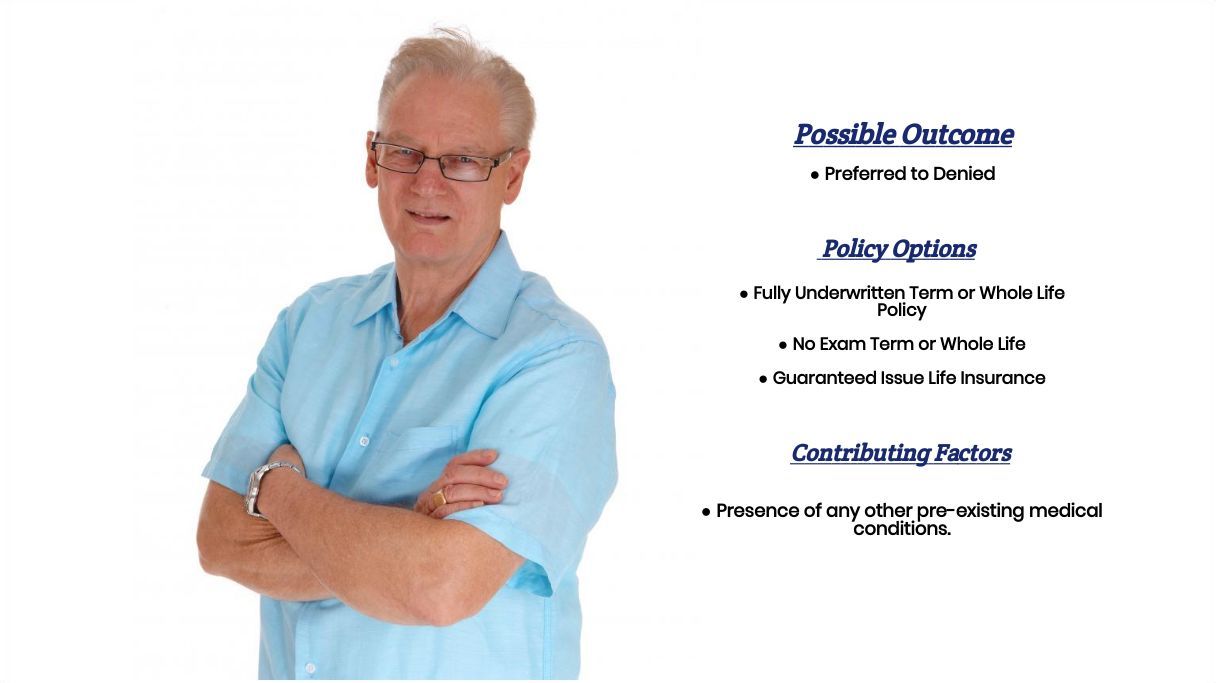

Yes, individuals who have been prescribed Mucinex can and often will be able to qualify for a traditional term or whole life insurance policy. In fact, some may even be able to qualify for some of the best no-medical-exam life insurance policies at a Preferred rate! This is why, in most cases, we as life insurance agents rarely learn that an individual has been prescribed Mucinex unless, of course, it’s right during their life insurance application, in which case we usually will advise that a client do one of two things.

First…

If they are determined to apply for a traditional term or whole life insurance policy, which will require them to take a medical exam, we’ll usually advise our clients to be sure to take their medical exam after they have fully recovered from their illness. This way, they are more likely to do better on their life insurance paramedical exam, which will play a large role in determining what kind of “rate” they will be able to qualify for.

But…

That’s just one option that we’ll suggest. The second option that we might suggest, assuming that our client is “healthy” even though they are currently suffering from a cold, is to apply for a traditional term or whole life insurance policy, which won’t require them to take a medical exam.

These types of…

Life insurance policies will still require one to answer a series of medical questions and will still order background checks on one’s:

- Prescription medication history,

- Driving record,

- Criminal record,

- And credit (in some cases),

But will not require one to provide a blood and urine sample. Which can be quite beneficial for a variety of issues, including:

- Not having to wait for your cold to go away in order to complete your life insurance application.

- Not having to wait for 2 to 4 weeks (or more) to get approved for coverage after taking a medical exam finally.

- And not having to run the risk of actually being diagnosed with some kind of pre-existing medical condition during your medical exam, such as:

- High blood pressure,

- High cholesterol,

- Or diabetes (high blood sugar).

Now, we here at IBUSA, aren’t necessarily “married” to one option vs. another, we just always like to provide our clients with a variety of options so that they can be sure that they are getting the “best” policy for them based on their wants and needs. That said, however, what we can tell you is that regardless of what option you choose, you will typically be asked a series of questions during your life insurance application which will all be designed to try and determine what “kind” of risk you would pose to the insurance company should you end up being approved.

What kind of information will the insurance companies ask me or be interested in?

Common questions you’ll likely be asked may include:

- What is your date of birth?

- What is your gender?

- Are you a United States citizen?

- What is your current height and weight?

- Have you ever been diagnosed with any pre-existing medical conditions?

- Have you ever been diagnosed with cancer, heart disease, or diabetes?

- Have you ever suffered from a heart attack or stroke?

- Have any of your immediate family members (mother, father, brother, or sister) ever been diagnosed with cancer, heart disease, or diabetes? Have any of them ever suffered from a heart attack or stroke?

- Are you taking any other prescription medication other than Mucinex?

- In the past two years, have you ever been hospitalized?

- In the past 12 months, have you used any tobacco or nicotine products?

- Do you have any issues with your driver’s license? Issues such as multiple moving violations, DUI, or a suspended license?

- Do you currently participate or plan on participating in any dangerous hobbies?

- Do you have any set plans to travel outside of the United States in the next year?

- Are you currently working now?

- In the past 12 months, have you applied for or received any form of disability benefits?

What rate (or price) can I qualify for?

Now, as you can see, there are a lot of factors that can come into play when it comes to determining what kind of “rate” an individual might be able to qualify for. This is why without knowing more about you specifically, we really wouldn’t have any idea what kind of “rate” you might receive. What we can tell you for sure is that assuming that you don’t take your medical exam while fully in the midst of a horrible cold, the fact that you’ve been prescribed Mucinex really shouldn’t have any kind of effect on the outcome of your life insurance application what so ever. Or, to put it another way, the “rate” that you would have been able to qualify.

Now, will we be able to help out everyone who has been prescribed Mucinex?

No, probably not. But what we can tell you is that in addition to offering a wide variety of different term and whole life insurance policies, IBUSA has also worked very hard to establish relationships with many of the Best Final Expense Insurance Companies as well. This way, if someone isn’t able to qualify for a traditional life insurance policy, chances are there may be some other “type” of product that you CAN qualify for.

So, if you’re ready to explore your options, just give us a call!