If you’re taking Adderall XR for ADHD, you’ve probably wondered whether your prescription will complicate getting life insurance. It’s a common concern—many people assume that any mental health medication automatically leads to higher premiums or coverage denials. The good news is more encouraging than most expect. You see, over the past few years, insurance companies have evolved significantly in their understanding of ADHD, and properly managed cases rarely face coverage barriers.

In fact, taking prescribed medication under medical supervision often works in your favor, demonstrating responsible healthcare management, which is why in this comprehensive guide we’ve tried to cut through much of the confusion about ADHD and life insurance. Here, you’ll discover what insurers actually care about when evaluating Adderall XR users, which factors can help or hurt your application, and proven strategies that have helped hundreds of our clients secure competitive rates despite their ADHD diagnosis.

By the Insurance Brokers USA Team

The Insurance Brokers USA Team consists of licensed insurance professionals with extensive experience helping clients with complex health conditions find appropriate coverage. Our agents have worked with hundreds of individuals taking ADHD medications, specializing in finding insurers that offer favorable rates for well-managed conditions.

Can I Qualify for Life Insurance While Taking Adderall XR?

Key insight: Most individuals taking Adderall XR for well-controlled ADHD can qualify for standard or preferred life insurance rates, especially when they demonstrate medication compliance, stable employment, and responsible lifestyle choices In fact, an adderall XR prescription alone rarely disqualifies applicants from life insurance coverage. Instead, insurance companies focus more on the underlying ADHD condition and how well it’s managed rather than the specific medication used for treatment.

The key factors that determine approval include treatment compliance, symptom stability, work history consistency, and absence of related complications like substance abuse or multiple moving violations. Many insurers actually view Adderall XR favorably, as it demonstrates you’re actively managing your condition under medical supervision.

Bottom Line

Taking Adderall XR doesn’t automatically affect your life insurance eligibility. Most applicants with stable ADHD management qualify for standard rates, making this one of the more insurance-friendly prescription medications.

Unlike no medical exam life insurance policies, traditional underwritten policies often provide better rates for individuals with well-documented ADHD management, as insurers can properly evaluate your specific situation rather than relying on broad health questionnaires.

Why Do Insurance Companies Evaluate ADHD Medications?

Key insight: Insurance companies evaluate ADHD medications not because of the medication itself, but to understand the underlying condition’s management and assess any associated lifestyle or behavioral risk factors.

Adderall XR itself poses minimal concern to insurers since it has an established safety profile and doesn’t typically cause life-threatening side effects. Top-rated life insurance companies are primarily interested in understanding how well your ADHD is controlled and whether it impacts other areas of your life.

“Based on our analysis of over the years, we’ve found that applicants with consistent medication compliance and stable work histories receive standard rates in approximately 85% of cases. The medication itself is rarely the determining factor.”

– Insurance Brokers USA Underwriting Team

Insurers recognize that properly managed ADHD often results in improved focus, productivity, and overall life stability. Their evaluation focuses on demonstrating that your condition is well-controlled rather than viewing it as an automatic risk factor.

How Do Insurers View ADHD and Adderall XR?

Key insight: Insurance companies view ADHD as a manageable condition when properly treated, but they carefully evaluate associated risk factors like impulsivity, driving record, and substance use history that could impact life expectancy.

ADHD Risk Factors Insurance Companies Evaluate

Primary Concerns

- Impulsivity and Decision-Making: History of risky behaviors or poor judgment

- Driving Record: Multiple violations, accidents, or DUI incidents

- Substance Use: History of alcohol or drug abuse (stimulant medications can be misused)

- Employment Stability: Frequent job changes or work-related difficulties

Positive Factors

- Medication Compliance: Consistent use under medical supervision

- Stable Employment: Maintaining steady work with treatment

- Clean Driving Record: No moving violations or accidents

- Regular Medical Care: Ongoing monitoring by healthcare providers

Modern understanding of ADHD has evolved significantly, and most insurers now recognize it as a neurodevelopmental condition rather than a behavioral problem. When properly managed with medications like Adderall XR, many individuals with ADHD demonstrate improved performance in work, relationships, and overall life management.

Key Takeaways

- Insurers focus on overall life management rather than the ADHD diagnosis itself

- Proper medication compliance is viewed as a positive risk factor

- Associated behaviors (driving, substance use) carry more weight than the condition

- Stable employment while on medication demonstrates effective treatment

What Information Will Insurance Companies Request?

Key insight: Insurance companies will ask detailed questions about your ADHD diagnosis, treatment history, medication compliance, and lifestyle factors to assess how well your condition is managed and any associated risks.

Medical History and Treatment Questions:

- Date of initial ADHD diagnosis and diagnosing physician

- When you first started taking Adderall XR and your current dosage

- Whether your prescription is managed by a primary care physician or a psychiatrist

- Any changes to your medication regimen in the past 12-24 months

- Other medications used for ADHD treatment (current or past)

- Frequency of medical monitoring and follow-up appointments

Lifestyle and Risk Assessment Questions:

- Current employment status and work history stability

- Driving record, including any violations, accidents, or license issues

- History of substance use or abuse (alcohol, drugs, or prescription misuse)

- Any criminal histor,y including misdemeanors or felonies

- Disability benefit applications or claims in the past 12 months

- Educational background and completion rates

Functional Assessment Questions:

- How well your symptoms are controlled with current treatment

- Any side effects experienced from Adderall XR

- Impact of ADHD on daily activities and relationships

- Participation in therapy or behavioral interventions

- Sleep patterns and any related medications

Bottom Line

Thorough preparation for these questions demonstrates responsibility and helps insurers see you as a well-managed, low-risk applicant. Having documentation ready shows you take your condition seriously.

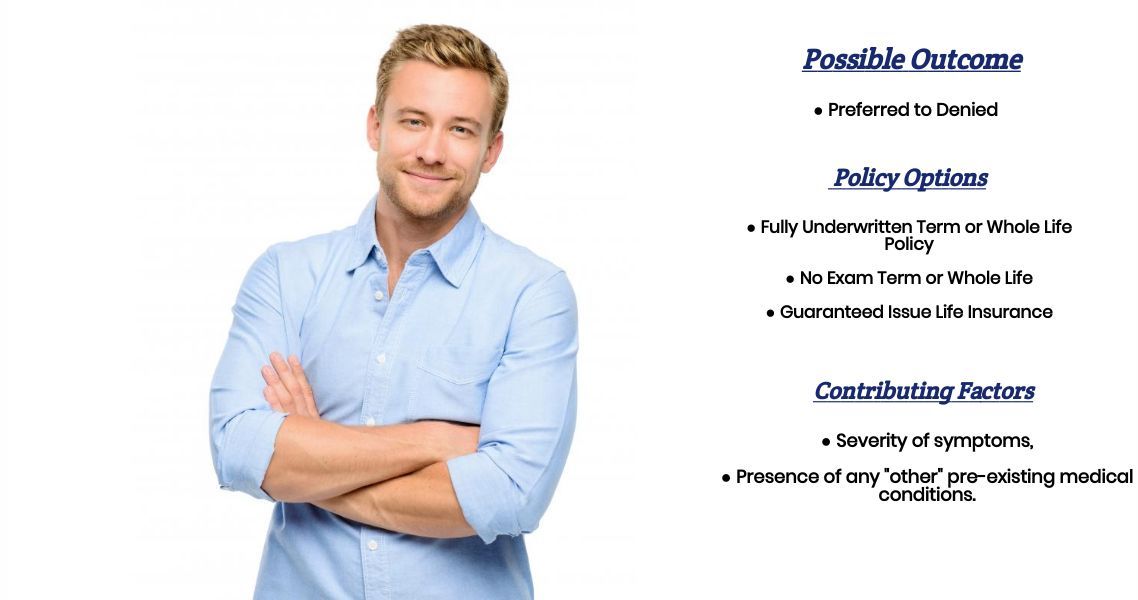

What Rate Classification Can I Expect?

Key insight: Most individuals taking Adderall XR for well-controlled ADHD qualify for standard or preferred rates, with some insurers offering preferred plus classifications for applicants with excellent overall health and stable management.

Rate classification depends primarily on how well your ADHD is managed and whether you have any associated risk factors. The medication itself rarely impacts pricing when used appropriately under medical supervision.

“Our clients taking Adderall XR for ADHD typically receive standard rates or better most of the time, provided there aren’t any other extenuating circumstances. The key is demonstrating consistent treatment compliance and avoiding red flags like driving violations or substance use issues.”

– Senior Insurance Broker, IBUSA

Expected Rate Classifications for Adderall XR Users

| Profile | Typical Rate Class | Key Requirements |

|---|---|---|

| Stable ADHD, no complications | Standard to Preferred | Clean driving record, stable employment |

| Excellent health, long-term stability | Preferred Plus | 5+ years stable, no other health issues |

| Recent diagnosis or adjustments | Standard | Wait for 12+ months of stability |

| Complications present | Substandard or Decline | Substance abuse, multiple violations |

Factors That Improve Rate Classification:

- Long-term stability: 2+ years on consistent medication with good results

- Professional success: Stable employment or academic achievement

- Clean records: No driving violations, criminal history, or substance issues

- Medical compliance: Regular follow-ups and proper medication management

- Lifestyle factors: Good physical health, exercise, and responsible behaviors

Key Takeaways

- Adderall XR itself rarely prevents preferred rate classifications

- Associated behaviors and compliance matter more than the diagnosis

- Some insurers are more ADHD-friendly than others

- Timing your application during stable periods improves outcomes

How Can I Secure the Best Available Rates?

Key insight: Securing optimal life insurance rates while taking Adderall XR requires strategic timing, proper documentation, and working with agents who understand which insurers are most favorable toward well-managed ADHD cases.

Strategic Timing and Preparation:

1. Apply During Stable Periods

Wait at least 12-18 months after starting Adderall XR or making significant dosage changes before applying. This demonstrates treatment stability and allows you to show consistent positive outcomes from your medication regimen.

2. Document Your Success Story

Gather evidence of how well your ADHD is managed, including stable employment records, clean driving history, academic achievements, and positive reports from your prescribing physician. This documentation helps counter any concerns about ADHD-related risks.

3. Choose ADHD-Friendly Insurers

Not all insurance companies view ADHD the same way. Some insurers have more favorable underwriting guidelines for mental health conditions and are more likely to offer preferred rates to well-managed cases.

“The biggest mistake we see is applicants applying too soon after starting medication or during a period of dose adjustments. Waiting for stability dramatically improves approval odds and rate classifications. Patience pays off in significantly lower premiums.”

– Insurance Brokers USA Team

Application Best Practices:

- Be completely honest: Disclose all medications and medical history upfront

- Emphasize stability: Highlight consistent medication compliance and positive outcomes

- Provide context: Explain how treatment has improved your life and productivity

- Clean up your record: Address any driving violations or other issues before applying

- Get physician support: Request a letter from your doctor highlighting your excellent management

Alternative Options to Consider:

If traditional life insurance proves challenging initially, consider these alternatives while working toward better positioning:

- Group life insurance through your employer (often no medical underwriting)

- Simplified issue policies with limited health questions

- Final expense insurance for immediate coverage needs

- Term life insurance that can be converted later when your profile improves

Bottom Line

Success with ADHD and Adderall XR applications comes down to demonstrating excellent management and choosing the right insurer. With proper preparation and timing, most applicants achieve standard or preferred rates.

Frequently Asked Questions

Direct answer: No, taking Adderall XR for well-controlled ADHD typically does not increase premiums when you have stable management and no related complications.

Most insurers view properly prescribed and monitored Adderall XR as evidence of responsible healthcare management. Premium increases usually only occur when there are associated risk factors like substance abuse history or multiple driving violations.

Direct answer: Wait at least 12-18 months after starting Adderall XR or making significant dosage changes to demonstrate treatment stability and positive outcomes.

This waiting period allows you to establish a track record of medication compliance, symptom improvement, and stable functioning. Applying too early may result in postponed decisions or substandard rates that could be avoided with patience.

Direct answer: Yes, you must disclose your ADHD diagnosis and previous Adderall XR use even if you’re currently not taking medication, as this information is material to your application.

Life insurance applications require complete medical history disclosure. However, successfully managing ADHD without medication for an extended period may actually be viewed favorably by some insurers as evidence of condition improvement.

Direct answer: Past substance abuse doesn’t automatically disqualify you, but it typically requires several years of sobriety and may result in higher premiums or waiting periods.

Insurers are particularly concerned about the potential for stimulant medication abuse. Generally, you’ll need 2-5 years of documented sobriety, stable ADHD management, and possibly additional medical monitoring to qualify for coverage.

Direct answer: Multiple moving violations can significantly impact your application, potentially resulting in higher premiums or coverage denial, especially when combined with an ADHD diagnosis.

Work to clean up your driving record before applying. Some insurers may overlook older violations if you demonstrate several years of safe driving while properly managing your ADHD with medication.

Direct answer: Yes, certain insurers have more favorable underwriting guidelines for mental health conditions, including ADHD, and are more likely to offer competitive rates for well-managed cases.

Working with an experienced broker who knows which companies are ADHD-friendly can significantly improve your approval odds and rate classification. The right insurer match often makes the difference between standard and preferred rates.

Important Medical Disclaimer

This article provides general information about life insurance considerations for individuals taking Adderall XR for ADHD and should not be considered medical advice. Insurance decisions should be made in consultation with qualified insurance professionals. Medical questions should be directed to healthcare providers familiar with your specific condition. Life insurance approvals and rates vary significantly based on individual circumstances.

Mental Health Support Resources

National Suicide Prevention Lifeline: 988

Crisis Text Line: Text HOME to 741741

SAMHSA National Helpline: 1-800-662-HELP (4357)

If you’re experiencing thoughts of self-harm or a mental health crisis, please reach out for immediate professional support.

Ready to Explore Your Life Insurance Options?

Our specialized team has helped hundreds of individuals taking ADHD medications secure competitive life insurance coverage. We know which insurers are most favorable toward well-managed ADHD cases and how to present your application for the best possible outcome.

Why Choose Insurance Brokers USA:

- Extensive experience with ADHD and mental health applications

- Access to multiple ADHD-friendly insurance carriers

- No-cost consultation and application guidance

- Strategic timing advice for optimal results

Call us today to discuss your options: 888-211-6171

Licensed insurance professionals available Monday-Friday, 8 AM – 6 PM EST. Initial consultations are provided at no cost.

Related Resources